The 4th Industrial Revolution is here (even for lawyers). A look at what digital transformation actually means for legal markets — and the investments tomorrow’s winners are making today.

Today’s post is the final part in the 5-part series #GreatExpectations for the #GreatReset. (Like the vaccine rollout 💉 and my workout plan 😁, this post is a bit delayed 🥺. A million thanks to Bill and the Legal Evolution audience for the patience!)

Part I (216) gave a retrospective on the last downturn and some big-picture data to explain the changing context around the legal industry. Part II (217) and III (218) were experimental in format, relying on 10-12 charts to explore a central theme. Part II explored the impacts and implications of a K-shaped recovery for legal markets. Part III focused on YOY volatility for incumbent players amid stagnating market conditions. Part IV (219) applied some of these trends to interpret key dynamics in the enterprise law market, with emphasis on why I’m bullish for ALSP hockey stick growth in 2021.

Today we zoom back out market-wide and shift our focus to tech. What will the #GreatReset look like for the fast-growing legal technology market? What are the implications for lawyers and legal teams, not only as consumers of technology but also as makers, buyers and stewards of technology? To explore these questions, we also look at how technology is already and will likely change the experience of the end-user of legal services (bc #clientcentricity, always).

LegalTech: Current State of Play (TL;DR: It’s 🔥 but unevenly distributed)

