One-to-many legal solutions are built by teams of multidisciplinary professionals. It’s time to build a legal talent supply chain.

The above graphic is a map of the human capital needed to create “one-to-many” legal solutions (Human Capital Map). It’s a dense graphic on a complex topic. To explain its structure and the key insights it provides, I’ll cover the following topics:

- What’s a one-to-many legal solution?

- The structure of the Human Capital Map

- L2C versus the L2C markets

- Bespoke lawyering: still important, still profitable

- Challenges to traditional large law firm model

- The Type 1 innovation lawyer [needed to design and build one-to-many solutions]

- Constructing a better legal talent supply chain

- The primary structural bottleneck

- Fixing the bottleneck

The endpoint of this essay is a first-cut proposal to construct a better legal talent supply chain. It’s a proposed pilot that, if successful, could be scaled to benefit clients, legal employers, law schools, and young people trying to launch a successful career in law.

1. What’s a one-to-many legal solution?

One-to-many legal solutions are a combination of legal products and services that are designed to scale to many clients and consumers. “Many” ranges from several dozen to several million clients/consumers; the total quantum depends upon the market segment being served.

Scale is important because it enables us to achieve higher quantity and quality (measured by speed, outcome, user experience, etc.) while also driving down total per-unit cost. Simply stated, scale is how most wealth is created, from agriculture to medicine to transportation to housing to consumer electronics. Now comes law.

Obviously, one-to-many solutions are good for clients and broader society. But they’re also potentially lucrative for innovative organizations that become dominant in a particular market segment, including very narrow micro-niches. See, e.g., Post 072 (discussing transition issues and PartnerVine, a one-to-many legal marketplace). There’s no need to debate the advent of one-to-many legal solutions. They are being developed now because (a) the capability exists and (b) the benefits, both public and private, are enormous.

What is worth discussing, however, is how legal industry stakeholders can come together to build an explicit, high-functioning legal talent supply chain. Out of pure self-interest, some type of collaboration is bound to occur. This is because collaboration is the best way to de-risk the process of creating teams of highly skilled knowledge workers who have the requisite depth and breadth of skills and experience. Cf. Post 053 (discussing how law firms and NewLaw are coping with cost and risk of developing P3 legal talent). Yet, layered on top of commercial benefits is the profound social good that such an effort would accelerate.

By building a more explicit talent supply chain, we connect ourselves to the success of the next generation of legal professionals, which is one of the hallmarks of a true profession. Conversely, if we fail to support a more coordinated industry-level response — if we just leave it to market actors seeking to maximize profit and prestige — we going to experience continued market failures that harm clients and stymie the ambitions of talented young people seeking to launch heir legal careers. See Part 8 below (data on failing supply chain).

This post is about the golden opportunity. Over the next half generation or so, we’re going to find out who we really are.

