Are you a mid-market firm worried about the cost and risk of innovation? UnitedLex is offering a turn-key solution.

By any objective standards, equity partners working in AmLaw 200 firms are rich. Even firms at the lower end of the profitability scale are filled with 1-percenters ($481,000+ per year). So why, then, do law firm leaders complain about lack of access to capital to finance much needed law firm innovations?

Based on recent news, we can ask the question another way: Why do we need a entity like UnitedLex’s ULX Partners to bear risk for a firm like LeClairRyan (325 lawyers, 25 offices)? See Rozen, “UnitedLex and LeClairRyan Announce Innovative New Law Venture,” Law.com, June 13, 2018.

Many of us struggle to answer this question, at least succinctly, because we start with the assumption that large law firms are unified businesses. But that’s not quite right. Law firms have revenues because partners are out there hustling work, typically by selling a combination of personal expertise and responsiveness. Partners who have built and managed a decent-sized practice know they need IT, office space, associates, support staff, and even marketing, if only to respond to RFPs. Yet, partner books are often an idiosyncratic mash of clients that vary widely by industry, price sensitivity, legal spend, and appetite for change. See Post 048 (clients vary by size and adopter type, making generalizations hard); Post 013 (same).

At a practical level, this means that firm leaders struggle to explain to partners why a meaningful slice of profit needs to finance “innovations” that are (a) relevant to only a subset of clients, and (b) require partners to learn and change. If law firm leaders push the innovation envelope too far, big-producing partners might leave. So here is the answer to our question: Law firms need capital because their own partners are reluctant to pony up, at least in the quantity needed to compete with VC- and PE-backed NewLaw companies.

Despite these challenges, a surprising number of law firms are going down the innovation road–~10-15% of the AmLaw 200. If I were a law firm leader who had successfully sold such a plan to my partners, I would be worried that the P3 professionals (pricing, project management, process improvement) we worked so hard to find and train will get poached by competitors. Cf. Henderson & Zorn, “The Most Prized Lateral Hire of 2015 Wasn’t a Partner,” AmLaw Daily, Feb. 1, 2016 (discussing poaching of four-person P3 team from BLP to Herbert Smith Freehills). Of course, if I failed to sell such a plan, I would be worried that I was presiding over a hotel for lawyers (a two-star hotel at that).

These are very serious challenges to manage. It’s also the problem that ULX Partners is designed to solve.

Deep bench

This post is being written on the last day of the ACC Legal Ops conference in Chicago. During one of the sessions earlier this week, I heard a legal department ops professional advise his peers that “it’s a good idea to engage with the law firms’ price and project management professionals” because “these folks are also doing legal ops, but from the law firm side.” Others in the room agreed. This is evidence that a true sea change is taking hold.

Yet, I have been a regular attendee at these ops conferences, and often the most expert panelists work at NewLaw providers, with UnitedLex and Elevate typically jockeying for the pole position. These companies have the largest and deepest bench of seasoned legal ops professionals. And because these companies are not law firms, lawyers and allied professionals work together as co-equals in terms of status, bonus, and equity. Consistent with Clayton Christiansen’s disruptive innovation, these companies started with rebar (e-discovery) but are now climbing the value ladder toward high-grade steel (strategic work on par with bespoke practitioners).

For many years, CEO Dan Reed has been hinting that UnitedLex is on the path to become something like Accenture, but pointed at the corporate legal services market. To made that a reality, however, UnitedLex has to reconfigure (disrupt or dis-intermediate are too strong a word) the traditional client-law firm relationship. BigLaw has tremendously valuable client relationships. However, much to the disappointment and frustration of the legaltech world, those relationships are almost never used to introduce clients to innovation by third-party companies. See Post 025 (discussing law firms as failed distribution channels for legaltech innovators). Thus, most NewLaw providers focus primarily if not exclusively on legal departments.

For many years, CEO Dan Reed has been hinting that UnitedLex is on the path to become something like Accenture, but pointed at the corporate legal services market. To made that a reality, however, UnitedLex has to reconfigure (disrupt or dis-intermediate are too strong a word) the traditional client-law firm relationship. BigLaw has tremendously valuable client relationships. However, much to the disappointment and frustration of the legaltech world, those relationships are almost never used to introduce clients to innovation by third-party companies. See Post 025 (discussing law firms as failed distribution channels for legaltech innovators). Thus, most NewLaw providers focus primarily if not exclusively on legal departments.

