Stable, transparent, not very complicated, reasonably profitable, and often quite collegial. It also has flaws.

As noted in Part I (330) of this “learning about law firms” series, it’s taken nearly two decades in the trenches, including many years doing applied work with law firms, for a very confusing and counterintuitive insight to come into focus: Most large firms are not “firms” in the sense of conventional business theory. Instead, they are a confederation of individual partners building and running leveraged practices in various complementary and adjacent legal specialties.

In today’s essay (Part II), I’ll add a second counterintuitive insight: For the most part, lawyers pay little or no financial price for organizing themselves as a confederation rather than a firm. Even in the event of spectacular collapse, as was the case with Dewey, Brobeck, Heller, Howrey, Thelen, and many other large firms, see ALM Staff, “30 Years of Law Firm Collapses: An Annotated Timeline,” Law.com, Oct 29, 2019, there’s always a large cadre of competitor firms looking to give the partners (and their fee-generating practices) a new home. In most cases, what provides financial security and certainty to an equity partner is seldom the quality of firm-level strategy, or the ability of firm leadership to execute, but instead the health and vitality of their own practice.

This is what distinguishes law firms from conventional businesses. Like Legos blocks, individual law practices can be removed from one law firm and snapped onto another. Some Lego pieces involve a single lawyer; others are leveraged, involving one or more partners who keep several associates, paralegals, and staff busy; most are external facing, but some are internal and enable the growth and stability of other practices; but all of them, for the most part, pull their own economic weight.

Because their law practice is their most valuable professional asset, law firm partners are generally going to prefer a governance structure that enables them to protect it while also providing resources to improve its economic performance. This explains why confederation is the default model of law firm governance. Nonetheless, the confederation model is severely undertheorized by academics and consultants. This is probably because it reflects the natural resting place of lawyers seeking to balance risk and reward, requiring about as much reasoned justification as food or sleep.

The purpose of today’s Part II is to go deep into the confederation model. Without this knowledge, we can’t meaningfully evaluate the desirability or viability of any change or modification, particularly from a law partner’s point of view. Part II covers the following three topics:

- How the relationship between economic and social incentives changes as a law firm grows in size. In smaller firms, it is easier for partners to develop trust and sharing practices that advance the collective interests of the firm, thus softening the impact of mechanical formulas that reward individual practices.

- Why the confederation model works good enough in larger law firms, and fabulously well for some individual lawyers and practices, thus undercutting the urgency necessary to drive more ambitious firm-level strategy and innovation.

- The concept of firm-specific capital, which is the key ingredient necessary for lawyers to comfortably share clients and risk. This section discusses (a) our shallow understanding of the Cravath firm and lockstep compensation, (b) a new type of market power enjoyed by today’s super-rich firms, and (c) a new type of firm-specific capital grounded in legal expertise combined with data, process, technology, design, and business operations.

A true profession figures out how to overcome its own internal collection problems so that important things that serve clients and the public actually get built. This essay series is part of that project.

1. Economic and social incentives; small versus large

The final section of Part I (330) noted that the Paganelli Law Group (an 18-lawyer firm in Indianapolis, and one of the mini-case studies in my 2022 Law Firms class) had a 100% objective compensation formula, which is a hallmark of a pure confederation model. However, it also has an admirable and magnetic law firm culture that values work-life balance and the training of junior lawyers.

Well, that’s quite a data point.

A. Dunbar’s Number

At the end of Part I (330), I also hinted at a plausible explanation: the Paganelli Law Group was below Dunbar’s Number of 150, which is the cognitive limit to the number of stable relationships in any social unit.

When at or below 150, individuals in the group know each other’s roles and status and thus can work together cooperatively to advance their collective group interests. However, once beyond this limit, peer pressure and group norms are no longer effective for maintaining group cohesiveness; hence the need for formal governance structures that can mediate individual and group competition. See Part I (330)(citing Robin M. I. Dunbar, “Co-Evolution of Neocortex Size, Group Size and Language in Humans,” 16 Behav & Brain Sci 681 (1993)).

