Before we peer into the 🔮 crystal ball to forecast what awaits legal markets in a post-pandemic future, we first look back to the past for lessons from the last downturn – with a wider lens to better understand how the world around our industry is changing.

Now is the winter of our discontent: the worst (😧!) year (🤮!) EVER (😣!!) is finally in the rearview mirror. Although the first stretch of the new year presages some grim days ahead, I’m doing my best to look to 2021 and beyond with hope and optimism.

Both hope and optimism may be in short supply at present, not only among our audience but across the entire world. Last Wednesday’s attack on the U.S. Capitol is both horrifying and heartbreaking but not surprising. Around the globe, economic inequality is on the rise. In tandem, the past decade has seen a cresting wave of nationalist sentiment and troubling spikes of extremism and violence. The ravages of the pandemic have simply revealed the fragility of the current socioeconomic order.

Today’s post (216) is Part 1 in a 5-part series on the post-pandemic legal market landscape, which will run through MLK Day. As against the backdrop of economic turmoil, geopolitical instability, and ongoing threat to human life, the fate of legal markets may fade into relative insignificance in our hearts and minds – but this is a mistake.

What we see happening in the world around us provides critical context for the work we do in this industry. More importantly, what we do – as individuals and as participants in businesses and in markets – matters. For my part, the best contribution I can offer is clarity.

A. Roadmap to Recovery for ⚖️ and 🌏: We Begin with Shared Truths

As in the wider world, we in the legal industry spend a lot of time and energy talking past each other and shouting at the rain, because we have lost our footing on the firm foundation of shared truths. The overarching goal of this series is to provide a more credible narrative of how and why legal buy has changed in the past decade — one with greater continuity, coherence, and fidelity than the snapshots and hot takes that are usually afforded by the frenetic pace of the 24-hour news cycle.

- Part I (216) is a historical retrospective on the Great Recession. My intent is to shed light on the growing tensions across buyers and sellers in the enterprise legal market and to reframe how we think about our priorities going forward.

- Parts II through IV (217, 218, and 219) address the factors that will separate the winners from the losers in a post-pandemic reality. In these posts, we take a deeper dive into data on critical differentiators across segments: service providers (e.g. corporate buyers, incumbent law firms, insurgent new entrants) and enablers/encroachers (e.g. legal tech & content).

- Part V (220) covers key trends to watch for the next 5-year period, with emphasis on how legal innovation of all flavors are likely to transform both enterprise and PeopleLaw segments.

Throughout the series, these posts will venture into the realm of projection – always a risky endeavor. However, my goal is not to make lucky guesses about what the future holds. Instead, the objective is to provide useful observations that will draw attention and focus to issues that must and can be addressed. As always, the hope is to offer constructive analysis that will inform more meaningful dialogue and more intentional action.

B.  Revisionist History: Mythbusting the 2008 Crisis & Aftereffects on AmLaw 200

Revisionist History: Mythbusting the 2008 Crisis & Aftereffects on AmLaw 200

The COVID-19 pandemic kicked off a long-expected downturn in the most unexpected manner, and current levels of uncertainty cast legitimate doubt on whether any past lessons might apply to our current timeline. A close look at historical data 📉 convinces me that we can find a few, but first we need a bit of skepticism to sift through a few misleading narratives that have long since entered our collective consciousness as canon.

(i) Growth is a Siren Song (and BigLaw Prosperity May Be #BIGLY #FakeNews) 😮

Eight years ago, Bruce MacEwen published a book titled “Growth is Dead: Now What?” Apparently, most of the market didn’t get the memo.

In most years, the AmLaw 200 collectively post a “record year” for revenue growth, and “down years” have become the stuff of nightmares for managing partners and CFOs across BigLaw. While few would admit managing to the ALM metrics, nobody likes to take a tumble in any power rankings. And while PPEP has little bearing on the cash money distributions that hit the bank accounts of each individual partner, PPEP remains a handy metric to compare the waxing and waning fortunes of every other firm, stoking the competitive fire in the hearts and minds of millionaire lawyers looking to keep up with the Joneses.

Thus, “AmLaw 200 as a perpetual growth engine” becomes a self-fulfilling prophecy, but the real story here is one of sustained and gradual consolidation rather than perennial prosperity:

- In 1998, the first year the American Lawyer expanded its rankings to the Second Hundred, the 200 highest-grossing firms in the U.S. collectively housed approximately 58,000 lawyers or 6% of ABA membership that year.

- Fast forward to 2019 and the collective headcount of the AmLaw 200 has more than doubled to about 134,000 or 10% of ABA membership.

- Since 1998, the AmLaw 100 has only contracted collective headcount once (if you guessed 2009, you would be right 👏).