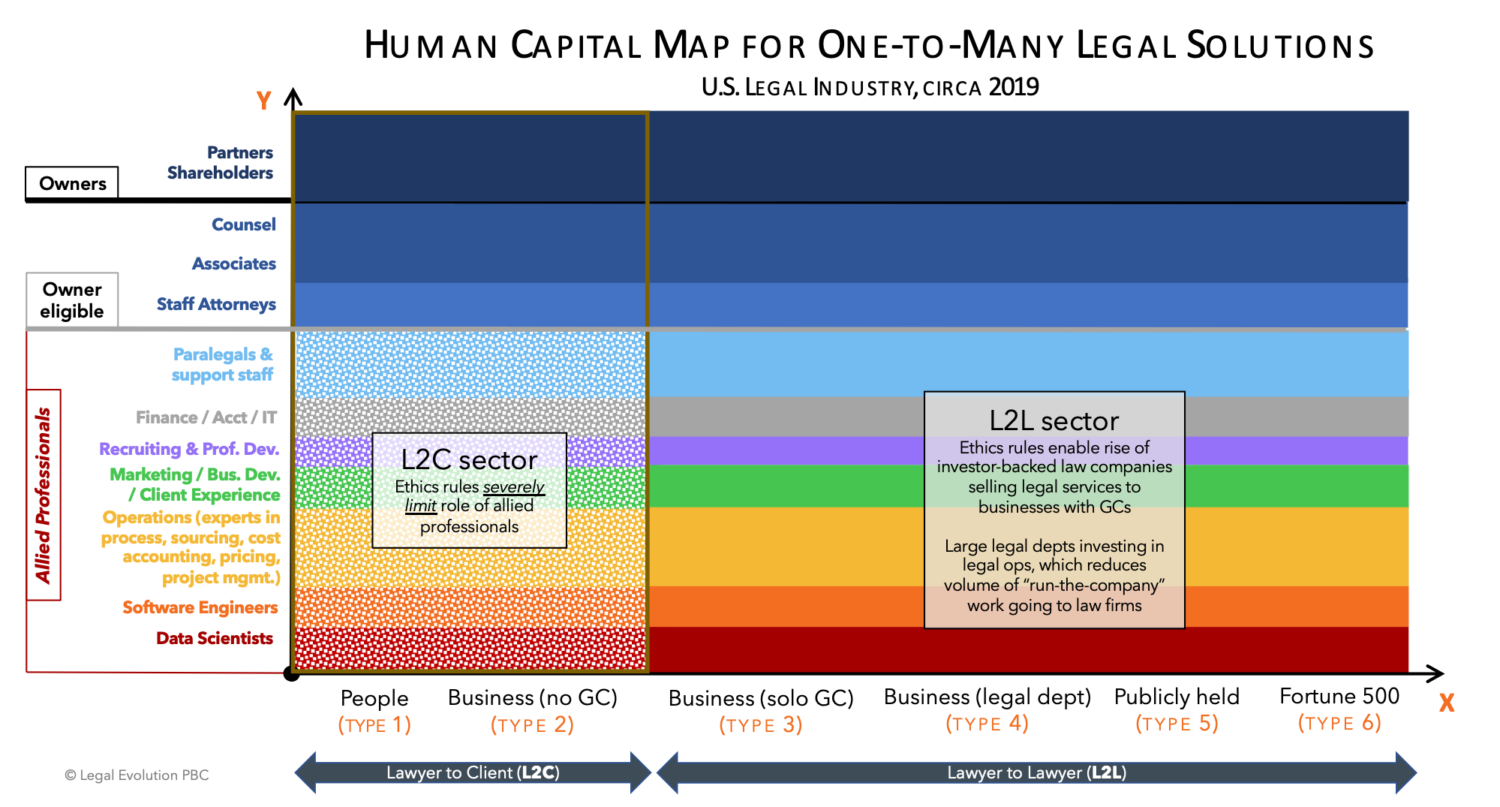

2. Structure of Human Capital Map

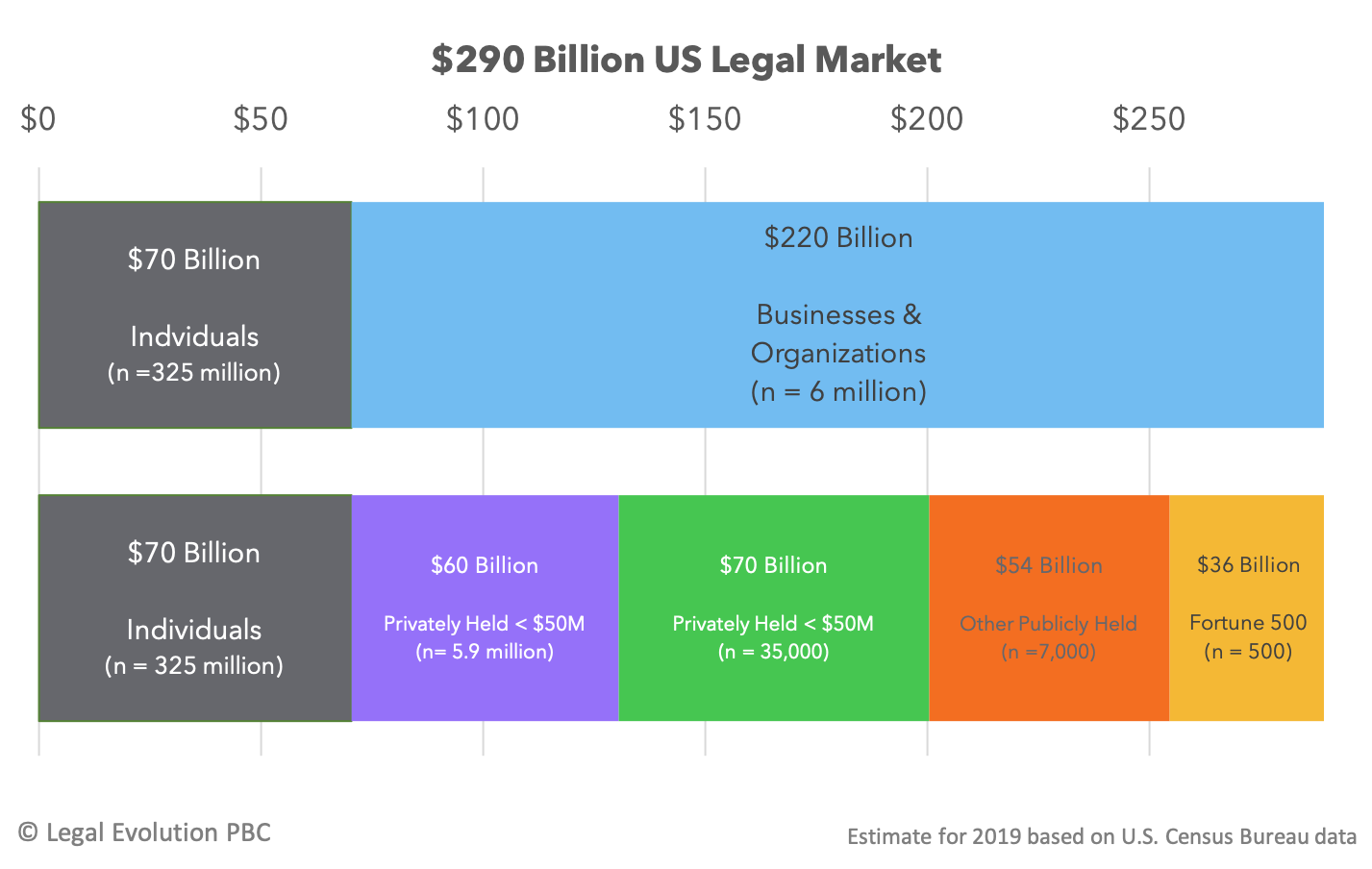

Type of legal professional (y) runs from law partner (dark blue, top) to data scientist (dark red, bottom). Market segment (x) reflects the type of client based on rough volume of paid legal work. Thus, we move from a pure PeopleLaw practice (Type 1 clients) to very large corporations with sophisticated legal departments (Type 6 clients). See Post 005 (presenting client typology); Post 048 (using client typology to illustrate rate of innovation diffusion).

Every professional, not just lawyers, currently employed in private practice should be able to locate their specific x/y coordinates.

In interpreting the map, I offer one important caveat: The spacing of market segments on the x axis roughly corresponds to size (based on revenue), see Size of US Legal Services Market, but the same is not necessarily true for the colored bands that correspond to each type of legal professional (y-axis). Although we lack an industry-level census of professionals by role (we need one), we can nonetheless be confident that the total number of allied professionals is destined to grow relatively quickly over the next generation, with some portion of these positions being filled by law graduates who, before or during practice, acquired the additional skills needed to make the transition. The rest will be allied professionals who build their careers in law.

{kind=link}

3. L2C versus L2L markets

One the left side of the Human Capital Map, we have a brown vertical line, which delineates the lawyer-to-consumer (L2C) market from the lawyer-to-lawyer (L2L) market. In the L2C segment (see cutout to the right) the color bands for the allied professionals are variegated. I added this effect to signify how the Rule 5.4 prohibition on fee-splitting reduces the quantity and quality of collaboration between Main Street lawyers and the allied professionals working at companies like LegalZoom and Avvo.

One the left side of the Human Capital Map, we have a brown vertical line, which delineates the lawyer-to-consumer (L2C) market from the lawyer-to-lawyer (L2L) market. In the L2C segment (see cutout to the right) the color bands for the allied professionals are variegated. I added this effect to signify how the Rule 5.4 prohibition on fee-splitting reduces the quantity and quality of collaboration between Main Street lawyers and the allied professionals working at companies like LegalZoom and Avvo.