The core point is that in smaller firms, culture can be a powerful and workable substitute for management and governance. The objective, formula-driven compensation model makes clear that the ABCs of law practice (acquire, bill, collect) are critical to the survival of the firm. However, within a close office environment in which everyone knows each other and wants to fit in, the ABCs can easily become a team sport.

Tony Paganelli‘s career suggests some limits to the small, collegial, and economically successful confederation. For example, Tony told my Law Firms class that Paganelli Law Group is consciously modeled on the Sommer Barnard law firm, where Tony practiced from 1998 to 2008. Tony described Sommer Barnard as a “hippie culture” created in the late 1960s by partners from larger firms who wanted to do sophisticated legal work but also avoid the painful formalities of a larger partnership. According to Tony, this is where he became a fully developed lawyer, eventually being promoted to partner.

At the same time, however, the mix of corporate work was changing (less regional, more national and international), which made a large single-office Indianapolis firm less competitive for work. Hence, in 2008, Sommer Barnard become the Indianapolis office of Taft Stettinius & Hollister LLP (currently #100 in the AmLaw revenue legal tables).

Paganelli Law Group fills a slightly different market niche. What makes it sustainable in the year 2022 is a close-knit collegial and transparent culture, technically skilled lawyers, an advantageous cost structure (Tony tells his corporate clients, “I’m selling dollars for 75 cents”), and the ability to focus on Type 1 to 4 clients, whereas larger firms want and need the larger projects coming from Type 5 and 6 clientele. See Post 285 (size of legal market broken down by client type).

B. The Bermuda Triangle of law firm management

During Week 6 of my “Law Firm as a Business Organization” class, our guest speaker was Tim Mohan, former Chief Executive Partner of Chapman and Cutler (currently #132 in the AmLaw 200 revenue league table), who provided additional insight on the nuanced relationship between economic and social incentives.

Specifically, Tim told the story of attending Patrick McKenna’s “First 100 Days” Master Class back in 2010 when he was promoted to the firm’s top leadership position. Although Tim had long been an avid student of strategy and management, one of the key takeaways from Patrick’s class was the importance of having a one-on-one meeting with every equity partner in the firm and listening to their thoughts on the future direction of the firm.

Very early in his tenure, Tim completed this task, in most cases each traveling to his partner’s home office. In hindsight, he viewed it as perhaps his single most valuable decision as Chief Executive Partner. Yet, he remarked that it would not have been possible if the firm had been significantly larger. At the time, the firm had roughly 90 equity partners, a point he made in direct reference to Dunbar’s Number of 150.

Tim then told the story of attending Harvard’s Law Firm Leaders Program, where Ashish Nanda did a session on the Bermuda Triangle of law firm management. To illustrate, Mohan shared the graphic below:

Mohan’s takeaway was that Chapman (relatively small for an AmLaw 200 firm) had not yet entered the danger zone of needing to invest in a formal management structure — but more importantly, maybe Chapman would be culturally and economically better off by staying to the left of the triangle.

Mohan’s takeaway was that Chapman (relatively small for an AmLaw 200 firm) had not yet entered the danger zone of needing to invest in a formal management structure — but more importantly, maybe Chapman would be culturally and economically better off by staying to the left of the triangle.

Several years ago, during my Lawyer Metrics days, I was part of a team that built a detailed law firm profitability model that heavily leveraged virtually all the data published by The American Lawyer and the National Law Journal. Much to our satisfaction, we predicted approximately 80% of the variation in average partner profits. The graphic below summarizes the results:

After publishing our results, Evan Parker and I had a conversation with Tim Mohan, letting him know that his firm appeared to be doing everything right. Moving from the top to the bottom of the chart, here are it’s key takeaways:

- A focus on specific practice areas (i.e., greatest percentage of lawyers in few practices) is a strong positive driver of firm profits.

- Geographic concentration (usually a large percentage of lawyers in a headquarter office) is associated with higher profits.

- All else equal, Total Attorney Headcount is associated with lower profits.