Headcount growth provides plenty of self-contained noise within the AmLaw dataset, but the problems don’t end there. Historical trendlines and growth figures relying on nominal figures often tell a story that seems too good to be true, because it is (and most industry observers in the know don’t believe it). While the complete AmLaw dataset and ALM’s coverage provide greater granularity and fidelity, the most accessible figures tend to travel the furthest. Left unchecked, the quick-and-easy narratives give rise to misleading and ultimately unhelpful assumptions about incumbent firms and their competitive posture (💰 richer every year like clockwork ⏰) and strategic mindset (🥱 too complacent to care about clients, let alone innovation 🤷♂️).

The table below shows the real story (h/t to Bruce and Janet Stanton of Adam Smith Esq; this analysis is derivative of their work in past years).

The chosen timeframe (2010 to 2019) is noteworthy for a couple of reasons. Officially, the Great Recession began in December 2007 and ended in June 2009, so 2010 theoretically marks the first year of recovery, giving us a nice, clean, downturn-free decade between the 2008 GFC and 2020 pandemic. Once adjusted for inflation and headcount growth, however, we get a very different narrative about that decade.

Generally speaking, annualized revenue growth between 2% and 5% as reported in nominal dollars seems both plausible and fairly good. It’s just not representative of the lived experience of most AmLaw 200 firms. Revenue growth in any form doesn’t come easy and it definitely doesn’t come for free when coupled this tightly to bloating payroll. The adjusted figures essentially tell us that BigLaw takes 😨 bigger risks 😰 each year to grow. For their pains, they’ve barely stayed ahead of inflation in the past 10 years. (And that’s during the longest economic expansion in U.S. history.)

