Big corporations are growing faster than the rest of the economy. It is not hard to figure out where this is going. Lawyer acceptance is different story.

Many lawyers and law firms claim to serve the middle market, often describing how they deal directly with owners and executives rather than in-house counsel. Although these clients aren’t the Fortune 500, the lawyers and law firm leaders take enormous pride in this type of practice and discuss it in ways that suggest it’s a stable and permanent market niche. I’m not sure that’s right.

Above is a treemap chart of U.S. businesses grouped by annual revenue. The key takeaway is that $100M+ companies comprise the vast majority of U.S. business activity (71.6%). Remarkably, all this purple is generated by 22,400 businesses, a mere 0.4% of the 5.7 million businesses in operation in the U.S. in 2012 (the most recent year that contains total receipts).

Companies in purple tend to have legal departments as do a meaningful number of companies in orange (>$25M-$100M). We can deduce this from a number of sources. For example, according to the Legal Executive Institute, companies with less than $1 billion in revenue were classified as “small.” See 2018 State of Corporate Law Departments at 10. Yet, these companies had, on average, nine in-house lawyers, or one attorney per $65M in revenue. Likewise, a 2016 report by Barker Gilmore, a national recruiting firm, classified companies into four groups: >$10B, $1B-10B, $100M-$1B, <$100M. Yet, even in the smallest category (<$100M), there were sufficient data to calculate separate salary, bonus and equity averages for three different in-house roles: general counsel, managing counsel, and senior counsel. See 2016 In-House Counsel Compensation Report at 14-22.

Defining “middle market” turns out to be surprisingly difficult — is it somewhere in the purple? The orange? The gold? The managing partner of a successful firm near the bottom of the AmLaw 200 recently told me that all his partners agreed that the firm served the middle market. Yet, that consensus broke down during a strategic planning process when partners were asked to define middle market using specific criteria. Finally they gave up. The firm was still middle market, but each partner was free to follow his or her own definition.

Although consensus on the middle market is bound to elude us, not everything is so ambiguous. This Post addresses two interrelated topics regarding the future of law:

- The Journey to Big. Large corporations are the fastest growing segment of the U.S. economy. This trend started several decades ago and will continue into the future.

- How Big affects the practice of law. Once one sees and accepts the journey to Big, several consequences for the practice of law come quickly into focus.

Journey to Big

Every day the global economy becomes a little more interconnected and complex. In contrast, our mental models for the practice of law are very sticky. This is because we need common, coherent and tractable mental models to coordinate organizational goals and effort. Thus, we only change our mental models when they become a source of competitive disadvantage, essentially pitting the pain of building new models against the pain of imminent failure.

The middle-market law firm discussed above is in that uncomfortable in-between state where the need for new mental models is building but the organizational benefits of such a change remain out of focus. This likely describes most lawyers and law firms.

Below are charts regarding the more rapid grow of large businesses. Yet, these data are supported by our own intuition if we take a moment to reflect on the enormous advantages that accrue to very large companies. These include:

- Significant economies of scale and scope, which translate into cost and pricing advantages

- Portfolios of familiar brands that send signals of quality and value

- A plethora of low-cost sales channels they either control or can readily influence

- Ample cash on hand to develop new products and services

- If internal R&D fails, the financial resources to acquire smaller, more innovative competitors

If you’re wondering how important large companies are to the overall economy, review your credit card statement or the bills you pay online each month, such as your mortgage, car payment or student loans.