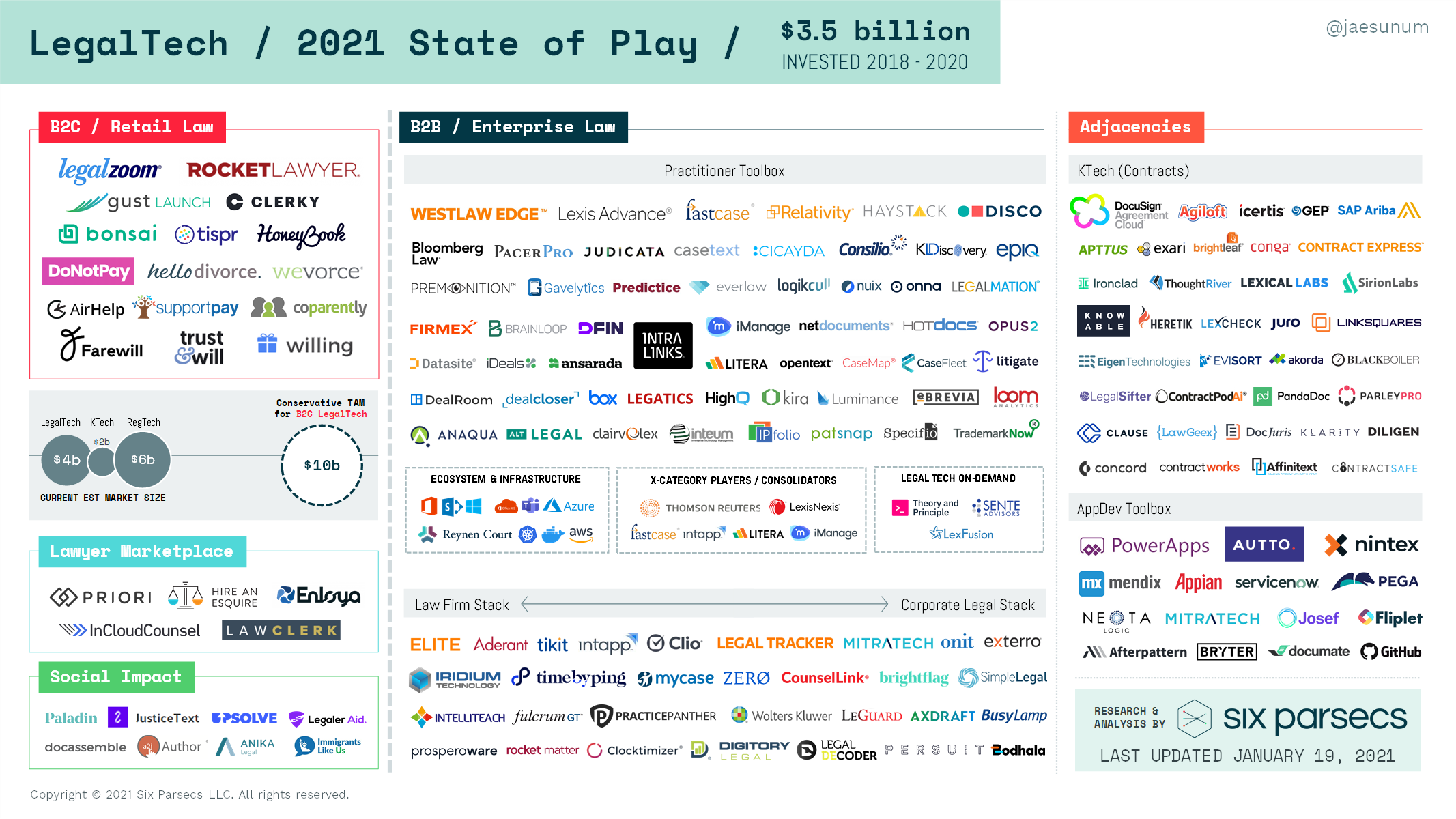

Let’s start with a high-level look at the legal tech market landscape today. The below graphic is intended to provide a directional & representative sense of who is playing where in the legal tech market with highlights on some key trends of particular interest.

Before we dig in, two disclaimers & some recommended resources. This is far from comprehensive (and market maps rarely are, although this MarTech supergraphic is an exception.

- To those who want to dive deep and wide to experience the full extent of the Cambrian explosion happening right now in legal tech, two new-ish links worth bookmarking: (a) Orrick Observatory and (b) Legal Tech Hub. Both are ambitious projects to catalog and organize the exploding number of legal tech tools available in the market today, and both are backed by the experience and insights of teams deep in the #RealLife trenches of legal tech. Orrick has been a consistent leader among BigLaw peers in innovation investments, while Legal Tech Hub is the passion project of Nicola Shaver, Managing Director of Innovation and KM at Paul Hastings.

- While I’ve attempted to highlight some of the legal tech activity happening in the social impact space, others far more experienced and knowledgeable than me will provide more meaningful guidance. Watch for an imminent overview of #JusticeTech from Felicity Conrad of Paladin, a platform dedicated to expanding access to justice through tech that supports pro bono programs.

Lots of white space for legal tech in B2C markets 👀

First point of note in exploring the market map: the distinction across B2C Retail Law and B2B Enterprise Law.

The retail law market will map roughly to the “PeopleLaw” sector as discussed in Post 037 as well as the Heinz-Laumann two-hemisphere model as explained further in Post 051 (key graphic reproduced below). See also Bill Henderson, What is more important for lawyers: where you go to law school or what you learned? (Part II), Legal Whiteboard (July 19, 2015).

LegalZoom and RocketLawyer still dominate the B2C legal tech category as they have for many years, but a few interesting patterns emerge in my scan:

- Specialization in the retail legal tech market: GustLaunch and Clerky are both geared to helping entrepreneurs navigate the process of starting a company. Two distinct subcategories in the retail market are geared toward major life events in the human experience with significant legal and financial implications: divorce and death.

- Legal is part of the show but not the star: Bonsai, Tispr and HoneyBook are broader solutions aimed at freelancers. All three products offer a broad range of value and benefit across back-office bookkeeping and project management functions as well as front-office commercial activity. That last piece includes contracting with customers, and for that reason they are included here. (Keep this configuration in mind; this theme will emerge again with BIG implications in the enterprise market.)

- DoNotPay aims to put a lawyer in every pocket: One of the bright spots in an otherwise dreary year for legal tech funding, DoNotPay raised a $12 million Series A last summer (a quick follow to the $4.6 million seed round in 2019). See Paul Sawers, “DoNotPay’s legal bots help consumers fight the system during lockdown,” VentureBeat.com, Jun 23, 2020. The round puts DoNotPay at an impressive $80 million valuation with a sparkly roster of Valley investors. I signed up (and paid) for DoNotPay. While I think the team has some hurdles still to clear, the concept is on point. DoNotPay is seeking to roll up the universe of small friction points and consumer aggrievances that accumulate in life. While each grievance doesn’t merit lawyering up, DoNotPay is betting that bundling all those little annoyances into a low annual fee (currently $36 per year) will convince millions of individuals to pay them instead (presumably with all the money they #DidNotPay). The hurdles DoNotPay must clear are (a) lowering the total effort required for consumers to complain (they nailed this); (b) iterating through customer pain points (and they are, very fast); and (c) aligning the build-out and scaling #InRealLife fixes behind the digital UX (I suspect this will be harder and more expensive bit). The sheer market size explains the Silicon Valley interest and the valuation. (Again, there are a few themes here that will resurface soon).