(ii) Post-GFC Recovery for the AmLaw 200 = More #FakeNews 🤥

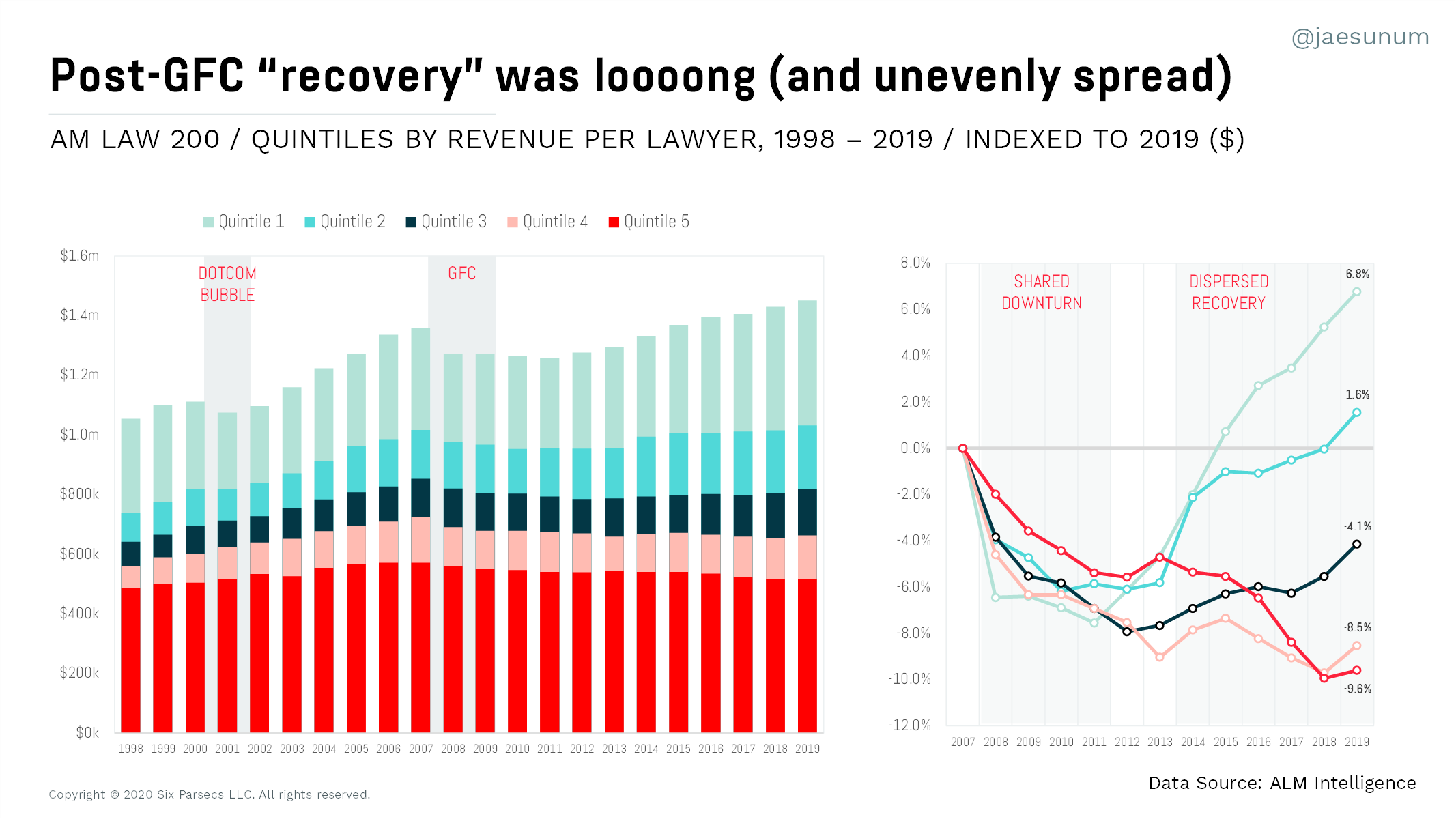

How did AmLaw firms actually fare during the boom years from 2010 to 2019? The below graphic depicts a single data set in two charts: historical AmLaw 200 firms and their revenue per lawyer (RPL) from 1998 to 2019.

- In the chart to the left, each bar represents the 200 firms with the highest grossing revenues in the corresponding year. Within each year, the AmLaw 200 is broken down into quintiles (200 firms in 5 groups of 40 firms in each group) using each firm’s RPL (revenue per lawyer) in that year: Quintile 1 in 1998 comprises the 40 firms posting highest RPLs in that year, Quintile 2 includes firms that ranked 41st to 80th in RPL, and so on. For clarity, this means that neither the bars nor quintiles contain stable sets of firms from year to year — a distinction that will become relevant very shortly.

- In the chart to the right, each line depicts the average RPL within each quintile group expressed as a percentage change from the pre-GFC peak of 2007.

Click to enlarge / Quintile analysis of RPL / Historical AmLaw 200 firms (n=294) / 1998 – 2019, indexed to 2019 dollars using CPI-U

The two graphs above present three points of interest:

- Lengthening the time period to 1998 and indexing all historical figures to 2019 allows a comparison of the dot-com bubble in 2000 and the GFC in 2008 – 2009. The dotcom bubble was shorter in duration and appears milder in impact, with fairly immediate recovery for all but the top quintile. In contrast, the 2008 crisis lasted much longer and is followed by a sustained period of stagnation for all quintiles. I suspect the longer duration of the Great Recession as well as the belt-tightening experience from 2000 enabled market players – primarily corporates clients – to formulate a multi-pronged and structural response. The number of in-house lawyers doubled from 2010 to 2016 as clients kept more work in-house and began to rebalance workloads across a more diverse supply chain from year to year.

- The chart on the right gives a better sense of how AmLaw 200 firms actually experienced that recovery, if at all. As a group, Quintile 1 firms (highest RPL performers) recovered to 2007 levels by 2015; the second quintile got there three years later in 2018. The remaining firms have yet to cross that milestone. In fact, the fourth and fifth quintiles have posted a downward trend in average RPL for most of the “recovery.” Of the 159 firms in the 2019 AmLaw 200 firms that operated under current shingles in 2007, 55 remain shy of their pre-recession peak based on inflation-adjusted figures.

- The chart on the right also provides a clear picture of steadily widening performance dispersion from 2013 onward, with the first quintile pulling further away each year since 2014. ALM has continued to report on this trend since 2014, when the inaugural Super Rich list was published, comprising 20 firms with RPL of >$1M and PPEP of >$2M. See, e.g., Press Release, “The American Lawyer Finds Am Law 100 Had Middling Year, While A Subset of Super Rich Firms Got Richer,” April 28, 2014, and Patrick Smith, “Straight to the Top: The Super Rich Drove Nearly All the Am Law 100’s Profits Growth,” The American Lawyer, April 21, 2020 (noting that the 30 Super Rich firms posted 5.1% growth in net income in 2019 compared to 2018 – taking the lion’s share and leaving only 0.02% average profit growth for everyone else).

(iii) For (Most) BigLaw Incumbents, ❄️ Winter Is Here 🥶

Taken together, I believe these data points give a more accurate portrayal of the AmLaw 200 position heading into the current downturn. In a word, I would describe that position as precarious. The various analyses of AmLaw data outlined here strongly suggest that at least 50 firms are facing imminent existential threats in the next 24-month period. Particularly when taken with market-wide observations on client and new entrant trends, I expect that we will see at least half a dozen shingles taken down for good before the end of 2022.

That is a rather grim prognostication relative to views I usually give about the future of law firms, so I add a word of clarification. I remain as bullish as ever as to the durability of the law firm business model (up to and inclusive of the billable hour). In fact, I’d venture a guess that at least 25 firms across the top echelons emerge from the current downturn materially bigger, significantly more profitable, and more securely positioned than ever before. Another group of 30 to 40 firms are likely to leapfrog the competition in their current bracket. (More on this in Parts II-IV of this series.)