Several years before we created our model, Chapman and Cutler adopted the tagline “focused on finance,” which reflected the strategic decision to become less of a general service firm, thus making it easier to keep the firm relatively small (still mostly Chicago-based) and to the left side of the Bermuda triangle.

As part of his mini-case study, Tim shared financial data, which showed firm revenues increasing from $101 million in 2005 to $261 million in 2021 (moving from #184 to #132 in AmLaw 200 rankings). During the same period, profits per partner increased from $565,000 to $1.6 million (from #109 to #62). Obviously, Tim and his colleagues didn’t need our help to formulate an effective strategy. Nonetheless, he was grateful for the empirical validation, which he shared with his partners. (NB: for significant updates and improvements on this model, contact Evan Parker at Parker Analytics.)

My students, of course, were very interested in how profits are allocated at Chapman, as they had heard stories in other sessions about partners fighting over origination credits. Tim Mohan made clear that Chapman is not an eat-what-you-kill law firm, as partner compensation is determined subjectively by firm management after taking in a large amount of quantitative and narrative data. On this front, it’s noteworthy that Eric Wood was promoted from associate to equity partner at Chapman based on his work in document automation and related practice-management technology. See Post 039. That said, Tim also made clear that bringing in clients is very relevant—as the surfers say, “no tide, no ride.”

Chapman does not fit the confederation default model, albeit it’s taken care to stay to the left of the Bermuda Triangle.

C. Summary

The key point of this section on that the social incentives of smaller law firms—i.e., organizations that are less than Dunbar’s Number and/or to the left of the Bermuda Triangle—tend to mediate and soften economic incentives to focus solely on one’s own practice. Regardless of the formal compensation model, smaller firms find it much easier to behave like actual firms.

2. Why the confederation model works good enough for many, and fabulously for some

A. The virtue and simplicity of leaving partners alone

Let’s start with a concrete example from the vantage point of a highly productive partner.

Several years ago, during my days at Lawyer Metrics, I was working with a very large firm (AmLaw 100, well past Dunbar’s Number) on their lateral partner recruitment process. As part of the project, I met with numerous partners, including one of the firm’s biggest producers, who had a $20+ million leveraged practice made possible by obscure government regulations in a niche market that few lawyers understood or even knew existed. During his early years, he realized that his core customers strongly preferred flat-fee pricing, as it simplified and sped up deal velocity. After he made this change, his practice captured virtually the entire niche market. Further, as his team drove greater efficiencies, more money dropped to the bottom line.

In this partner’s mind, the most desirable lateral partner was someone who was consciously building “an enterprise,” which he described as a freestanding business embedded inside a larger law firm. This attitude was definitely not an outlier within the firm. During the meeting when this topic was being discussed, a younger partner nodded in agreement, discussing his own $5 million green energy finance practice. In the years ahead, he thought it could also become a $20 million enterprise.

A few days later, as I probed the firm’s strategy with the firm’s leadership, I realized that the firm’s actual strategy was to attract partners with current or future enterprise practices and, thereafter, “leave them alone.” Why? Because that was how many of the firm’s biggest producers wanted to be treated. This was the ultimate low-touch strategy and management.

So how does this type of confederation work in practice? It’s a firm that has a brand by dint of its regular appearance in the AmLaw 100-200 league tables. This affiliation is important to partners because, in the event of a bad outcome, it provides cover to the in-house lawyers who hire them. Yet, beyond the veneer of prestige and eliteness, the confederation is primarily a vehicle for shared services, such as marketing, IT, associate recruitment & development, insurance, office space, and various support practices (e.g., tax, L&E, Erisa, and environmental issues that arise in the context of M&A).

Of course, this is a generalization. In either substance or degree, it’s not true of every firm.