Why do we need a legal structure like ULX Partners?

The short answer is that partners need a way to co-venture with highly talented allied professionals without running afoul of Rule 5.4, which prohibits lawyers and nonlawyers from sharing ownership interests in a business that is engaged in the practice of law.

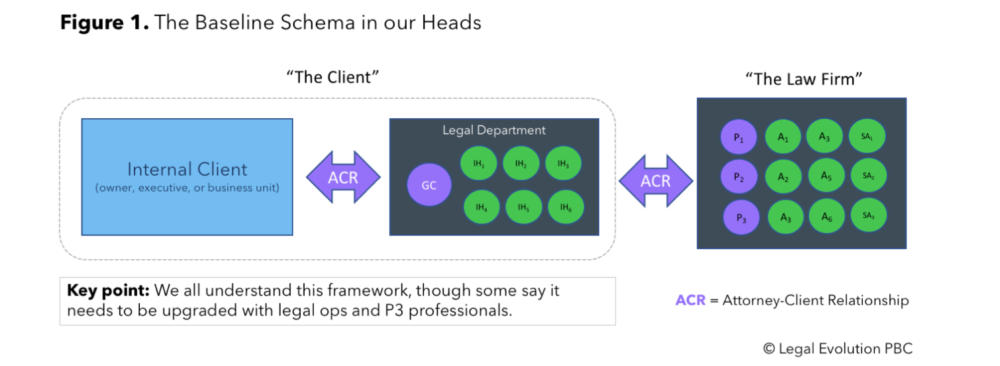

The figures that follow are designed to show how 5.4 shapes, but hardly prevents, how capital finds opportunity in the legal market. We start with Figure 1, which reflects the familiar schema that is in our heads. If we innovate, we are innovating to change this baseline model. By the way, the baseline model is much more powerful than some might realize, as it reflects the status quo. More on that latter.  Figure 2 reflects a configuration that is starting to take shape. If you were at the ACC Legal Ops conference or at CLOC, this is likely how you view the legal market.

Figure 2 reflects a configuration that is starting to take shape. If you were at the ACC Legal Ops conference or at CLOC, this is likely how you view the legal market.

Figure 3 adds in NewLaw’s current point of entry. Note that NewLaw has lots of lawyers along with allied professionals. Because its core business is legal ops / P3, NewLaw invests a lot in vetting technology, building sophisticated workflows, and measuring with data. Most legal departments and law firms can’t keep up with this level of sophistication. NewLaw, however, can’t engage in the practice of law. So, as a workaround, lawyers — usually in purple but sometimes in green — have to “supervise” them.

Figure 4 shows what Accenture’s legal vertical would look like but for Rule 5.4.

Thus, Dan Reed and others need a workaround. Figure 5 is a depiction of the ULX Partners configuration.

The UnitedLex-LeClairRyan initiative will conduct its business through an entity called ULX Partners, LLC, a Delaware Limited Liability Company with several subunits organized other the laws of Florida, California, Massachusetts, Virginia, and the District of Company. This structure has surely been set up so that no ULX Partner revenue accrues from the practice of law–i.e., no ULX employee will be signing pleadings, making appearance on behalf of clients in court, writing opinion letters, or negotiating with regulators at the FTC, DOJ, or EPA, etc. But absolutely every other activity that occurs within a law firm, including all the pre-work done by associates, staff attorneys, and other professionals before the partner signs off, can potentially be done better, faster, and cheaper inside ULX Partners.

UnitedLex will be the majority owners. LeClairRyan will be a minority shareholder, with ULX Partners set up to take on additional member firms. The law partners will continue to manage client relationships and perform their usual work. In the meantime, ULX Partners can drive lower-cost, higher-margin engagements. To make this as concrete as possible, about 300 employees of LeClairRyan will be “re-badged” as employees of ULX Partners. Instead of issuing paychecks to these folks, LeClairRyan will pay a service fee to ULX. If this workforce gets supercharged through UnitedLex’s superior legal ops capabilities, LeClairRyan will share in the upside as a ULX owner.

Capitalists and regulators

The configurations above (and in the appendix below) were predicted back in 2010 by Nick Baughan, a managing member of Marks Baughan & Co, an investment bank with a specialization in legaltech.

‘If the law firms themselves can’t have outside investors, the market will continue to chip away at every part of a law firm that is not the pure provision of legal advice,’ says Nick Baughan, a managing member of investment banking firm Marks Baughan & Co., with offices in Conshohocken, Pa., and London. ‘Anything that can be provided legally by a third party will be.’