Apart from the above, my main takeaways are that the retail law market offers an enormous amount of white space for legal tech, and I think this market subsegment is (finally) ripe for a Cambrian explosion of its own. Why now and not before? Two reasons:

- Perpetually underserved customers in a highly fragmented and difficult-to-navigate market: Even for professionally trained and qualified lawyers, legal services are difficult to buy. Most purchases in life are “search” or “experience” goods, in that, a potential buyer can usually obtain and evaluate information on available options before (search) or after (experience) buying and using the product or service on offer. Legal services remain an example of a relatively rare third category: the “credence” good. Credence goods are difficult or even impossible to evaluate even after purchase and consumption, usually because the customer lacks the domain knowledge or expertise to make a meaningful judgment, or because reliable information on available options is prohibitively difficult to explain. This pretty much sums up the frustration of all buyers of legal services everywhere ever, but it hints at a massive opportunity for would-be disruptors.

- Trained user base with built-in point-of-sale: In 2020, 2.9 billion people worldwide used smartphones; the average user will interact with their phone over 2,600 times a day. Millennials spend about 5.7 hours per day on their phones and Boomers aren’t too far behind at 5.0 hours per day. Quick flashback. Apple released the first-generation iPhone in 2007 and sold 6.1 million units; in 2020, iPhone sales tipped 195 million units. See Jefferson Graham, “Apple iPhone again best tech seller of the year, thanks to the working-from-home trend,” USA Today, Dec 28, 2020.

The PeopleLaw sector in the U.S. hovers around $60 billion spent per year in a perpetually dissatisfied and underserved market, and that figure of course does not capture all of the currently unserved legal needs (like those identified by DoNotPay). See Post 037. Extrapolating some of the U.S. figures for a global estimate, an 10% to 12% displacement of current consumer spend on legal services by digital alternatives would give us a total addressable market between $9 and $11 billion. On that basis, I expect the Silicon Valley money to be looking for smart investments in this space.

Can’t stop, won’t stop 🎶 (2020 was just a speed bump for enterprise legal tech)

Both legal tech spending by law firms and capital investments into legal tech startups slowed down in 2020. Amid the across-the-board slashing of expenses by law firms, only two categories remain on an upward trend: technology and knowledge management, both hovering around a 2% increase year-on-year from 2019. (As a benchmark, technology spending increased almost 6% from 2018 to 2019 and almost 4% from 2017 to 2018). See Thomson Reuters / Georgetown Reports on State of the Legal Market. While both deal count and deal value dipped in 2020, many of the long-term trends we’ve seen in legal tech markets held up, particularly the increasing size of fundraising rounds. See Post 218 (key graphic reproduced below); see also Post 109 (providing overview of legal tech funding trends over the past decade).

We’ll dig into a couple of these deals in more detail, but first let’s take another peek at the market map, turning our attention to the enterprise market. (I promise we will talk about that monster Series D for Ironclad.)

🗺️ A few user notes on how the market map is organized, because they hint at some broader trends we’ll discuss in more detail in just a bit.

🧰 PRACTITIONER TOOLBOX getting more crowded (but cross-category consolidation should rationalize this a bit): Rather than hard-and-fast buckets, I’ve organized this section into rough regions, as follows. Research anchors the top left and eDiscovery the top right. Just beneath, DealTech anchors the left side, litigation tech the right. In the center of the map I’ve grouped tech that targets document drafting, management & analytics. Intellectual Property runs across the bottom lane. Not only longtime cross-category players like TR and Lexis but also a new wave of consolidators are playing across traditional categories.

🤝 Enterprise CONTRACTING requires an ensemble cast: Lawyers play an important role but they’re not the star, and a new wave of players in KTech are building with this in mind. For that reason I’ve carved out contract-related solutions to an adjacency.

🛠️ Built for lawyers by lawyers with a growing APPDEV TOOLBOX: A number of macro trends converge to make it easier for business and legal teams to build lightweight apps. For that reason, I’ve highlighted AppDev Toolbox as a second adjacency.

🥊 Goliaths dominate BUSINESS-OF-LAW STACKS (but a few new entrants mount a challenge). Legacy market leaders like TR, Aderant and LexisNexis have dominated both law firm and corporate legal back- and middle-office stacks, but watch for some reshuffling in the next 3 to 5 years: both Intapp and Iridium are rolling up acquisitions across the law firm back office; Silicon Valley-funded Ping takes a run at the age-old problem of making time entry less awful, and expect an ongoing melee in matter management and pricing.

🚧 ECOSYSTEM & INFRASTRUCTURE matter (because tech doesn’t get sold, deployed, and used in a vacuum): For a number of reasons, cloud readiness is likely top-of-mind and top-of-agenda for every CIO in 2021 — and if it isn’t, it should be. (Keep reading 👇👇👇 for the proof.)

🎥 A few quick hits from the 2020 highlight reel:

- hG-backed Litera continues buying spree for an unrivalled 18-month run. Since acquiring Best Authority, Workshare and Doxly in 2019, Litera’s 2020 buys add bolt-ons from a diversity of categories, including contract drafting (Bestpractix) and litigation management (Allegory Law). See Bob Ambrogi, “Litera Acquires Litigation Management Platform Allegory Law from Integreon,” Lawsites, Aug 21, 2020.