C. 💬 Voice of the Client 2021: 👂 for the Signal in the Noise

Why does any of this matter at all? In every industry, commerce is a Darwinian exercise, and legal services is no exception. The answer is because these myths perpetuate misguided actions by all players. Even worse, they distract from the real issues that have left both the legal industry and profession in crisis.

To better understand how these dynamics play out, we need to shift focus to the buy-side position. Similar to the BigLaw analysis above, a historical lookback is instructive.

(i) What Clients SAY (on Panels and Interviews) and What Clients DO (with Their Budgets)

For as long as I’ve worked in and analyzed legal markets, corporate clients have decried what they see as explosive and unconstrained growth in the wealth of large law firms. Over the years, the perception of seemingly unbroken BigLaw prosperity (as measured by topline revenues and PPEP) has given rise to client complaints about the greed and excess of their outside counsel, ranging from associate salaries (too high) to Class A office space (too nice). See Caroline Spiezio & Dan Clark, “‘The Tone Deafness Is Astounding’: Clients Unhappy About Milbank Associate Raise Announcement,” The American Lawyer, June 8, 2018.

In many indignant discussions across enterprise legal buy, clients have demanded that law firms explain (and sometimes singlehandedly undo) the drivers of increasing legal spend. Those complaints have translated to decisions that apply intense and sustained pressure on law firms—primarily in the pricing arena. Too often, corporate clients conflate BigLaw growth with their budgeting difficulties, and the presumption of unchecked law firm wealth has led to an increasingly adversarial dynamic between buyer and seller. See Blog Post, “5.8.20: COVID-19 Crisis Series LAW FIRM,” Legal Value Network, May 8, 2020 (discussing implicit client resentments on law firm profitability and the myth of buyer-dictated prices). In the coming downturn, I fear those tensions will only intensify.