As noted by law professor and economist Gillian Hadfield, this is a very bad outcome for ordinary people. See Hadfield, “Legal Barriers to Innovation,” 31 Regulation 14 (Fall 2008) (noting greatest harm on the pricing and availability of legal help “in the personal services sector”). This is because one-to-many solutions in the L2C space do not make economic sense without very large investments in technology, marketing, and customer experience, which (again) is a problem of scale. To sell at a low price, the total addressable market needs to be very large. Obviously, the solo and small-firm crowd lacks the capital, risk tolerance and expertise to make this happen on their own. Further, and more significantly, Rules 5.4 prohibits them from co-venturing with anyone except other licensed lawyers.

In contrast, the L2L space has much greater latitude, and hence the more vivid color bars. This difference is traceable to the view, accepted many years ago by bar officials, that companies with nonlawyer owners are not engaged in the practice of law if they sell their legal services to a client with at least one in-house or law firm lawyer who can supervise the work. See ABA Formal Opinion 08-451, “Lawyer Obligations When Outsourcing Legal and Nonlegal Support Services,” Aug. 8, 2008 (providing ethics compliance roadmap for outsourcing of legal work). Thus, law companies in the L2L section — roughly 70% of the total legal services market — have access to outside capital from PE/VC funds or public capital markets. This is also how the Big Four accounting firms are entering the US market.

Hopefully, liberalization efforts in California, Arizona, Utah, and elsewhere will result in changes that incentivize the creation of a vibrant one-to-many sector focused on PeopleLaw. What’s needed are ethics rules that (a) enable lawyers to collaborate with allied professionals as co-equals and (b) permit the raising of equity capital sufficient to reach scale. For the latest developments on this front, see Jayne Reardon, “Re-regulating Lawyers for the 21st Century,” 2Civility, July 18, 2019.

The remainder of this post, however, is focused on the much larger L2L sector. Although changes to Rule 5.4 might materially change the composition and dynamism of this sector, the higher stakes and more affluent client base ensure that the L2L sector will evolve in the direction of more one-to-many legal solutions. Along the way, this will increase the relative mix of allied professionals, with many eventually achieving the functional equivalent of equity partner, at least in terms of status, influence, and pay. That said, the profession and industry would benefit from a straighter path forward.

One apology in advance: the supply chain analysis below is very lawyer-centric. We are headed into a future where licensed lawyers will be a subset of a larger group of legal professionals. Some of these professionals will have JDs, but the rest will have a varied set of educational credentials. Purely for ease of illustration, however, I focus on the supply of talent attempting to enter the profession with a traditional three-year law degree.

4. Bespoke lawyering: still important, still profitable

It’s important to get this fact onto the table: Bespoke lawyering is destined to remain a vital part of the legal economy. That said, let me be clear — this is a statement about areas of legal specialization; it is not a comment on the viability of the traditional large law firm model, which is headed for some challenges in the years ahead. See, e.g., Post 055 (discussing these ideas in context of David Cambria’s move from ADM to Baker McKenzie).

On the Human Capital Map, most of the Type 0 innovation is occurring in the top right (medium/dark blue), which is lawyers serving relatively large organizational clients. Type 0 innovation requires a sound legal education in substantive law combined with practice experience in highly specialized areas of law. Many current law students hope to land in this career track, as the entry-level salaries remain high, thus ensuring their ability to comfortably service their law school debt.See NALP Salary Distribution Curves (approximately 4,000 students from class of 2018 beginning careers in firms paying $180k-$190k starting salaries).

5. Challenges to traditional large law firm model

The continued importance of Bespoke lawyering for Type 0 work does not create a permanent safespace for the large law firm sector (the NLJ 500), which services more than half of the total legal services market (from privately held companies with a solo GC to Fortune 100 businesses with 50-person legal ops teams). Indeed, other changes in the legal industry are placing enormous pressure on the traditional partner-associate staffing model.

The most significant change is the divergent hourly rates for legal work in emerging and growth areas of law (Type 0 innovation) versus legal work in mature and saturated areas. Although highly specialized Type 0 legal work commands premium rates–which law firm management loves–there remains a massive volume of “run-the-company” legal work in the mature and saturated parts of the Lifecycle graphic.