- Fastcase also continues an extended run of consolidation. In 2020, Fastcase brought Judicata into the fold, likely toward a better-knit practitioner experience across research and drafting. See Ambrogi, “Fastcase Acquires Technology and Staff of Innovative Legal Research Platform Judicata,” Lawsites, Aug 21, 2020.

- iManage joins the #DealTech wave by picking up Closing Folders in 2020. Back in 2018, NetDocuments’ acquisition of Closing Room made waves by buying tech baked inside a law firm (Chapman and Cutler). I suspect this may portend a category-wide move by the document-centric players to reach for practice-specific extensions across both transactions and disputes. See Press Release, “iManage Acquires Closing Folders, Leader in Legal Transaction Management; Combination Yields Best-in-Class Integrated Document and Transaction Management,” August 24, 2020.

🌪️ And 2021 off to a whirlwind start, with big news from both Litera and Fastcase (🤔 notice a pattern here?); the official announcement of Ironclad’s Series D; Relativity’s acquisition of VerQu; and a $14 million raise from Lupl (featuring a global cast of law firm backers).

That concludes our quick scan of the current state of play. Against that backdrop, what might 2021 hold in store for legal tech?

KTech is the new hotness 🔥 (and understanding WHY would help everyone)

At least until the singularity arrives, tech exists to serve humans, and a tech business must understand not only WHAT it makes and HOW it will work, but also WHY human beings need it.

This is customer-centricity in a nutshell: to see past what the startup wants ( 🦄 valuation because a billion dollars is cool) and needs (🏒 hockey stick growth and ALL THE ARR) to what paying customers want and need (but don’t have yet). This is much harder than it sounds, and a successful exercise in commercial empathy doesn’t end with post-its about feelings. The search for product-market fit may begin on a whiteboard but at some point, cold hard math must enter the arena: market size, adoption and growth rates, and a price point that market will bear.

🏆 Size the prize (because market is EVERYTHING)

In a 2007 post, Marc Andreesen posited a theory that market size trumps everything, including product quality and team caliber: “[t]he #1 company-killer is lack of market.” (The post is part 4 of his 9-part Guide to Startups and is well worth the time to read for anyone interested in legal tech.) My favorite line in this post:

In a great market — a market with lots of real potential customers — the market pulls the product out of the startup.

The contracts space is a good illustration of how Andreesen’s point plays out in the real world (and quite close to home for the legal industry):

Contracting is not a new challenge for corporates. Like any endeavor in life requiring two or more parties to reach an agreement, human factors add layers of nuance and complexity. However, commercial leaders have long understood the size of the prize at stake. Companies that are more adept at managing the contract lifecycle make (a LOT) more money. Here’s a rough back-of-napkin illustration of problem size. In 2020, the Fortune 500 collectively posted $14.2 trillion in revenue. Conservatively estimating “high performing contractors” as the companies taking 10% of revenue share ($1.4 trillion), the would-be buyers of better and faster contracting capabilities stand to gain revenue lift in excess of $120 billion.

That should shed a bit of light on the tsunami of capital and frothy valuations we are likely to see for KTech players. I believe the KTech market will pull the product out of startups — and the visible signals from the past three years suggest, at least to me, that the time is now.

⏲️ The importance of timing (because being too early is the same as being wrong)

Until fairly recently, the contract space was preoccupied by the mechanics of shuffling paper from one part of the organization to the next. Digitizing the contracting process required enterprises to incur material change management costs, often faltered in creating frictionless user experiences, and offered little gain in terms of “better, faster” contracting.

Fast forward to 2021 and KTech is making leapfrog advances to focus on the substance of the commercial transactions that comprise the flow of capitalism. This is made apparent by the proliferation and diversification of next-gen tools now available across full contracting lifecycle: drafting, negotiation, and obligation management. From a technical standpoint, the tooling is much more sophisticated and way more (if not quite) ready for prime time across extraction and abstraction for analysis — bringing to bear years of maturation in component technologies like NLP (natural language processing) and TAR (technology-assisted review) in eDiscovery. 🦄 If Ironclad is the BTS of KTech, then Kira would probably be Gangnam Style for taking AI-enabled contract review mainstream. 🦄

Apart from technical advances, environmental factors likely jumpstarted the entire category and pulled current-gen KTech out of startups. Brexit and then massive regulatory reform in financial services collided to create a contract remediation challenge massive in scale and global in scope. (Basically, it’s like Y2K but for lawyers).