An example of a confederation in its purest form is the virtual law firm of FisherBroyles, which recently broke into the AmLaw 200 despite having no associates and no physical offices for partners. See New Release, “FisherBroyles Reaches New Am Law 200 Milestone,” May 26, 2022. According to the most recent AmLaw data, Fisher Broyles has 295 lawyers, 295 partners, and is currently ranked #188 in total revenues, at $136 million. Compensation is 100% formula based. The average partner makes $386,000 per year, yet supervises no associates, has no committee duties, and has complete control over his practice. Of course, before you join, someone else will need to teach you how to practice law and acquire clients.

It’s noteworthy that a significant number of upstart firms are adopting the same virtual pure confederation model. See, e.g, Jenna Greene, “Is virtual firm Scale LLP the wave of the future?,” Bloomberg Law, Oct 6, 2021 (discussing the 50-lawyer Scale LLP and several similar virtual firms). In effect, this gives partners the option of retaining the title of partner while becoming a well-paid gig worker.

B. Business school theory inside a confederation

Harkening back to the bread-and-butter concepts taught in business school, what explains the enduring stability and prosperity of a business model that is so disinterested in a single, unified strategy?

As I explain to my students, a successful confederation relies upon some type of eat-what-you-kill (EWYK) compensation system, a term they find jarring, at least initially, but also memorable and descriptively accurate of so many systems that carefully track (and negotiate and split) origination credits. By making internal referrals within a large firm of specialists, a partner can reap financial rewards for work performed by other lawyers while simultaneously reducing the likelihood that his or her clients will consult with lawyers at another firm. In theory, the confederation can both grow and protect each partner’s enterprise practice.

A capable business school strategist would be quick to point out that it’s possible for a law firm, or even a group of partners, to make more money by designing a more coordinated and sophisticated approach that can solve some of the most difficult and vexing problems facing clients. Outside counsel, after all, are ideally situated to see and identify patterns across a wide range of clients and industries. Further, this isn’t pie-in-sky academic theory—it’s the exact approach used by the Big Four to build their large and lucrative non-audit service offerings, which include, in Europe and elsewhere, the practice of law.

Remarkably, this type of growth remains relatively rare in law firms. A war story from fellow LE contributor Patrick McKenna explains why.

At the time, Patrick was working with a large law firm with a strong international reputation. Patrick explained to the partners in one of the firm’s largest practice groups how a modification in the compensation model (away from EWYK) would incentivize the type of partner collaborations that would (a) attract a broader array of clients and (b) command even higher premium rates.

In the context of a practice group strategy session, Patrick’s approach certainly made sense. Yet, in a series of private side bars, many of the partners revealed to Patrick that they hated the idea, not because it was bad, but because they came to firm specifically because of its highly objective compensation model, thus putting their pay entirely within their own control. Patrick’s approach required the partners to develop a new set of skills combined with a willingness to trust their partners. For many, that was a bridge too far.

If just 10% of partners moved to another firm in response to an increase in shared risk, the firm’s leadership has created enormous headwinds for meeting the current year’s budget. The inevitable result is to ignore the advice of any business strategist who naively believes that they’re advising a firm that’s trying to maximize overall profit.

The pervasiveness and durability of the confederation model is also revealed in Heidi Gardner’s excellent work on lawyer collaboration. As discussed in detail in Post 191 (lawyers and teamwork), the thrust of Gardner’s empirical work on collaboration is that, from an individual lawyer perspective, and independent of how partners are compensated, it pays to export surplus or out-of-scope work to more capable and/or lower-cost peers. Why? Because in the long run, the internal and external clients notice the commitment to problem-solving. Thus, in some second or third period in the future, the economic rewards eventually come to both the lawyer and the firm.

That said, ad hoc collaboration in service of solving your clients’ problems is not the same thing as sharing risk with your partners. In a confederation, when Partner A has a bad year, that’s largely Partner A’s problem, as Partner B still reaps the full rewards of their own practice management. Although the partners are less likely to capture the benefits of a coordinated strategy touted by the MBA crowd, a confederation keeps all the partners focused on the ABCs of law practice. For many lawyers, that’s a good enough reason to keep it.

3. Firm-specific capital, past and future

Most lawyers have impatience with academic theories, and over the years, I’ve come to understand why. Although “the juice may be worth the squeeze,” most lawyers are too time-starved to make the investment. This is why virtually every discussion of law firm strategy begins (and often ends) with what peer firms are doing.