Rose, “Law, the Investment,” ABA Journal, Sept. 2010 (also quoting the late Prof. Larry Ribstein, “The question used to be: ‘Will the ABA change Rule 5.4?’ … The question now is, ‘Who cares?’”). For the last decade or so, Baughan’s firm has been running a large proportion of the major legaltech deals. So if this feels new to you or me, it’s old news to the professional investors tracking the legal sector.

Now that the market has shifted in a way that could really disrupt traditional law practice, it’s possible state bar regulators will interject themselves into these more aggressive NewLaw structures. This has long been a risk factor in NewLaw PPMs.

That said, regulators will have to work very hard to find a public interest rationale in Rule 5.4 or Rule 5.5 (pertaining to the unauthorized practice of law) that will contain NewLaw’s growth. These rules are grounded in a presumption of asymmetric information between lawyers and unsophisticated clients. If knowledge is asymmetric, clients have little choice but to trust lawyers. Thus, under this policy rationale, lawyers as a group must be completely independent. Obviously, this asymmetry does not exist in large corporations with legal departments comprised of former BigLaw lawyers. As a result, protectionist motives dressed up as consumer protection won’t cut it. Ironically, NewLaw will have no trouble finding BigLaw lawyers willing to take their case.

All of this, however, may be premature, as ULX Partners (or related models) may not be a sufficiently large or imminent threat. As noted by Jae Um, “legal innovation is an extreme sport.” Post 051.

Why would a law firm join ULX Partners?

Well, I can think of five reasons, with higher profits being the least important.

- More Profit. UnitedLex CEO Dan Reed claims that ULX Partners will increase partner profits by 5-15%. See Strom, “Will LeClairRyan’s UnitedLex Deal Be the Accelerant Big Law Innovation Needs?“, June 13, 2018. This is certainly possible, albeit it depends upon the level of internal adoption by the lawyers inside ULX member firms. For this to have been the primary driver of the deal, LeClairRyan partners would have made business judgments based on models of future cash flows and profit margins. This is too much math and too much uncertainty for the typical line partner. I don’t buy it. Profit is, at best, icing on something else.

- Cost of innovation efforts. A credible legal ops team inside a major law firm is going to cost between 1-2% of firm revenues. There is a lot of talk that such teams will productize firm offerings and become freestanding profit centers. A few have, see Post 039 (Chapman and Cutler), and more will. But not in the first year or two. Further, there are indirect, but extremely significant, costs associated with training and change management. Through ULX Partners, UnitedLex bears the start-up costs and associated headaches.

- Risk of slow or uneven adoption. If a firm built its own legal ops team and did everything right, clients may not adopt at the rate and volume needed for a fair return. Last week, I heard a innovation officer at an AmLaw 200 firm say that his firm took the ACC’s Value Challenge seriously, making major investment in people, process, technology, and data. When shown the output, however, many clients continue to just ask for a fee discount. Cf Post 048 (corporate clients still in early adopter stage). Innovation requires clients to (a) think, and (b) think in a different way. Not all clients are ready. ULX Partners off-loads this risk to UnitedLex.

- Risk of innovation failure. A firm could expend money on its own legal ops team only to get its talent poached. Alternatively, the firm leadership could underinvest in change management, resulting in faulty execution and plummeting firm morale. “For god sakes, can’t we just sell time?”

- Focus on the practice of law. Partners excel at counseling clients, dispensing legal advice, advocating, negotiating, and developing clever solutions to knotty problems. In the past, they have been paid well for this work. If keeping it requires them to bundle in NewLaw features, they would be most grateful for low-cost, non-compulsory solutions that leave them in control of their own practice. Cf. Post 040 (describing Flaherty’s “Lawyer Theory of Value”). Most partners want to reserve their white space for things related to the practice of law. Let UnitedLex worry about everything else.

These are five very compelling reasons to ink a deal with UnitedLex. But will other firms follow suit? And if so, when? The answer to these questions is complicated.

Why did LeClairRyan go first?

LeClairRyan is not your typical AmLaw200 firm. It was founded in the mid-1980s by Gary LeClair, who specializes in venture capital businesses, and Dennis Ryan, a now-retired tax lawyer. So it is a “young” AmLaw 200 firm. Gary stepped down as chairman in 2015. But during his tenure, he was one of the most visionary and innovative law firm leaders I have ever met. He is also a person of exceptional discipline and character who attracts a large client following. Thus, Gary always had the respect of his partners even if only a few had the time and patience to digest the full sweep of his futuristic thinking.