- In 2018, Axiom launched BrexitBridge, noting that Brexit readiness would require changes to 7.5 million contracts within the following 12 months. See Press Release, “Axiom Launches BrexitBridge to Handle the More Than 7.5 Million Financial Services Contracts That Require Updates for Brexit,” March 15, 2018.

- More than a decade after the subprime crisis tanked global markets, LIBOR (London Interbank Offered Rate) will finally sunset in coming months. PwC estimated that LIBOR is the benchmark for over $350 trillion across 100 million financial contracts worldwide, with Factor estimating that 40% of these include no provision regarding the cessation of the benchmark. See Press Release, “New Analysis Estimates Up to 100 Million Contracts Require Assessment, Remediation as LIBOR Benchmark Rates are Discontinued,” March 20, 2020.

These contracting crises proved a boon to emerging KTech stars by creating optimal conditions for adoption and growth. The immense time pressure and scale complexity of these contracting challenges forced clients to develop an openness to new ways of working. That gave emerging frontier tech plenty of runs in the wild to test and improve any wrinkles but also to build success stories.

Beyond the KTech market, these contracting crises arising from geopolitical shifts and an increasingly regulatory landscaped also pulled digital transformation out of financial services firms. If necessity is the mother 🐔 of invention 🐣 , pressure might be the mother of adoption. After a decade of consultants and analysts prematurely predicting the imminent digital transformation of large-scale enterprises (and as many years of eyerolling and facepalming about the change resistance of lawyers), Brexit and IBOR remediation are now underway, enabled by an unbelievably speedy adoption of digital technologies both old and new. In the process, some of the most laggard business functions inside corporations (across compliance, risk, accounting and legal) have made the leap into the digital economy. This means they can now show (not tell) the positive externalities of digitalizing a business-critical process: an exhaust of structured data ripe for analytics & insights.

Technical feasibility and timing conspired to make KTech a “great market” by 2017, and I think that momentum will continue for the next 3- to 5-year run. (When it comes to market… timing is also everything. Videoconferencing, workflow software and micropayments are the 3 examples Andreessen gave as terrible markets in 2007.)

🌊 The next wave of KTech growth

Expect to see continued acceleration of activity levels for KTech players in 2021, but that activity will likely traverse the bounds of ‘legal tech’ as we know it.

- DocuSign has made big acquisitions in this direction beginning with SpringCM in 2018 and Seal in 2020, now wrapped and packaged into DocuSign Agreement Cloud, a growing suite of applications with more than 350 integrations to cover nearly every enterprise stack configuration under the sun, mounting a challenge to the “API-first” ethos that has kept Icertis at the forefront with 200+ APIs out of the box. See Blog Post, “Announcing the DocuSign Agreement Cloud: 2020 Release 3,” November 12, 2020.

- Agiloft (a Gartner CLM Magic Quadrant leader for multiple years) made waves by nabbing Andy Wishart, founder of ContractXpress and longtime product lead for TR’s drafting and productivity solutions, as its new Chief Product Officer. This high-profile hire suggests Agiloft will double down on the contract creation phase of the lifecycle, which could have immense multiplier effects on downstream needs across review, search, analysis, risk scoring and obligation management. See Ambrogi, “Legaltech Moves: Wishart to Agiloft; Levine to ContractPodAi,” LawSites, January 13, 2021.

Ironclad’s recent raise should fund a good run at the established leaders and its stated mission of creating a new “digital standard for digital contracting” (a righteously ambitious vision). While lawyer-led Kira and Luminance have a head start in intelligent review, I suspect serving both law firms and corporates will prove to be a challenge when so many KTech players remain laser-focused. DocuSign’s dominant market share in e-signatures makes for a built-in channel to the largest corporate accounts worldwide, while Icertis has a proven track record in large scale enterprise deployments and Agiloft has racked up very high customer feedback scores across the board. Knowable, the Axiom spin-off, likely has an insider foothold in financial services.

In the next 24 months I suspect we will see continued capital flow in KTech and likely a wave of consolidation via acquisition. The point solutions focused on contract drafting, negotiation and large-scale review are strong candidates to hit escape velocity out of legal tech given that those phases require heaviest touches from lawyers.

👀 LegalTech markets are smaller (and harder to find)

In my very first post on Legal Evolution, I characterized legal markets as balkanized and opaque (👩🎤 to the extreme 🤘). This is at least in part why innovations take so long to take hold in this market and why the sales cycle for legal tech is so long and hard. See Post 063 (detailed discussion of Miller-Heiman Strategic Selling framework applied to legal vertical).