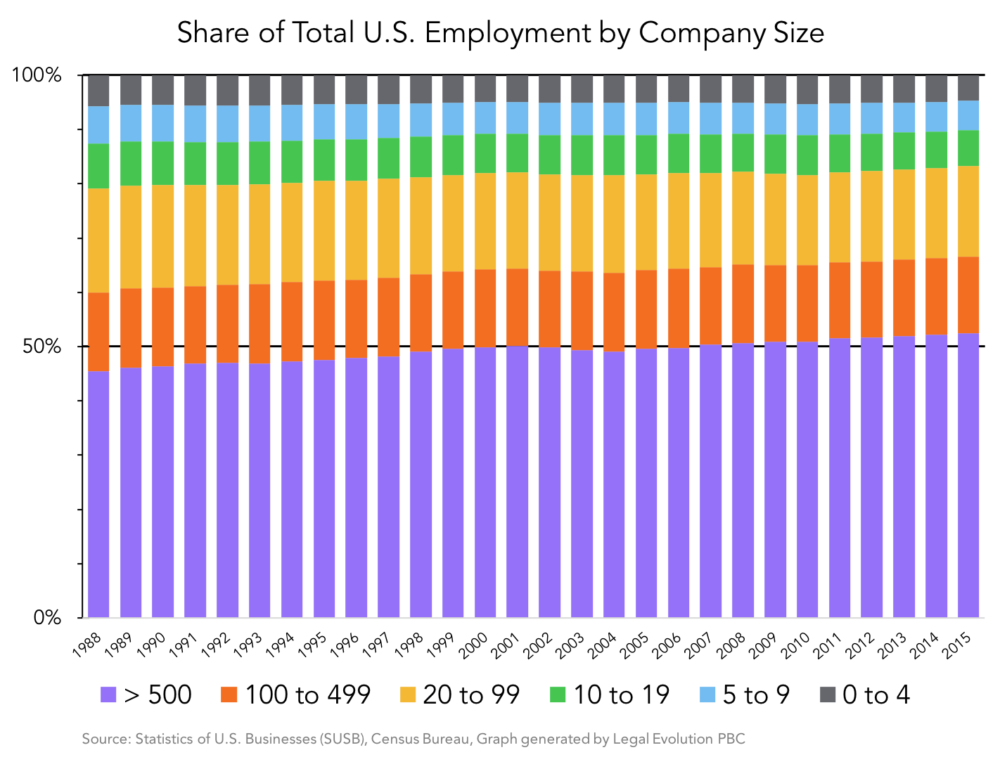

The graphic below shows how the mix of U.S. employment is steadily shifting to companies with large employee headcounts.

Companies with 500+ employees (purple bars) comprise the largest category in the SUSB data. This is the only group growing in proportionate size, increasing from 45.4% of total US employment in 1988 to 52.5% in 2015. If the change looks quite subtle, that’s also it’s experienced — so gradual it’s barely noticed. This makes it more difficult to keep our mental models up to date.