LeClairRyan is not your typical AmLaw200 firm. It was founded in the mid-1980s by Gary LeClair, who specializes in venture capital businesses, and Dennis Ryan, a now-retired tax lawyer. So it is a “young” AmLaw 200 firm. Gary stepped down as chairman in 2015. But during his tenure, he was one of the most visionary and innovative law firm leaders I have ever met. He is also a person of exceptional discipline and character who attracts a large client following. Thus, Gary always had the respect of his partners even if only a few had the time and patience to digest the full sweep of his futuristic thinking.

One of the consequences of a decade or two of give-and-take with Gary is that LeClairRyan partners understand the shifting economics of modern practice, at least compared to other AmLaw 200 lawyers. Under LeClair, the firm did a large deal with UnitedLex around the firm’s e-discovery practice. See Cassens Weiss, “LeClairRyan opens ‘legal solutions center’ in collaboration with tech company,” ABA Journal, Nov. 1, 2013. The current CEO of LeClairRyan is Erik Gustafson, a litigator who formerly served as head of the firm’s litigation practice. For the five reasons listed above, plus a longstanding relationship of trust with UnitedLex, Erik and the firm’s executive committee were able to make business decision on par with a corporate client in a highly competitive sink-or-swim business environment.

What firms will go next?

I suspect and hope that UnitedLex gets a few other takers in the relative near term. (They will get a lot of meeting with law firms, primarily to shake them down for competitive intelligence. David Perla has an obscene term to describe this ritual. Fill in the blank: grin ____ .)

The most receptive firms would be in the NLJ 100 to 300 range with a diverse range of practices (i.e., not specialized). These firms would also need an innovative-visionary-realistic leadership team and partners who want to stay middle-market for reasons related to clients and culture. Suffice it to say, this is not a long list. If, three or four years from now, ULX member firms get their promised 5-15% return and praise from clients regarding service delivery, UnitedLex may get the early majority to tip, see Post 004, setting off rapid adoption in the rest of the social system. Dan Reed and his senior leadership team will be declared geniuses who changed everything. And they will deserve it.

However, this could play out in a different way. The most lucid account of BigLaw’s possible futures can be found in TomorrowLand by Bruce MacEwen. First among the eight competing scenarios for how the market might evolve is Chapter I, “Nothing to see here, folks; move along.” Its core point is that all noise from the blogosphere and legal press may be nothing more than Chicken Little. Through the passage of time, BigLaw proves itself endurable. If Chapter I is right, doing nothing is the wisest strategy.

However, this could play out in a different way. The most lucid account of BigLaw’s possible futures can be found in TomorrowLand by Bruce MacEwen. First among the eight competing scenarios for how the market might evolve is Chapter I, “Nothing to see here, folks; move along.” Its core point is that all noise from the blogosphere and legal press may be nothing more than Chicken Little. Through the passage of time, BigLaw proves itself endurable. If Chapter I is right, doing nothing is the wisest strategy.

Chapter II is titled, “Lawyer Psychology and the Partnership Structure Win.” In this scenario, law firms also do nothing. The difference is that “outside forces impose urgent requirements that [firms] change, but they simply cannot bring themselves to do so. This scenario, in short, is populated by firms that would rather fail than change” (p. 26).

This is a funny line. But I have spent enough time around large firm lawyers to understand how this would play out. In fact, it’s a short walk to failure:

- Should we build out our own innovation team? “No, there is too much upfront expense and risk.”

- Should we do a deal with UnitedLex? “No, there is too much brand risk.”

- Can we at least merge with another firm so we can get some economies of scale to grapple with innovation? Cf. Post 016 (size associated with greater organizational innovation). “No, we need to protect our unique firm culture.”

- Well, more of our clients are clamoring for the type of solutions offered by NewLaw and our innovative peer firms. What should we do? Partner 1: “I don’t care because I’m retiring.” Partner 2: “I don’t care because I’m lateraling to a more innovative firm.” Partner 3: “I knew this would happen.”

Perhaps this is what game theory would predict. I think the ranks of the NLJ 350 are going to get thinned out, either through planned mergers, rescue mergers, or run-on-the-bank implosions. But lawyers with their own books of business will never miss a meal.