This puts the burden on legal innovators of all stripes to actively define niche markets and subsegments (key graphic from Post 051 reproduced below):

A customer-oriented, need-based view reveals that the broader market for legal services actually functions as a fluid and complex network of mini-markets, loosely held together by the fact that the sellers and providers have historically been licensed lawyers. See Posts 217 and 218 (discussing varying pricing pressures and likely divergent demand trends across practice-industry matrix); see also Post 219 (describing erosion of the near-monopoly of the law firm model in enterprise markets).

Most legal tech companies selling primarily to lawyers and law firms are targeting tiny slices of those mini-markets. If KTech comprises a huge market, most legal tech market sizes (especially those coalescing around the Practitioner Toolbox) probably fall closer to micro-markets.

That may sound discouraging, but there’s no need for despair. It is very possible to make money in micro-markets — but relentless and obsessive focus on the customer is a must (and proper market and problem sizing are even more critically important). For a reality-based peek into the crystal ball for #LegalTech, we first need to understand the viewpoint of the people and organizations that comprise potential micro-markets.

🌏 A brave new world: the 4th Industrial Revolution is here (and why it matters for legal markets)

The 4th Industrial Revolution encompasses several megatrends, but they all coalesce around the digitalization of commerce, work and life. I’ll skip all the eminently hashtag-able buzzwords (#AI, #IoT, #RobotEverything) and cut to the chase.

The World Economic Forum put it best:

In its scale, scope, and complexity, the transformation will be unlike anything humankind has experienced before… The speed of current breakthroughs has no historical precedent.

There are two reasons to for everyone to care, right now. Firstly, we are all competing in a new economy whether we realize it or not, one based on data as its primary resource (making insights the new currency). Secondly, the digitalization of life is rewiring our world to move exponentially faster, making the extent of change more drastic and leaving laggards so far behind that catching up later may not be an option.

🦾 The future belongs to bionic teams (not sentient AI)

Simply put, teams and organizations that harness tech and data to supercharge human efforts will win the future. In concrete terms, legal businesses leading in these four interdependent areas will gain a competitive edge: fluid access to frontier practice tech; superior data handling capabilities to enable faster access to better insights; a head start toward cloud readiness; and the organizational capabilities required to empower the rise of citizen developers and analysts.

Next-gen tooling is here….

but our total cost-to-consume (beyond direct hard costs of the tech) remains high and time-to-value is far too long.

As the legal tech market map above makes clear, legal teams now have more available options than ever before to ingest technology into their ways of working. And yet, fluid procurement and adoption remain elusive. On balance, the expanding practitioner toolbox is a plus for the industry, but comes at a cost: more marketplace crowding makes it more difficult for resource-constrained teams to discover, vet and assess options. Across the industry, law firms and law departments remain scattered across a wide spectrum for legal tech maturity, adding yet another substrate to the balkanization of legal markets.

The implications for the industry are bad. Too many finance and legal operations stacks reinforce outdated models of legal buy and impede meaningful progress toward AFA adoption at scale, while tech procurement hurdles separate practitioner teams from frontier tech built on next-gen AI. Despite widespread experimentation with a growing suite of tools, market penetration is moving slower than we’d like, with very few legal teams deploying best-in-breed practice tech at scale.

We are all data hoarders…

A critical feature of the 4th Industrial Revolution is exponential growth, and the ongoing explosion of data in the world provides the most concretely observable illustration. Here are some 🤯 statistics to make this more real. Every 60 seconds, 200 million emails are sent, nearly 5 million YouTube videos get watched, and over 4 million searches are typed into Google. All of that digital activity adds up and the resulting data exhaust accumulates over time, leading to the total volume of data in the world doubling every two years. With over two thirds of the world’s population now online, this exponential growth in data volume and variety will continue —and that may leave the legal industry in a ⚠️ danger zone ⚠️.

If data is really the new oil, why wouldn’t we want more of it? Firstly, data volume is multiplying much faster than we can manage (like tribbles); secondly, not all data is useful or usable; and thirdly, the turning data into valuable insights often requires work from specialist teams and therefore costs the organization time and money.

A recent tweet from Sarah Glassmeyer explains it differently:

I had not heard that @SusanWojcicki called YouTube a library.

Dear technologists: libraries are curated and moderated collections of tools and information. Stop calling your hoarded piles of digital crap a library in order to use the earned reputation of 1000 yr old institution

— Sarah Glassmeyer (@sglassmeyer) January 18, 2021

Gartner estimates that poor data quality costs the US economy up to $3.1 trillion yearly, with 95% of businesses reporting that they need to improve how manage unstructured data. See Mike Davie, “Why Bad Data Could Cost Entrepreneurs Millions,” entrepreneur.com, April 15, 2019. After a decade of mounting “more with less” pressures, most law firms or law departments lack a clear roadmap forward to improve data quality and usability.