Large law firms can retain run-the-company work by investing in Type 1 innovation. In my view, there are three reasons to do so:

- Higher profit. Type 1 innovations can result in portfolios of relatively high-margin work performed by non-partner (i.e., non-owner) personnel. In many cases, the margins will be higher because of the connection to firm’s Type 0 reputational capital.

- Institutionalizing clients. The value-add here is being a general contractor who can be trusted to bundle and perform work at the best mix of cost and quality. Yet, once a client becomes wedded to a firm’s Type 1 innovation (a mix of data, process, design and tech), it becomes harder for them to switch firms. This reduces a firm’s reliance of partners with portable books of business.

- Talent supply chain advantages. As discussed below, lawyers who can do Type 1 innovation require the same foundational knowledge as lawyers who do Type 0 innovation — both need to understand the substance and economics of run-the-company legal work. Yet, run-the-company work would seem to be the best starting point for learning the fundamentals. When partners turn up their noses at more rate-sensitive work, they create challenges to replenishing their talent.

That said, at least in the US market, when it comes to the factor 3 talent supply chain advantages, the transition is much more complex.

The biggest challenge is that law firms would prefer that clients pay for associate training. Yet, because law firms continue to pay exorbitant entry-level salaries ($180k-$190k with modest adjustments in smaller markets), associate billing rates are wildly out of step with their skill set. As corporate clients resist paying for first- and second-year associate talent, fewer entry-level lawyers get hired, which in turn affects the overall supply of experienced junior talent within the industry; and also the number of applicants applying to law school. See Post 060 (discussing trendlines). The interdependencies between clients, law firms, and law schools are what social scientists call a “complex system.”

A second complexity is that Type 1 Innovation requires more than just legal knowledge. To create scalable one-to-many legal solutions, one also needs a basic working knowledge of various allied disciplines, such as those represented in the rainbow section of the Human Capital Map. However, practice mastery in other disciplines is not the goal. Rather, what is required is enough working knowledge to be an effective, respectful collaborator.

Why is this important? As a group, lawyers in private practice know so little about the fields of marketing, organizational development, data science, etc., that they are unable to effectively receive and incorporate good advice. Instead, they “play it safe” by copying the practices of peer firms. The way to break out of this cycle is to ensure that your junior personnel learn the fundamentals of other disciplines early in their careers (and let them marinate). Opportunity cost for learning goes up with billing rates and production quotas. By installing a multidisciplinary perspective early, personnel avoid the trap of become too expensive to train; they also become more creative sooner.

The right side of the graphic below, which is the Human Capital Map limited to large organizational clients, illustrates the breadth of perspectives needed.

6. The Type 1 Innovation lawyer

A good example of the expansive skill set of a Type 1 Innovation Lawyer is Jason Barnwell, a CLOC Board Member and Assistant GC of Legal Business, Operations, and Strategy at Microsoft. In his “Bricklayers and Architects” essay, Barnwell, who worked as a software engineer before going to a law school, discusses his surprise at the technological backwardness of the two law firms where he began his career — in particular, the large volume of associate work that was ripe for automation.  Nonetheless, Barnwell soldiered on for two more years to “sharpen my lawyer knife” and become a “minimum viable lawyer.” See Post 080. According to Barnwell, he could not do his job today without this MVL training.

Nonetheless, Barnwell soldiered on for two more years to “sharpen my lawyer knife” and become a “minimum viable lawyer.” See Post 080. According to Barnwell, he could not do his job today without this MVL training.

A second example of the expansive skill set of a Type 1 Innovation lawyer is Eric Wood, who is Practice Innovations and Technology Partner at Chapman and Cutler. As discussed in Post 039 on law firm intrapreneurship, Wood was five years into practice as an associate when he decided to use his technical skills in database construction and coding (which he acquired to excel in his fantasy basketball hobby) to embark on a career in legaltech.