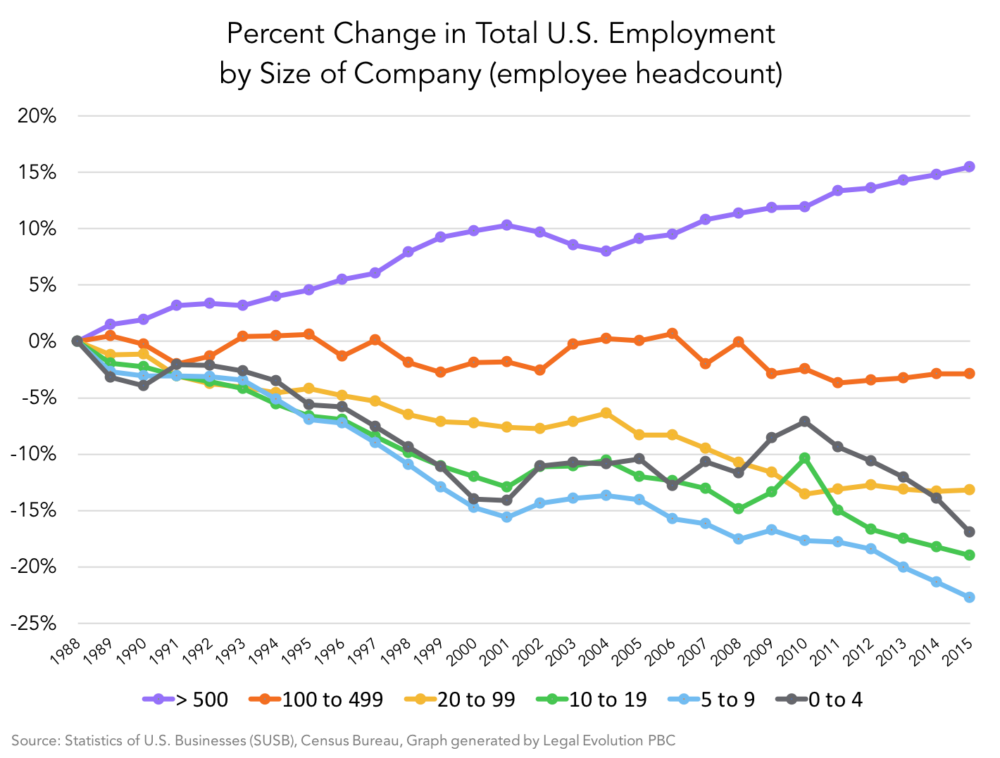

The magnitude of the change is easier to observe through a trendline analysis that starts with 1988 as baseline:

The absolute numbers underneath the purple trendline are striking. Between 1988 and 2015, the total number of companies with 500+ employees increased from 12,800 to 19,500. The total number of employees in the 500+ company category increased from 39.9 million to 65.1 million. Further, total payroll for these companies increased from $958 billion (51.4% of total US payroll) to $3.7 trillion (59.2%). Purple companies, by dint of their sheer size and scale, generate substantial and ongoing legal work for lawyers. Thus, they are very desirable clients for law firms.

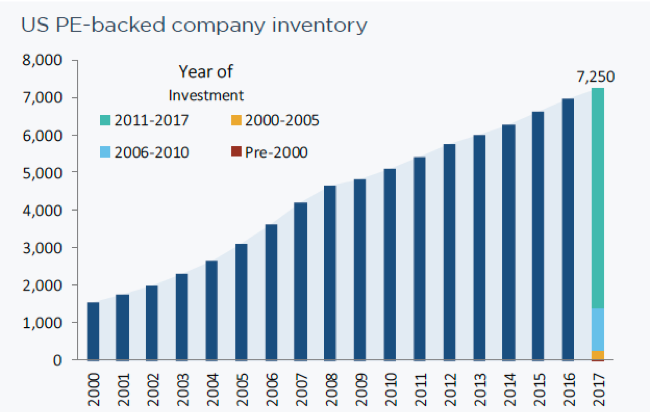

Finally, the trend toward bigness is compounded by the growing portion of purple, orange and gold companies that are partially or wholly owned by private equity. Below is graphic showing an annual count of U.S. companies in private equity-backed portfolios.

In our journey to Big, more and more successful businesses with regional roots are becoming assets in multi-billion dollar private equity funds. According to a recent McKinsey report, even the largest funds ($5B+) are growing faster than the rest of the PE market, increasing from 5% market share in 2010 to 25% in 2017. See “The rise and rise of private markets,” McKinsey Global Private Markets Review 2018 at 14 & Exhibit 9.

What makes all of these trends so powerful is (a) they are all moving to Big and (b) the pattern is near certain to continue. Alas, this is the path of globalization.

How Big affects the practice of law

Once we accept that the legal industry is on a journey to Big, several predictable consequences come into focus. In this post, I’ll discuss three.

1. Legal departments are law firms with structural features that favor efficiency and innovation. Thus, they are taking market share.

Our journey to Big produces legal departments that are comparable to AmLaw 200 law firms or specialized boutiques. Yet, legal department “firms” have several features that favor efficiency and innovation.

To illustrate this point, consider the statistics below from a recent CLOC survey of 156 member legal departments.

|

Large Companies ($10B+) |

Mid-Size Companies ($1B-$9.9B) | Small Companies (< $1B) | |

| Avg. attorney headcount | 188 | 41 | 9 |

| Avg. legal ops headcount | 21 | 6 | 1 |

| Avg. attorney to revenue ratio | 1 / $585M | 1 / $195M | 1 / $65M |

| Avg. internal spend per legal dept FTE* | $225K / FTE | $236K / FTE | $175K / FTE |

| * Legal Dept. FTEs include attorneys, paralegals, legal ops professionals, administrators, and all other members of the department. | |||

Although the per-FTE cost of staffing a legal department appears to be higher in large and mid-size departments ($225-$236K vs. $175K), it hardly matters because the overall cost structure of legal departments gets significantly lower with size, moving from one attorney per $65M (small company) to one attorney per $585M (large company).