The cloud imperative

For all practical intents and purposes, Microsoft, Amazon, and Google have already decided that our collective future will be a cloudy one — and most of the Fortune 1000 IT community appears to agree that cloud migration is an inevitability. The collective innovation and R&D firepower of these three companies amount to billions, and those investments are tipped so far in favor of the cloud that on-prem infrastructure will be hard pressed to compete. A 2020 Report on State of the Cloud found that 93% of enterprises have multiple clouds and 87% have a hybrid cloud strategy; Forrester predicts that by the end of 2021, 60% of companies will leverage containers on public clouds. See N. F. Mendoza, “Top cloud trends for 2021: Forrester predicts spike in cloud-native tech, public cloud, and more” TechRepublic, October 20, 2020.

The why, when, and how of cloud migration have been exhaustively and hotly debated by technical experts everywhere. For me, the scalability required to turn our “hoarded piles of digital crap” into “useful tools and information” is the most compelling reason for businesses to opt for a cloud-first strategy (because turning data into useful insights is what I primarily do). However, the second-order impacts on overall market efficiency for legal tech are worth noting.

Due to real governance and security concerns imposing unique barriers for legal organizations, CIOs across BigLaw will likely need to manage the when and how of their own journey to the cloud over the coming months and years. As legal businesses remain scattered at various points in that journey, infrastructure variations will add yet another layer of complexity and source of drag for legal tech vendors searching for product-market fit. During this transition period, the firms that can generate better insights faster will make better decisions, and practitioners with more fluid access to best-in-breed toolboxes will outperform the competition. Conversely, the legal tech companies able to deploy quickly and seamlessly across a variety of infrastructure roadmaps are far more likely to find their market first.

Ultimately, the digital economy will require every organization to rethink IT infrastructure from the ground up and to balance security and fluidity in how data and information flow across organizational boundaries. The current levels of fragmentation highlight the importance of more efficient market-making in legal tech procurement, and a more rationalized ecosystem and market landscape will require a greater degree of standardization and modularity.

Rise of the citizen developer and citizen analyst

Tech-first approaches targeting the high end (or even the mid-range core) of enterprise legal markets tend to fizzle, as Clearspire and Atrium did. “Disruptive innovation” is literally defined by the originator (RIP Clayton Christensen 😢) as starting in the low end of the market then moving upmarket to take share from incumbents. Cf. Clayton Christensen, Michael Raynor, and Rory McDonald, “What Is Disruptive Innovation?“, Harv Bus Rev (Dec. 2015). #RobotLawyer plays are far more likely to find early success in niche applications, either in the retail law market or in the more commoditized subsegments of enterprise law. Rather, winning service providers in most legal markets will likely be players with the process and tech muscles to drive incremental innovation in their core business.

The mission-critical mandate for most service providers in the enterprise market will be talent-led, to empower rather than displace expert practitioners. Apart from the legal tech maturity required to select and access the best-in-breed tech solutions available on the market, I expect we will see more firms invest in both talent and tech geared to workflow automation, knowledge management, and data handling — with the express goal of helping practitioners discharge their work and generate better insights faster. In that regard, the proliferation of low-code / no-code platforms as well as continuing expansion of open source resources are two trends that lower the cost of entry for incumbent law firms to build lightweight, fit-for-purpose business applications.

Democratizing the agile development of tech and more efficient production and consumption of data-driven insights will be an obvious source of competitive advantage — but as Casey Flaherty likes to say, “obvious ≠ simple and simple ≠ easy.” While we see more analytics and AppDev teams embedded in more law firms, they often work as firefighters or lone gunslingers, falling short of organizational enablement at scale. A critical barrier that legal businesses face will be to attract and retain the talent with the skills or potential to grow into effective citizen developers and analysts.

🤔 How to stop worrying and love the bomb

Digital transformation is an imperative for every organization, but the path from here to there is likely to include (a lot of) discomfort. Digitalization and automation remain inextricably linked, and for good reason. Much of the work humans do now will be unbundled and automated in pieces. That said, it bears repeating that automation is necessary because the aggregate volume of work that needs to be done is growing — in many cases exponentially. See Posts 216 and 218 (discussing multiple trends likely driving invisible increase in demand for legal services and declining willingness to pay prevailing rates).