Sensing an opportunity, however, Chapman Chief Executive Partner Tim Mohan immediately took Wood off client billable work so he could focus on various automation projects (and eventually products). A few years later, Wood was promoted to partner. More recently, Chapman’s closing room technology, which was a project headed by Wood, was sold to NetDocuments. See Caroline Hill, “Chapman and Cutler: Sale of Closing Room to NetDocuments could just be the start,” Legal IT Insider, Nov. 12, 2018. Obviously, Chapman and Cutler is at the forefront of one-to-many legal innovation. Yet, it is very telling that, according to Wood, his five years in practice was “the absolute minimum” amount of substantive practice experience he needed to perform his current job at a high level.

These two data points illustrate the more fundamental point, however, that the career path for Type 1 innovators is largely a series of unusual, relatively random path dependencies. If one-to-many legal solutions are important to ordinary people (in L2C) and important to the business models of the next generation of law firms (L2L), doesn’t it make sense to build a high-quality, reliable legal talent supply chain?

7. Constructing a better legal talent supply chain

When I discuss how to make a better legal talent supply chain, it makes sense to clearly define the content of “better.” Thus, I offer three desirable outcomes.

- Increased production. A better legal supply chain would increase the quantity and diversity of young people who are get the requisite experience to become minimal viable lawyers (MVLs). As discussed in detail below, features of the current market restrict the production of MVLs in ways that inhibit diversity and reduce the supply of both future Type 0 and Type I innovators. This needs to be fixed.

- Lower risk for law students. A better legal supply chain would provide greater clarity and certainty to young people signing loan papers for a very expensive graduate education. Through collaboration between law schools, legal employers, and large organizational clients, it is possible to reconfigure legal education and legal internships in ways that drive down the total cost of education, increase the quantity and quality of on-the-job training, and provide a relatively clear pathway to desirable post-grad employment.

- Reliable source of entry-level talent for employers. A better legal supply chain would deliver a reliable, diverse supply of talent that comes at a price point where clients and employers can share the cost of on-the-job training, including meaningful immersion in the fundamental of allied disciplines.

The only way to achieve these outcomes, however, is through some type of intentional cooperation/collaboration among stakeholders in different parts of the supply chain. Without such enlightened risk-sharing, we are stuck with some very difficult market coordination problems that make everyone worse off.

8. The primary structural bottleneck

The primary structural bottleneck is a hangover from the pre-recession go-go days that created the current BigLaw sector. Simply put, entry-level lawyers are paid a wage that makes them too expensive for foundational training in key allied disciplines (what’s needed for Type 1 Innovation). And relatedly, these high entry-level salaries ripple throughout the law firm, thus inflating their cost structures and causing clients to look for credible substitutes, particularly for lower-risk run-the-company legal work.

This structural bottleneck manifests itself in two ways. First, as shown in the graphic below, large organizational clients have gone on a prolonged 20-year hiring binge.

Remarkably, there are now more lawyers working in-house (106,000) than are working in the domestic offices of AmLaw 200 law firms. Further, since the great recession, the growth rate of lawyers in private practice lags behind the government sector. This should worry those of us in legal education, as the math of legal education does not add up without the engine of relatively well-paying jobs in private practice.

The rise of in-house lawyering is partially justified based on the growing number of very large organizational clients. See Post 067 (data showing that large corporations are growing significantly faster than broader economy). Thus, it makes sense to have more lawyers who are both physically and psychologically proximate to the client, which in a large organization is a business unit served by a legal department. Nonetheless, cost savings is undoubtedly a major driver of legal department insourcing, as the cost of paying a law firm associate is roughly 3x a fully loaded in-house lawyer . See, e.g., Simon & Passarella, “The Rise (and Fall?) of In-House,” Corp. Counsel, Oct. 24, 2018 (noting enduring cost differential between in-house and law firm lawyers and that roughly 45% of the AmLaw 100 were performing the type of work that could generate a 2x financial return if brought in-house).

Yet, here is the rub for legal talent supply chain: Despite all this insourcing of legal work, almost no legal departments hire directly out of law school, instead looking to the associate ranks of law firms as their primary source of talent. When this is combined with the pervasive practice of clients refusing to pay for first- and second-year associate work, we have the second manifestation of a structural bottleneck: an industry-level constriction in the volume of entry-level talent who are on path to become a “minimum viable lawyer.”

Evidence of industry-level constriction is presented in the graphic below, which shows the number of entry-level lawyers entering private practice during the 2007 to 2018 time period.