Legal Evolution, however, is focused on applied research, which is about solving “practical problems of the modern world.” Post 001 (emphasis in original). Following this approach, if you want to understand the conditions that enable law partners to comfortably share clients and business risk, you need to understand the concept of firm-specific capital. Likewise, firm-specific capital is what is necessary for lawyers and law firms to innovate in ways that dramatically improve lagging legal productivity, which is a serious social problem connected to, among other things, the access to justice crisis. See Post 042. In short, this is worth the time of serious professionals.

Note that the “future” of firm-specific capital, which is briefly touched on below, is the topic of Part III of this series, which will be published in two weeks (10/23). Part III is primarily a case study of a current AmLaw 100 law firm and its ingenious leveraging of lawyers and allied professionals to build a competitive advantage that is very difficult to replicate and near impossible to move to a rival firm.

A. The theory of firm-specific capital

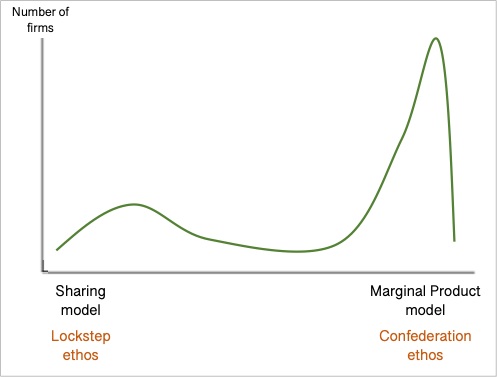

Early in my research on law firms, I read an influential article by Ron Gilson and Robert Mnookin that theorized that all partner compensation systems could be plotted along a continuum between a “sharing model,” which in its purest form was based on partner seniority, and a “marginal product model,” which sought to accurately and fully reward each partners’ individual contribution. See Ronald J. Gilson & Robert H. Mnookin, “Sharing Among the Human Capitalists: An Economic Inquiry into the Corporate Law Firm and How Partners Split Profits,” 37 Stan L Rev 313, 348-356 (1985).

Gilson and Mnookin argued that the virtue of the sharing model was that it enabled partners to specialize (which yields higher rates) while also spreading risk across multiple practice areas with offsetting peaks and valleys, such as securities work and bankruptcy. Conversely, the upside of the marginal product model was that it partially checked three types of opportunistic behavior that are bound to crop up in any firm that shares clients:

(1) partners “shirking” their duty to be a fully productive member of the firm; (2) partners “grabbing” a higher percentage of firm profits by threatening to depart; and (3) partners “leaving” the firm with their clients and business in tow.

Henderson, “An Empirical Study of Single-Tier Versus Two-Tier Partnerships in the Am Law 200,” 84 NC L Rev 1691, 1700 (2006) (summarizing Gilson & Mnookin). By paying each partner very close to what their practice could earn at another firm, the incentive to shirk, grab, or leave goes down, albeit so does cooperation.

In light of these Prisoner’s Dilemma-type dynamics, when does it make sense for partners to fully engage in a sharing model? Gilson and Mnookin argued that sharing was both stable and optimal when a law firm possessed “firm-specific capital,” which they defined as some attribute, such as reputation for superior work, that generates some type of premium or advantage that can only be exploited by staying at one’s current firm. Writing their article in 1985, Gilson and Mnookin were obviously describing the elite lockstep compensation firms that dominated New York, Washington, London, or various regional markets.

Twenty years later, when I began my own academic work on law firms, I relied upon the Gilson-Mnookin to unravel a seeming market paradox: Two-tier partnerships (equity and nonequity classes of partners) were quickly becoming the norm in the AmLaw 200 despite overwhelming evidence that single-term partnership (100% equity partners) were much more profitable.