The UnitedLex-DXC Deal

It is important to remember that UnitedLex is maneuvering on several fronts. In addition to its current point of entry (Figure 3) and ULX Partners (Figure 5), it recently launched a deal with DXC, a large information technology and professionals service firm. See SenGupta, “In-house legal teams take the lead on speed and spending,” FT, Dec. 11, 2017; Orum Hernández, “UnitedLex to Support Bulk of DXC Technology’s In-House Department,” Corp. Counsel, Dec. 5, 2017.

DXC is the product of a merger between Computer Sciences Corporation (CSC) and the Enterprise Services business of Hewlett Packard Enterprise (HPE). The new company has roughly $26 billion in annual revenues, which will eventually place it in the top quarter of the Fortune 500.

In the post-merger company, a portion of the lawyers and staff from CSC and HPE legal departments were re-badged as UnitedLex employees (and others were laid off). According to the press release, UnitedLex now “deploys more than 250 senior attorneys, contract and commercial professionals, engineers, and other experts in support of DXC around the globe.” Interestingly, AdvanceLaw is another part of this deal, handling the selection and management of DXC’s panel of outside law firms. See Sprouls, “Welcome to Legal 2.0,” Modern Counsel, Dec. 13, 2017. UnitedLex projects a 30% cost savings along with greater price certainty. Other anticipated benefits include a bump in quality and transparency.

Figure 6 shows the UnitedLex-DXC configuration, which is yet another Rule 5.4 workaround.

DXC’s general counsel, Bill Deckelman, believes that the sourcing and management system they have put together is “Legal 2.0.”

Last week, I attended a plenary at the ACC Legal Ops meeting that included Deckelman along with the GCs of Walmart, Medtronics, and Chicago Public Media (who had previously worked at Motorola Mobility). After Deckelman explained the new platform with UnitedLex, one of the GCs expressed tremendous skepticism that any cost saving would be worth the risk. Her point was that lawyerly judgment requires business context, and that context is made more attenuated through such aggressive outsourcing. (The other two GCs are building out a mix Figure 2 and Figure 3 models, so they listened with interest.)

What the skeptical GC did not grasp, however, is that DXC is a professional services firm whose core business is the sale and execution of outsourced solutions. DXC has decided to eat its own cooking. Further, although most GC’s are anxious to protect and preserve their headcount — because headcount equates with status and power in most corporate environments — operational legal work is not core to any business with the exception of insurance. The last 20 years have been characterized by an in-sourcing binge of legal work. See Post 003 (graphing growth). The next 20 will be focused on outsourcing to NewLaw or innovative AmLaw200 firms. Either way, UnitedLex wins. See Figure 5 (ULX Partners); Figure 6 (UnitedLex-DXC). The timing, however, may still be an irritant to Dan Reed and many others.

Still a very slow bake

Folks, I am going to make a point grounded in diffusion theory. But this puts everything into full perspective and is arguably the most important point in a very long post. Sorry, it had to come last.

For a moment, consider the Figure 1 baseline model.

Each one of the lawyers in purple and green has a view on how things are going and what needs to be changed. In a corporation, the legal budget (in-house and outside counsel) runs around .3% of revenues with variations by industry. See Henderson & Parker, “Your Firm’s Place in the Legal Market,” American Lawyer, Dec. 2015. Is that too much money? Well, are we talking a relatively simple thin-margin business (e.g., transportation or retail), or a complex business involving IP and extensive regulation (telecom)? A lawyer content with the status quo can spin a story of risk best managed by a big in-house team and/or elite outside counsel. How many CEOs or CFOs can see through the law-is-a-black-art handwaving? Probably not many, though their ranks are growing as they compare notes while socializing.

Granted, agency costs are not the full story. Quite a bit of change is driven by the desires and preferences of innovator/early adopter lawyers (on both the client and law firm sides). It’s just that actual client urgency, and thus law firm urgency, is far from a given. It is also distributed unevenly and somewhat randomly.

Now, consider the UnitedLex configurations (Figures 3, 5, 6) in light of the perceived innovation attributes of the Rogers rate of adoption model in Post 008 (five factors explain 49-87% of rate of adoption). See also Post 011 (slow versus fast innovations).