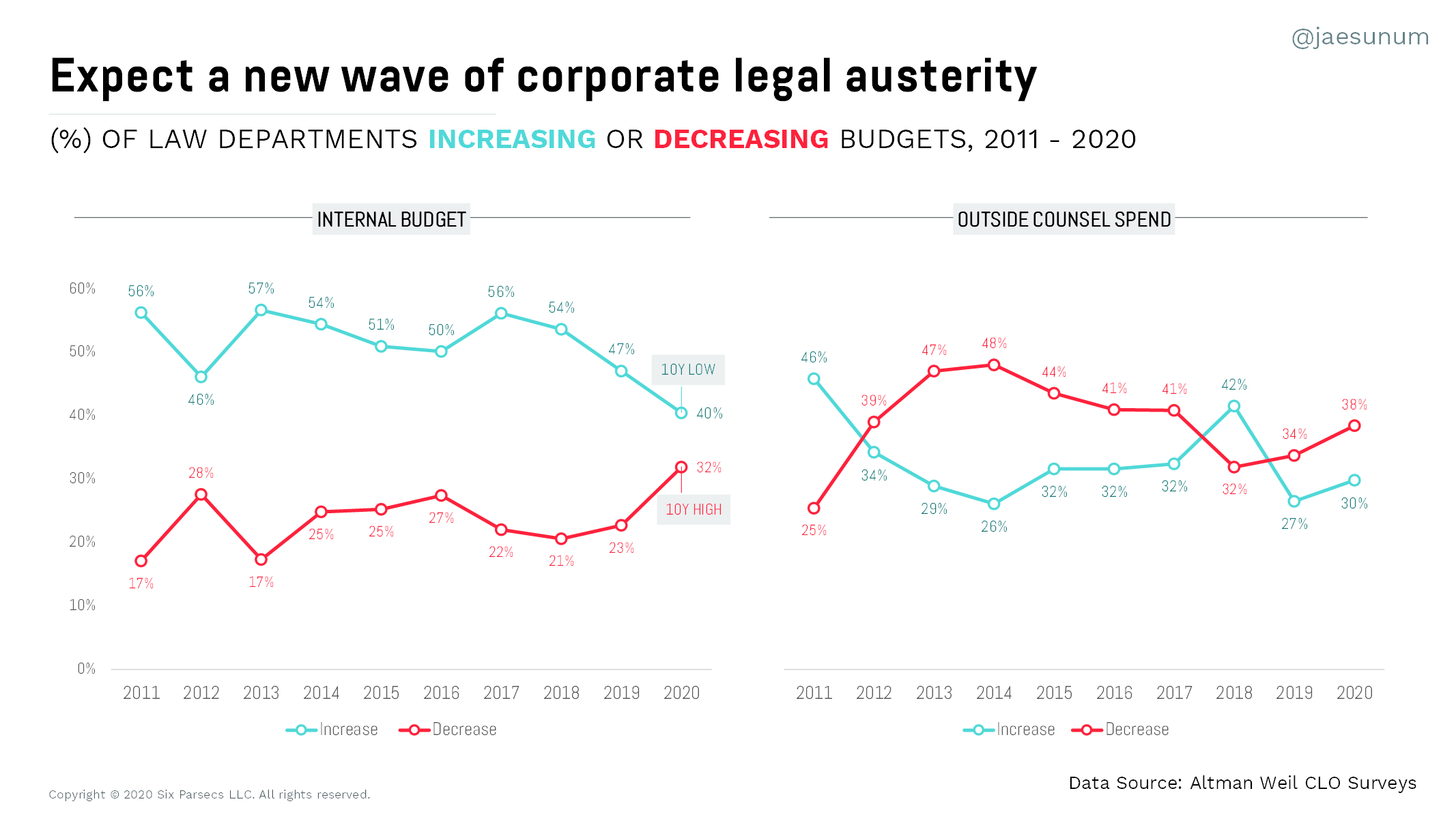

For years, Altman Weil has tracked changes to in-house legal budgets through an annual survey of Chief Legal Officers. The graphic below shows a 10-year history going back to 2011 (responses indicating flat budgets are omitted).

In 2020, 40% of CLOs reported increases to internal budgets while 32% reported decreases, marking ten-year low and high points respectively. On the right, 38% of CLOs reported decreasing outside spend in 2020, with 30% reporting increases. Taken separately, these figures tell a story of perennial belt-tightening on the buy-side: old news for anyone who’s listened to at least one client panel in the last decade.

A comparison of the two buckets turns out to be more instructive. From 2013 to 2017, the proportion of CLOs reporting decreases to outside counsel spend hovered at nearly double the proportion of CLOs reporting decreases to internal budgets. The Altman Weil data confirms that clients protect their internal budgets at the expense of their providers’ toplines (and suggests that BigLaw faced intensifying headwinds even prior to the current downturn).

Most signals indicate that CLOs head into 2021 with austerity in mind, with 40% of respondents planning on reducing outside counsel spend and 15% planning significant reductions of 10% or greater. Similarly, internal budgets are under pressure, though to a lesser extent: 34% of CLOs plan to decrease internal budgets, with 9% aiming for reductions of 10% or greater.

While self-reported data can only tell us so much, the Altman Weil data suggests that what we can expect from corporate law departments in 2021 is very much what we’ve seen in the Great Recession playbook… and that’s a problem.

In the same Altman Weil survey cited above, 77% of CLOs reported increased workloads in 2020 due to COVID-19, while only 40% of CLOs reported any increase to total legal budgets, leaving 37% of CLOs with a classic “more with less” problem.

Since the last downturn, corporate buyers of legal services have issued a challenge to their outside suppliers: (more) value for (less) money. Throughout that period, Thomson Reuters and Citi-Hildebrandt have consistently reported on “flat demand” for law firms. See also Post 214 (reviewing TR data). The natural tension across these two narratives is left largely unexplored and unexplained. It’s time to probe a bit deeper into both.

(ii) Flat Demand? The Biggest Myth of All 🤥🤥

In this context, “demand” is a term of art and financial KPI for law firms, measuring total billable hours worked in a given period. In that sense, it is accurate to say demand for law firm hours has been stagnant over the past decade. However, I get the sense that many conflate the “hours worked” KPI with the notion that the total workload for the enterprise legal market have remained constant. This could not be further from the truth.

“Demand” as defined narrowly above is a concept that is both distinct and far removed from its origins in classic economics, where “demand” refers to “the consumer’s desire to purchase [] and willingness to pay a price for a specific good or service … across all consumers in a market for a given good.” Semantics? Maybe, but for good reason.

Simply put, the enterprise legal market lacks reliable measurements to track changes to the buy-side demand for legal services. In a decade of truly lackluster growth for BigLaw, actual workloads generated by large corporations requiring legal expertise has undergone an invisible explosion—one that all industry participants feel in their bones but cannot measure. This leaves the corporate legal function in a perpetual budget squeeze — and their outside counsel edging dangerously close to the edge of an existential abyss.

D. 🐘🐘🐘 Elephants in the Room

Totally absent from myopic discussions of legal spend are three factors that actually drive corporate demand for legal services. Third-rail topics they may be 🤐, these are root causes of systemic ills with far-reaching impacts beyond the legal industry:

(i) Spend Reduction Is a Red Herring While Demand Remains a Mystery

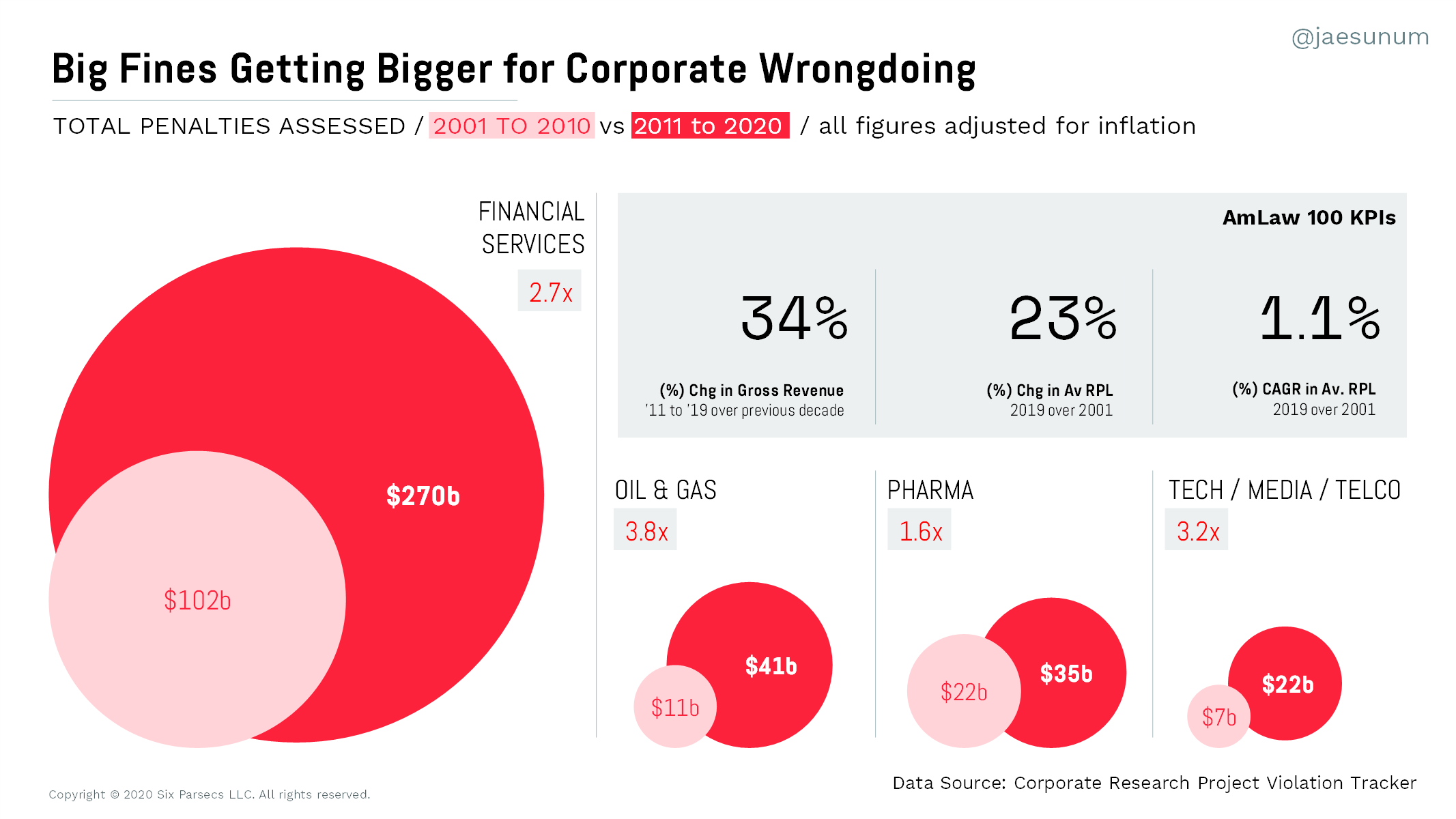

The below graphic provides a comparative analysis of data collected by the Corporate Research Project, covering 444,000 civil and criminal cases and $650 billion in penalties levied by more than 250 agencies since 2000. The chart below covers only four sectors — financial services, oil & gas, pharma, and TMT (tech, media, and telecommunications) — but 70% of all penalties reported in the database. As a proxy measure of corporate misconduct, these penalties provide a rather conservative signal. They are usually assessed only after prolonged investigation and litigation, often as part of a settlement agreed to by the companies involved.

Three interconnected factors explain this group’s disproportionate share of corporate misconduct.

1. Size and scale. Best estimates now place the global financial services at around $22 trillion, or just shy of 25% share of global GDP. TMT, oil & gas and pharma are relatively smaller, but the four sectors share another commonality relating to size: they are top-heavy, winner-take-most markets that are dominated by a few gargantuan players. After decades of consolidation, the market capitalization of global banking sector is pushing $8 trillion, while the Big 5 Tech companies now combine for over $6 trillion in market cap (FAMGA: Facebook, Apple, Microsoft, Google, and Amazon). Oil & gas has long been dominated by six “supermajors,” while the top 20 pharma companies tipped $2.5 trillion in combined market cap in 2019.