In vast swaths of today’s legal market landscape, automation & displacement anxiety are likely overblown and misplaced. Three concrete illustrations support the general view that lawyers and technology must not be enemies but friends:

#WhiteShoe 💖 #DealTech

Most prestige firms will likely be fast followers (if not leaders) in adoption of best-in-breed #DealTech. Competing for top-of-market work at top-of-market prices will simply require it, because the next-gen DealTech will make deal teams materially better (in their insights and advice) and faster (not in the sense of billing fewer hours to do the same work but rather in pace of execution to get to the right answer faster). If one of the old-line Wall Street or City firms should decline and fall, lagging in this aspect will likely be a contributing factor. However, don’t expect a barrage of press releases on their tech roadmaps or category-wide decline in their pricing; neither will be necessary.

(As a contrast, I don’t believe the same will apply to disputes, where I suspect adoption of breakthrough innovations will continue to thrive closer to the lower end of the market. The difference is that companies engage in (most) deals by choice, whereas much of the litigation volume in the enterprise market is defensive in nature and already under immense price pressure. The dwindling share of high-consequence, bet-the-company litigation remains less conducive to prediction and planning relative to deal work — and will likely stay expensive regardless of how outside counsel discharge the work simply because the business value at stake merits the price tag. That said, litigation teams with superior proficiency in leading-edge TAR will also find quicker paths to victory; on that basis I think litigation tech will flourish as well.)

KTech & RegTech bonanza 🎊

Leading law departments will build new infrastructure to enable step change in how the enterprise (a) handles day-to-day transacting and (b) operationalizes compliance at scale. The pace of commerce and increasing complexity/volatility in the regulatory landscape will demand it. This translates to massive opportunity for KTech and RegTech, but (as is the case with spend reduction and budget control) this transformation remains the domain and accountability of the corporate legal function, not their outside suppliers. Corporations that focus exclusively on short-term legal spend reduction at the expense of this long-term investment do so at their peril. Those who simultaneously slash rates while relying on outside counsel to subsidize innovation via “value-adds” (e.g. more free labor on top of discounted rates) will fall behind, to the mounting detriment of the enterprise.

The digital front door 🚪 must evolve into digital pipelines (at scale)

Over the past decade, firms have invested immense amounts of time and money into client portals in an attempt to digitalize the client experience. SharePoint-based extranets have helped to advance financial reporting and team collaboration (and decorated many careers with ILTA awards in the process). Meanwhile, clients have made their own investments into operational stacks, and en masse implementation of e-billing systems have now dominated legal ops agendas for several years running.

In a classic scenario common to wicked problems, the best efforts of individual players have somehow made the collective problem worse. In any given year, most of the AmLaw 100 will need to service between 5,000 and 20,000 active clients. Despite an extended effort by corporate counsel to rationalize legal supply chains, many large-cap corporates still maintain provider networks that number in the hundreds (in part because jurisdictions add yet another substrate of fragmentation to legal markets but also because conflicts pose a hard barrier to the otherwise extreme forces for consolidation). As things stand, point-to-point interfaces for every client-firm pairing are already unworkable, and the ecosystem is likely to experience increasing rather than decreasing strain in future.

Modern enterprise-to-enterprise relationships require collaborative investment in interoperability, and market efficiency depends on industry-wide standards that reduce switching costs. Instead, law firms have grafted a digital front door to an otherwise frustrating client experience while clients have invested in back-office infrastructure that does not easily lend itself to scalable interoperability across the supply chain. As a result, delayed and inaccurate bills remain a perennial wellspring of client complaints. Many clients have weaponized e-billing systems that simultaneously whittle down law firm cash receipts while adding to law firm back-office costs. The collateral cost to the industry has been a steady erosion of trust in complex institutional relationships. As this problem demonstrates, digital transformation is not about bolting more technology onto broken systems; instead, we need to revisit and rethink some of our long-held assumptions about (a) why things don’t work as we want and need them to and (b) how technology can fix the problem at the source.

Innovation is as innovation does 🃏

In some ways, technology is both the driving force and the great red herring of our time. Organizational transformation of any flavor is a human endeavor. No matter the external pressures or intrinsic rewards, meaningful change doesn’t just happen — persistent people and committed teams make them happen.

As critical as innovation will be in the digital economy, it is not a panacea nor a guarantee of survival. Meaningful experimentation always carries a degree of risk. For a few incumbents who are poorly positioned in practice mix and client base or lacking the cultural foundation and commitment to hear the voice of the client, no amount of legal tech can stem the bleed. Meanwhile, some who are really trying to adapt will ultimately fall victim to the Darwinian dynamics of competition despite significant investment in innovation, either due to bad decision-making or failures in execution.

Building and investing for the future is an imperative for all. Most in legal markets face significant headwinds in coming months and years, and a few will decline and fall. Still, my general outlook is one of hope and positivity. Even in an environment of increasing risk, one thing is for certain: we all have the ability to influence our own outcomes. Those who adapt will be the ones that thrive.