Part of the declining cost structure is economies of scale that apply equally to in-house and outside counsel. For example, the legal work for a loan or other type of financing is not ten times more labor-intensive because the monies raised are ten times larger. Yet, another part is surely greater operational efficiency. The larger and more mature a company, the more it must rely upon lower per-unit costs to meet its financial targets. We see this in the CLOC survey above. When asked to identify their department’s top priorities, the top response was “Controlling outside counsel costs” (76%) followed by “Using technology to simplify workflow and manual processes” (41%). See 2018 State of Corporate Law Departments at 8-9.

Although law firms and legal departments may be doing very similar work, their internal incentives run in opposite directions. Most law firm partners are strongly incentivized to maximize the revenue, either through originations or working receipts. Likewise, high-billing partners can stifle innovation and efficiency measures by threatening to leave the firm. In contrast, when a general counsel commits to similar initiatives, in-house lawyers have limited leverage to push back.

A recent American Lawyer article by Hugh Simons and Gina Passarella modeled the financial cut point for bringing work in-house. See “The Rise (and Fall?) of In-House Counsel,” Corp. Counsel, Feb. 25, 2018. According to their analysis, roughly 45% of the AmLaw 100 were performing the type of work that could generate a 2x financial return if brought in-house. In asking how far insourcing might go, the authors offered a startling benchmark: “70 percent of accountants and auditors work in-house.”

Cost, however, is not the sole reason to insource. In-house lawyers have an enormous advantage in acquiring essential knowledge regarding client goals and needs. This physical and organizational proximity reduces communication overhead and creates conditions where legal work can be better defined, scoped and managed. As a result, some of the insourced legal work will eventually be outsourced again, but this time to lower-cost NewLaw service providers.

2. Specialized tranches of work go to law firms and other service providers

Although the journey to Big leads to in-house “law firms” that become very good at process and efficiency, there remains a significant class of work that, for reasons of cost or quality, will continue to go to law firms. What are the criteria for these decisions?

Below is a graphic that Mark Chandler, the GC of Cisco, showed during the final plenary session of the 2018 CLOC Institute:

The top-right quadrant consumes 65% of the department’s internal resources. The high percentage is warranted because (a) these are mission-critical activities that (b) bear on the competitive advantage of Cisco, a $48 billion technology company that manufactures and sells networking hardware, telecommunications equipment and other high-technology services and products.

The second biggest area of internal resource allocation (20%) is the bottom-right quadrant, which enables business units to more efficiently conduct their activities in a legally appropriate way. Note, however, that “Tools/Processes” are in every quadrant, not just in the self-service green. That is the result of Cisco’s very advanced legal ops function led by Steve Harmon.

Law firms are mostly likely to get work from the left side of the matrix. The work in the top-left pays the most because it is mission critical and Cisco’s in-house staff lacks contextual knowledge to perform the work at the necessary level of quality. Nonetheless, 15% of the department’s resources are dedicated to managing out-tasked work. This is to ensure that the department achieves its cost and quality objectives. The goal in the bottom-left is to lock-in a combination of quality-cost-reliability for low-stakes matters. The best outcome is one that require little to no department oversight.

Under this type of decision matrix, traditional law firms have two clear paths for winning work:

- Be best-in-class in an area of law that is mission critical. Cf. Henderson & Parker, “The Five Strategies of Highly Effective Firms,” Am. Law, Jan. 2017 (statistical model showing that practice area specialization is the single most important factor in law firm profitability).

- Be outstanding at doing volume legal work. Cf. Henderson & Parker, “Your Place in the Legal Market,” Am Law, Dec. 2015 (discussing how three firms climbed into the AmLaw 100 by focusing on price-sensitive labor and employment work).