Yet, far from being economically irrational, virtually all the firms adopting two-tier partnerships had lower measures of prestige as measured by the American Lawyer and Vault. In other words, they all lacked the firm-specific capital of a superior brand or reputation. See Henderson, Single-Tier versus Two-Tier, supra at 1729 (reporting statistical results showing that superior profitability of single-tier firms “is probably attributable to superior prestige rather than incentives that flow from the partnership structure”). Indeed, switching to a two-tier structure was arguably a necessary step for firms to survive, particularly as the legal market was gradually transforming from separate and discrete regional fiefdoms to crowded national and international market. See Post 082 (discussing how his competition eventually reached—and transformed—the London market, as US firms overtook the Magic Circle).

Pulling back, and with the benefit of 20 years of observation and experience, the graphic below is a reasonable estimation of how corporate law firms are arrayed along the Gilson-Mnookin continuum.

The implication, of course, is that sharing firms are relatively rare and likely shrinking. Hence, the waning of lockstep. Conversely, for reasons of pure survival, more and more firm are relying on a marginal product model. This explains why, from far away, so many BigLaw firms look like large and prosperous businesses, but up close they operate as confederations of partners with adjacent and complimentary specialty practices that, at the end of the day, are relatively portable. Cf Randy Kiser, American Law Firms in Transition at 1 (2019) (noting that law firms “are remarkably profitable but surprisingly fragile”).

B. A shallow understanding of Cravath and lockstep

As the forgoing analysis suggests, the opposite of a confederation is a lockstep compensation firm, which compensates all partners based solely on seniority.

For several decades, the standard bearer of lockstep was Cravath Swaine & Moore along with the Magic Circle firms in the UK. Although many stories in the legal press report that lockstep is on the decline, see, e.g., John Roemer, “BigLaw’s lockstep compensation is declining in order to keep and attract talent,” ABA Journal, Apr/May 2021, there is a remarkable lack of curiosity, and thus a very shallow understanding, regarding what enabled the lockstep law firms to be so dominant for so long.

Here, it is important to note that the hallowed performance of these firms has two essential pieces that are separated in time: (1) the creation of firm-specific capital, which enables the charging of premium rates, and (2) the implementation of lockstep compensation, which creates conditions that promote the financial value and longevity of the shared enterprise. In the case of the Cravath firm, Paul Cravath had everything to do with (1), but nothing to do with (2).

Specifically, lockstep compensation was not a feature of the Cravath system, nor was it something that Cravath himself would have likely supported. Part of the evidence comes from the first 12 pages of Volume II of the firm’s comprehensive history, which was authored by Cravath partner Robert Swaine and provides a detailed account of virtually all aspects of the Cravath system. The following passage describes how partners are evaluated and progress within the firm:

The younger partner who evidences the capacity to win the confidence of the clients with whom he works so that they continue with the firm, who impresses others who come into contact with his work so that other business comes to the firm through him, and who takes responsibility for a number of varied matters, at the same time supervising the work of members of the staff and sometimes other partners, may well rise, and indeed often has risen, within the firm more rapidly than some of the seniors. … Complete objectivity in such appraisals is not easy, for the most compatible man is not always the best, or the most effective, lawyer.

Swaine, The Cravath Firm and Its Predecessors: 1819-1948 Vol II at 10 (1948). Yet, even more to the point of how profits were divided, in his book, The Lawyers (1967), journalist Martin Mayer tells the story of a group of partners coming to Paul Cravath to suggest changes to the firm’s compensation system. Cravath reportedly replied that he was willing to go along with anything the partners wanted, “provided it was understood that his share remained 50 percent.” Mayer at 335.

Although this is a funny anecdote (and possibly apocryphal), it’s worth taking stock of relative contributions. The Cravath system, which Cravath himself designed and presided over, was creating extremely rare and valuable human capital that, in turn, was being deployed in a coordinated fashion to achieve clients’ complex commercial objectives. As a result, the Cravath firm was perpetually deluged with clients willing to pay the firm’s premium rates. In turn, to compete, all of Cravath’s peer firms adopted some variant of his model, albeit almost all remained in severe catch-up mode.