These trend lines show the anemic state of our current legal talent supply chain. The direct consequence of this weak supply chain is significantly smaller cohort of legal professionals best positioned to become leaders in Type 0 (substantive law) and Type 1 (one-to-many) Innovation. Rather than making a large investment in the next generation, the largest law firms and legal departments are, as a group, leaning more heavily on already-trained senior talent. Where is the leadership?

As a profession, here are three laudable goals that virtually everyone can get behind: (1) diversifying our ranks, (2) bridging generational divides, and (3) developing talent that can bring clients the benefits of one-to-many legal solutions. What’s the likelihood we will get there without some coordination on a legal talent supply chain?

9. Fixing the bottleneck

At present, the best coordination device among large law firms is a shared desire to play at the top of market. Therefore, because starting salaries are transparent to the market, virtually all firms fall in line with the median starting salaries. This amount is now $190,000 (up from $160,000 in 2007). It’s also a wage that clients have rejected as too high. Nonetheless, until a subset of the market comes up with a better model that creates a clear commercial advantage, we’re effectively stuck in a prisoner’s dilemma that causes us to forego smart, long-term investments in talent.

In my view, the best way to precede is for a small group of innovator/early adopter law firms, opinion leader clients, best-in-class law companies, and law schools to collaborate on a legal talent supply chain pilot that focuses on higher quality training at a point in time when law students are worried about their future job prospects and are not expecting to paid top-of-the-market wages.

Below is a high-level description of how this might work.

- Pilot group. Five leading clients, five law firms, two law companies, and several law schools will come together with the law schools agreeing to grant academic credit for paid work during the 3L year (something now permissible under the ABA-accreditation standards, see Karen Sloan, “ABA Approves Pay for Law Student’s For-Credit Externships,” Law.com, Aug. 8, 2016). From the schools, we recruit approximately 75 students who want guaranteed employment before graduating from law school. We screen the students using a standardized interview process that evaluates initiative, problem-solving, teamwork ability, and communication skills. We also commit to a relatively high level of diversity (which will not be hard, see Post 118). By involving multiple stakeholders, we have safety in numbers. Further, the participation of five leading clients provides cover for the law firm leaders who have to push this through internally.

- Two-year training program. Develop a two-year training program that spans the 3L year of law school and first year of practice, with a window built in to take the bar. During this time period, students are paid a training wage of $80,000 during the 3L year and $110,000 in year 1 of practice, which nets out to $190,000 over two years (so no student is being asked to take a financial hit). Part of the training is a rotation system that embeds students with clients (to learn business and the client perspective), with law companies (to supercharge them on data, process, technology, and design), and law firms (to get exposure to the most complex and cutting-edge areas of law).

- Compare the results. The size of this pilot is not large enough to replace a law firm’s entering class of associates. Thus, beginning in the second year of practice, we compare the subsequence performance of the pilot graduates with the second-year associates (in essence, a control group). Further, we ask clients for their feedback. If the pilot is successful, we scale it to increase the supply of better-trained, more diverse early career lawyers. We also carefully track the career progression of each wave of graduates so the benefits of the program can be fully measured and quantified. In the program works, it will produce leaders in both Type 0 and Type 1 Innovation.

- Institutionalize and scale the program. If the pilot is successful getting law students high-quality paid employment, there will be no shortage of law schools seeking to plug into the model. Likewise, by opening the aperture to a wide range of law schools, it will be much easier to build a diverse cohort of students, as the vast majority of diverse law students don’t attend elite law schools. See Post 114 (Evan Parker reporting diversity pipeline numbers broken down by US News tier). If law firms are getting a better, more reliable, and more diverse supply of talent, the industry begins to tip toward a new model that expands to include other sectors (e.g., government, public interest) and market segments (most urgently, PeopleLaw). We have to start somewhere.

The key to getting this pilot off the ground is five opinion leader general counsel who acknowledge the supply chain problem and are willing to throw their pro bono time and reputational capital behind a credible pilot to solve it. If the pilot works, we roll the snowball. Per the three metrics discussed above, the “better” legal talent supply chain delivers (1) more production of talent, (2) lower risk for law students, and (3) a more reliable source of talent for legal employers.

We have a golden opportunity to reset our industry. It’s time to see who we really are.