- Relative Advantage. It really depends on the intensity of pressure placed on legal departments. Exogenous forces can help, as Pangea3 and Axiom were dramatically aided by the 2008 financial crisis. See Post 032 (Pangea3); Post 036 (Axiom). Pressure is steadily increasing — Richard Susskind’s “more-for-less” challenge — but not necessarily on the timetable of VC and PE investors.

- Cultural Compatibility. NewLaw scores low on compatibility, albeit crossover at CLOC and ACC are slowly changing that. UnitedLex and others need to continue the basic blocking and tackling. Theses are the “efforts of change agents,” which is an important rate-of-adoption factor. See Post 008 (reviewing full model, including change agents); Post 020 (going deep on change agents).

- Complexity. Very complex. UnitedLex is not offering a smartphone app. This slows adoption.

- Trialability. Not really. A trial on low stakes work is dismissed as not a real test. The really transformative stuff requires a commitment + effort + time. The client must believe in reason, data, and the experience of other industries. This slows adoption.

- Observability. Really hard to do. I have done site visits and web/conference demos and have been impressed. But that still takes a lot of effort for potential clients. Client testimonials can help here, but are they from opinion leaders? See Post 020 (opinion leaders needed to tip early majority). DXC and LeClairRyan don’t fit that bill, as they are innovator/early adopters. Cf. Post 052 (discussing need of right types of reference clients for pragmatist mainstream market). Higher PPP by itself won’t do it, as the causal relation will be contested.

In summary, ULX Partners (and the UnitedLex-DXC model) appears to be, at best, a slow innovation. See Post 011 (fast versus slow innovations). UnitedLex is competing against in-house legal ops and more innovative law firms, see Figure 2, which are (a) more culturally compatible and (b) require less complex changes in how the work gets done. For some clients, in the short to medium-term at least, these factors may weigh heavier than lower cost and higher quality. Remember these adoption decisions are made by groups of lawyers. All day long, collective adoption decisions impede the diffusion of valuable innovations. See Post 008 (basic model); Post 048 (comparing individual and corporate markets based on type of adoption decision). This is why leadership is so crucial — to serve as a counterweight to paralysis-by-analysis so common among lawyers.

Lawyers might confuse slow change with no change. But they are different. Further, to benefit from slow change, you might need to act very soon in relatively significant ways lest the door of opportunity permanently close. One can’t put off change for a decade and then, when the heat gets unbearable, change overnight.

Appendix on ElevateNext

ElevateNext appears to be a cross between the two UnitedLex models. Basically, most of the legal department functions, including outside counsel management, are being moved to ElevateNext, a law firm that will be very tightly integrated with Elevate Services. The client in this case is Univar, a global chemical company currently ranked #349 in the Fortune 500.

![]() Under this configuration, those practicing law in ElevateNext have best-in-class process, technology, and staffing options. This effort is being engineered by Univar GC Jeff Carr, who is famous in in-house circles for his ACES model and his excellent track record at FMC Technologies, see, e.g., Davis, “Playing with ACES,” ABA Journal, Oct. 7, 2009. In fact, this opportunity got Jeff to un-retire. Thus, ElevateNext will be highly incentivized to optimize their use of Elevate legal ops functions. Also, when Univar needs the specialized expertise of a law firm, the firm will enter into an ACR with Univar, but ElevateNext lawyers (i.e., another law firm) will, in most cases, manage them. (By the way, the DNA here descends from Mark Cohen and Clearspire.)

Under this configuration, those practicing law in ElevateNext have best-in-class process, technology, and staffing options. This effort is being engineered by Univar GC Jeff Carr, who is famous in in-house circles for his ACES model and his excellent track record at FMC Technologies, see, e.g., Davis, “Playing with ACES,” ABA Journal, Oct. 7, 2009. In fact, this opportunity got Jeff to un-retire. Thus, ElevateNext will be highly incentivized to optimize their use of Elevate legal ops functions. Also, when Univar needs the specialized expertise of a law firm, the firm will enter into an ACR with Univar, but ElevateNext lawyers (i.e., another law firm) will, in most cases, manage them. (By the way, the DNA here descends from Mark Cohen and Clearspire.)

Below is the ElevateNext configuration.

The analysis on the UnitedLex models applies wholesale to ElevateNext. Jeff Carr is a thought leader, but he is not an opinion leader that triggers the early majority to follow. Instead, they watch with interest, as happened with the ACC Value Challenge. All of this will take longer than reason or self-interest would suggest.

What’s next? See BigLaw partners aren’t dumb: they are just not in the room (054)