A crucial point worth hammering home is that the creation of firm-specific capital may require large investments of time over a period of decades. Indeed, it’s likely that without Paul Cravath having complete control over firm management for 30+ years (likely tied to his share of profits), a committee of partners would have scuttled the system as too much work. Certainly, that was the attitude of Cravath’s partner, William Guthrie, the leading trial lawyer of his generation and a massive rainmaker, who departed the firm in part because Cravath’s regimented approach interfered with how Guthrie wanted to run his own large practice. See Post 312 (telling this story and how both men, going their separate ways, became fabulously wealthy serving the interests of Gilded Age clients).

When Cravath died in 1940, the firm had just 17 partners and 70 lawyers. See “Paul D. Cravath Dies Suddenly, 79,” NY Times, July 2, 1940. Thus, it’s likely that the power of the Cravath system was still gaining momentum. Fortunately, by its fourth decade of operation, the lawyers brought up through the system didn’t need to be convinced of its merits, as its transformative power built their careers. By his death, Cravath’s ideas were no longer eccentric theories, but powerful and proven practices.

That said, if Cravath’s firm-specific capital was very expensive to build, its half-life has been truly extraordinary. We know this to be true by comments made last year by Cravath’s presiding partner, Faiza Saeed. In making the announcement that the firm was moving from “pure” to “modified lockstep,” she revealed that pure lockstep was a policy adopted in 1976—36 years after the death of Paul Cravath.

Consistent with the Gilson-Mnookin thesis on firm-specific capital, Saeed’s stated that the firm adopted pure lockstep “to institutionalize and make durable our model.” See Jack Newsham, “Read the memo Cravath sent around to mark the end of its lockstep pay system,” Business Insider, Dec 6, 2021. In hindsight, it appears to have promoted the financial value and longevity of the shared enterprise, as Cravath remained a market leader for another 50+ years.

Saeed characterized the move to modified lockstep as the best way to “advance our strategic objectives so that we can continue to thrive in a dynamic marketplace.” However, it was, in fact, a defensive measure to reduce the risk that sought-after boardroom lawyers will leave for rival firms. Id (citing Scott Barshay’s move to Paul Weiss and Sandra Goldstein’s move to Kirkland).

C. Jae Um’s Prestige League, market power, and the future of firm-specific capital

Obviously, something important has changed, as elite large law firms have never been as profitable as they are today, and virtually all of the historical lockstep firms have altered their compensation systems so they can compete (or defend) more aggressively in the market for lateral talent.

Firm-specific capital is an attribute that can only be exploited by staying at one’s current firm. With a frothy lateral market that is affecting even the most elite firms, it’s worth asking, “Does firm-specific capital have a future?” I think the answer is yes, albeit it’s important to understand the larger economic forces that have reshaped the market for corporate legal services and created significant market power for a few dozen large firms.

Foremost, over the last half-century, the firms that comprise the present-day AmLaw 200 transitioned from comfortable regional fiefdoms (1970s and 80s), to general service firms competing on a national-international level (1990s and 00s), to larger, more specialized firms, some of which have obtained considerable market power in complex, technical niche markets serving the world’s largest and wealthiest clients (2010s to the present). In purely economic terms, this is a multi-decade-long dynamic that has produced various graduations of prosperity, from very comfortable to annual income on par with professional athletes. See Post 082 (discussing this multi-decade change).

The reference to professional athletes is apt, because, for this year’s AmLaw results, Jae Um created an ingenious bracketing system modeled on the English football league system, which is a pyramid of leagues. As U.S. fans of Ted Lasso have recently learned, the top bracket is the Premier League, which features the nation’s 20 most talented and competitive teams. Underneath it is the Championship League, which is composed of another 24 teams. At the end of each year, the top three teams in the Championship League are “promoted” to Premier; and the bottom three teams in the Premier League are “relegated” to Championship. A similar dynamic applies to several layers of additional leagues underneath, which Jae lumps together as “Everybody Else,” or EE.

(NB: As noted below, if you’re a law student, “Everybody Else” is a very important category for you.)