Some law firm partners might dismiss Cisco’s resource allocation matrix as this year’s gimmick. That’s wrong for at least two reasons. First, Cisco has been using this system for 12+ dozen years. I first saw Chandler present a 1.0 version of this model at a 2010 Georgetown Law conference. That slide was dated 2006. Second, this type of resource allocation matrix was featured in a 2018 CLOC Institute session taught by Nancy Jessen (SVP of Legal Business Solutions at UnitedLex) and Elizabeth Lugones (Dir. of Legal Operations, DXC.technology). See DCX-UnitedLex allocation matrix. This session was attended by roughly 300 people. The presenters, however, are innovators or early adopters. See Post 007 (discussing adopter types). The success they were sharing is what other professionals in the social system will to try to replicate. This is how innovation diffusion works. See Post 004 (innovation diffuses through social systems).

3. In the long-term, there is no middle market

Because the journey to Big is a very gradual process, it’s easy to confuse slow change with no change. Further, there is a generational effect, with both buyers and sellers of legal services sticking with what they know until external events force them to change. It’s certainly true that a no-change approach will work many lawyers in the last decade or so of their careers.

I have never met a law firm partner who told me that he or she planned to ride out the clock rather than adapt to changing times. Instead, I hear a lot of lawyers 50+ years of age tell me their “middle market” clients just want excellent service at a cost-effective price. These lawyers continue to stay busy, or busy enough, because there is demand for what they offer: (1) a personal relationship with a knowledgeable, responsive lawyer who makes difficult legal business issues go away (2) at rates that do not carry the expense and overhead of AmLaw 50 or Global 100 law firms.

Many lawyers like this type of practice because it puts them in control, giving them autonomy and security within their firms. They don’t have to collaborate with anyone if they don’t want to. Arguably, when the business world was itself more middle market and less influenced by private equity, this described the bulk of private law practice. Less so now. And less so in the future as economic activity is increasingly driven by larger, more complex organizations that have the resources to build out their own sophisticated legal departments.

Strategy and the Fat Smoker (2008) was the last book David Maister, the preeminent law firm consultant, wrote before he retired. Maister starts Chapter 17, titled “The Trouble with Lawyers,” by conceding the point that lawyers are, in fact, different. “The combination of a desire for autonomy and high levels of skepticism,” wrote Maister, “makes most law firms low-trust environments” (p. 231). Thus, according to Maister, firms struggle to execute on strategies that require collaboration and sharing of risk.

If this is true, why do most firms do so well financially? Maister opines that it’s because lawyers “compete only with other lawyers. If everyone else does things equally poorly, and clients and recruits find little variation between firms, even the most egregious behavior will not lead to a competitive disadvantage” (p. 239).

This passage invariably garners a good laugh among lawyers, but less so in the future. Law firms inside large legal departments increasingly rely on systems and process. Likewise, to capture a tranche of the legal work that is sourced using a resource allocation model, some law firms are executing on a strategy that requires collaboration and risk sharing. Although most firms struggle with this approach, a firm only has to do marginally better to win. This is because the most able mid-career lawyers will eventually lateral out of firms unable to offer anything beyond a pledge of great service.

As discussed in Innovation in Organizations, Part I-III (015, 016, 017), firm size is correlated with innovation, not because of size per se, but because size brings with it specialized expertise, financial resources, and better access to a diverse stream of clients. Cf. Post 062 (Jae Um discussing how innovation require high-quality access to buyers and users). Further, the service offerings of marginally more innovative firms are destined to create value that is controlled by the firm, reducing the tyranny of partners with portable books of business. As portions of this legal work get productized, middle market lawyers will have very little left to sell. Thus, as it turns out, the middle market is but a waystation on the journey to Big.

Coda. The journey to Big has significant consequences for entry-level law graduates and thus legal education. But that is a topic for another day.

What’s next? See Can Microsoft hit “refresh” on client-law firm relations? (068)