2. Regulatory burden. Historically, financial services, oil & gas, and pharma have long been heavily regulated, leading to relatively higher rates of legal spend. Mounting furor over data privacy and election security as well as growing concerns over ethical AI and protected speech are issues likely to entrench the TMT sector firmly in this group for the foreseeable future.

3. Systemic risk. The regulatory burden on these sectors is imposed for good reason. The aftermath of the subprime meltdown demonstrated painfully and clearly that a few global financial conglomerates wield immense power. More than a decade later, many companies in and outside of financial services remain too big to fail, and their size and scale are such that their actions reverberate across the world, in second- and third-order effects that are difficult to control. A spin through some of the largest corporate fines in history give a sense of what is at stake when the biggest corporations in the world engage in corporate wrongdoing:

- $20.8bn against BP (Deepwater Horizon oil spill)

- $16.7bn against Bank of America (subprime crisis)

- $14.7bn against Volkswagen (Dieselgate)

- $13bn against JP Morgan (subprime crisis)

- $8.9bn against BNP Paribas (sanctions violations)

- $5bn against Facebook (privacy violations)

(ii) Multiplying Risks and Exponential Workloads (at 🏷️ 15% Discount 💸)

From 2001 to 2010, these four sectors (financial services, oil & gas, pharma, and TMT) were subject to fines and penalties totaling $113 billion. In the following decade, from 2011 to 2020, that figure tripled to $339 billion. As a comparison point, the AmLaw 100 posted a meager 34% growth in combined revenues in the same decade-on-decade analysis. Point-in-time comparisons in 2001 and 2019, adjusted for inflation, show a 23% increase in revenue per lawyer.

Year in and year out, these four sectors tend to dominate BigLaw revenues. Simply put, the legal and regulatory risks for BigLaw’s biggest clients are multiplying. Meanwhile, law firms are struggling to post incremental gains. What gives?

Law departments across these sectors also happen to house strongholds of sophistication in legal buy. After all, they are usually the law departments managing the largest risk portfolios across the most complex supply chains. It is no coincidence that Big Banks, Big Oil, Big Pharma, and now increasingly Big Tech tend to be pioneers and early adopters of legal buy innovations, ranging from new buying mechanics and models (e.g. reverse auctions and AFAs) to supply chain redesign (e.g. panel convergence, diversification across BigLaw and NewLaw). Notably, these very same clients also tend to be BigLaw’s toughest customers on rates and discounts.

However, the data points above suggest that our collective thinking about the “more for less” challenge needs a reboot. In the last downturn, clients relied heavily on cost reduction levers to hit budget each year. In today’s market, what passes for pricing dialogue in most of the legal market remains a zero-sum game that usually devolves into haggling over discounts. See Blog Post, “6.5.20: COVID-19 Crisis Series LAW FIRM,” Legal Value Network, June 5, 2020 (summarizing flash poll responses of law firm leaders on client requests for cost reduction help and discussing client and law firm pressures to accept work at discounted rates). Heading into 2021, most law firms have already leaned out their back-office operations, squeezed more billable hours out of fee earners, tweaked their leverage models, and invested in basic service delivery enhancements like process improvement.

All of these remain incremental improvements to systemic cost efficiencies in the 10% to 40% range. A far cry from “flat demand,” we are likely contending with exponential and intensifying pressure on that system. Without structural changes to how we think about legal sourcing or the means of production, cost savings of this magnitude are simply insufficient as they will run into a brick wall in the form of vanishing law firm margins. In the next decade, both buy- and sell-side will need to do 5x to 10x more with less — and the cost-focused playbooks of the past are unlikely to close this gap, even with widespread law firm failures and continued provider consolidation.

The intrinsic tension between BigLaw’s growth imperative (read: make more money) and corporate legal’s perpetual grind to do more with less (read: spend less money) is bad for our industry. The resulting distraction, however, is bad for the world. It’s long past time to ask the really important questions. Why is corporate misconduct on the rise? How do we reverse the trend? How do lawyers working at the biggest companies and law firms in the world actually leave that world a better place?

(iii) 🧐 New-Look Robber Barons & Monopolies: All of This Has Happened Before and It Will Happen Again

In 2020, the World Economic Forum called for a “Great Reset” of capitalism to aim the post-pandemic recovery toward three main goals: (1) steer the market toward fairer outcomes; (2) ensure that investments advance shared goals and mitigate shared risks such as inequality and sustainability; and (3) harness innovations of the Fourth Industrial Revolution to support the public good, with emphasis on health and social challenges.