Below is Jae’s Premier League, which was published in the May 2022 edition of The American Lawyer.

{kind=link}

With a handful of possible exceptions, most of the firms in the Premier and Championship Leagues are confederations of partners tied together with a very clear-eyed view of how to maximize the value of their human capital. In general, the strategy is to assemble teams that can win the most complex, high-stakes, price-insensitive work. This requires every personnel move to strengthen or broaden best-in-class practice areas. In turn, the practice groups target lucrative sector niches; hence Jae’s column for sector focus. If you’ve made the roster of a Premier or Championship League firm, particularly at the partner level, you understand the benefits of maintaining the strategic focus.

To illustrate how and why this works, consider the International Financial Law Review (IFLR1000), which is a country-by-country, continent-by-continent ranking service of law firms doing work in the financial sector. Obviously, the financial sector is very important to law firms because it accounts for roughly 20-25% of the world economy. See Sean Ross, “Financial Services: Sizing the Sector in the Global Economy,” Investopedia, Sept 30, 2021. For the IFLR 1000 rankings for the U.S., legal work is grouped into 16 different categories (Banking, M&A, Private Equity, Debt, Derivatives, High Yield, Regulatory, Fund Formation, Project Finance, Securitization, etc.). Further, the firms in each category are grouped into seven tiers. All the firms in Jae’s Premier and Championship Leagues appear multiple times, usually in the top tiers.

Because this type of complex work is for the world’s wealthiest clients, it necessarily flows to firms and lawyers who have deep experience and a track record of success. See Post 138 (Dan Currell of AdvanceLaw explaining the massive advantage of selling your narrow, on-point experience, particularly for high-stakes work). Further, because corporate executives, including in-house lawyers, don’t want to be second-guessed in the event of a bad outcome, there’s little benefit to price-shopping. As a result, firms in the Premier and Championship Leagues can comfortably pass along large rate increases each year.

What I’ve described above is market power across a series of narrow, technical practice areas that often include expertise in particular industry sectors. In contrast, a strategy focused on firm-specific capital might use data, process, technology, design, and business operations expertise to improve the quality of the work, or providing value-add insights to the client, while also reducing overall lawyer and staff effort. In turn, the firm could bid for larger tranches of narrow, specialized on a flat-fee basis, thus increasing firm profits while taking market share away from competitors. This approach, which requires lawyers to work with allied professionals to produce new types of production systems, can only be exploited by partner owners who remain with the firm. It also creates market power, albeit through innovation that directly benefits clients.

This is not MBA-school theory. As Tim Mohan shared with my Law Firms class, this is an approach being taken by Chapman and Cutler, due in part to its focus on finance and in part to the willingness of Chapman partners to share risk.

The key point I’m making here is that the creation of firm-specific capital is a strategy available to all firms, including Jae Um’s “Everybody Else” category. The fact that the market power of firms in the Premier and Championship Leagues are likely to produce larger economic returns, at least in the short to medium term, is not relevant to the vast majority of law firms, as the free-agent market for lateral talent will decimate a law firms attempt to get promoted to a higher league. Thus, for most law firms, the long-term strategic option is to build firm-specific capital for whatever type of legal work you already have a lot of. But first, the firm has to overcome the collective problem of shared risk and investment that’s endemic to the confederation default model.

Conclusion

Part III of this series, which publishes on October 23, is a real-world example of an AmLaw 100 firm creating firm-specific capital that is destined to deliver them a competitive advantage for many years to come. The substance of it comes from my Week 4 guest speakers, Gene D’Aversa, Senior Director Knowledge Management and Technology Innovation at Husch Blackwell, and Gavin McGrane, CEO and co-founder of Pacer Pro.

Hat tip to my Week 5 guest speakers, Jae Um and Stephen Poor, Chairman Emeritus of Seyfarth Shaw, whose comments in class helped inspire the above analysis. My students raved about depth and generosity of their insights, as Jae and Steve deftly deconstructed the legal market and law firm strategy and then went the extra mile to translate it all into career advice.