These are righteous and audaciously ambitious goals, with grave implications for our shared future. Lawyers have an important role to play in this Great Reset, and a myriad of data points suggest that we stand together at an inflection point in history:

🌎 Our planet on the brink. In a 2018 report by the Intergovernmental Panel on Climate Change, 90 climate scientists from 40 countries warned that we are 20 years away from irreversible consequences of global warming, a grim backdrop for corporate malfeasance with environmental impacts. In 2020 alone, we saw over 44 distinct “billion dollar” weather events, along with “apocalyptic wildfires” on multiple continents, tsunamis and floods in Asia-Pacific and a record-setting Atlantic hurricane season. See Judy Fays, “Billion-Dollar Disasters: The Costs, in Lives and Dollars, Have Never Been So High,” Inside Climate News, December 29, 2020.

💲 Dirty money everywhere. In a time when nationalist sentiment and income inequality are on the rise, financial institutions regularly run afoul of regulators for money laundering for drug cartels and terrorists, for violating sanctions against authoritarian regimes, and for widespread mistreatment of customers.

💻 Software eating the world. The rise of Big Tech has ushered in what some consider a golden age of innovation. We carry supercomputers in our pockets with 24/7 connectivity to goods, services, and people all around the world. This progress, however, has come at a steep price. While disinformation virality and fake news bubbles pose imminent threats to democracies around the world, the tech industry is just beginning to grapple with the wide-ranging impacts of moving fast and breaking things.

Apart from the malfeasance of isolated bad actors and the aggregate impacts of coordinated corporate greed, three other factors contribute to hot mess that is our current reality, in domains both squarely in and adjacent to the traditional province of lawyers:

Tech outpacing both legislation and regulation… Emerging technologies and platform business models enable Big Tech to play across categories, but leave legislators and regulators playing catch-up to untangle blurred lines across legal principles both uncharted (privacy) and well-traversed (competition). See, e.g. Shira Ovide, “Congress Doesn’t Get Big Tech. By Design,” NY Times, July 29, 2020; Shirin Gaffrey & Jason Del Rey, “The Big Tech antitrust report has one big conclusion: Amazon, Apple, Facebook, and Google are anti-competitive,” Recode, Oct. 6, 2020.

… against a backdrop of next-level regulatory complexity. In tandem with increasing complexity across the global economy, the regulatory environment around all businesses has long grown unwieldy. In 1988, the first Basel Accords filled 30 pages; in 2014, Basel III ran longer than 600 pages. See Jean-Edouard Colliard & Co-Pierre Georg, “Measuring Regulatory Complexity,” CEPR Discussion Paper No. DP14377, February 2020. A 2016 Competitive Enterprise Institute study estimated the annual cost for U.S. regulatory compliance and federal intervention at $1.9 trillion. See Nicholas Bruch & Jae Um “Are Wall Street Firms Built to Handle Today’s Financial Services Industry?,” The American Lawyer, August 19, 2018 (summarizing proxy measures of regulatory burden).

… and made worse by wild swings of polarized partisanship. Deregulation was de rigueur in 2016, with a crescendo of complaints from Big Business on the “crushing cost of regulation.” Part and parcel of a general hangover after four chaotic years of the Trump Administration, President-elect Biden and Democratic Congress will likely reverse the trend — but these extreme partisan swings are bad for business. Since the Clinton Administration, political polarization and legislative gridlock in the U.S. have given rise to increasing presidential reliance on agencies to make policy, subjecting businesses to the costs of untangling spaghetti rules and an expensive cycle of compliance updates every 4 to 8 years. See Elena Kagan, “Presidential Administration,” 114 Harv. Law Rev 2245 (2001) (discussing presidential exercise of administrative authority and predicting continued expansion of executive authority).

These problems are thorny and the stakes couldn’t be higher. We face dire threats to a fair and free society as well as existential threats to life as we know it on this planet. Still, the underlying beats offer some familiar echoes. The pendulum of history swings, sometimes in very wide arcs, but even the distant past can offer relevant and valuable lessons. At the intersection of law and policy, lawyers and judges pushed the U.S. out of the first Gilded Age to the reforms of the Progressive Era. As new robber barons clash with new trustbusters, the rule of law can and must adapt once again to new paradigms of commerce. See Ryan Cooper, “The return of the trust-busters,” The Week, January 9, 2018 (in-depth recounting of Justice Louis Brandeis and his role in the intellectual history of platform monopolies).

We Need Reality-Based Accountability for an Interconnected World

In coming years, lawyers in leadership roles have critical choices to make, in forums both private and public. Now is the time to dig deep and ask difficult questions about what we owe to each other and how our actions affect the world around us.

Big business and their legal counsel have the opportunity to steer capitalism to a gentler and fairer recovery, but the clock is ticking. The reckoning we face in the post-pandemic reality is not one of cancel culture but widespread calamity and increasing risk to our lives and livelihoods. Under such pressures, legal market participants can no longer afford the parochial short-termism and blame-based narratives of the past. In a zero-sum war of attrition, we all eventually lose.

Rebuilding capitalism with a conscience and focus on stakeholder value will be a long and difficult road. Broadening our shared frame of reference beyond legal spend reduction would be a good first step.