Is it time to take a fresh look at how we sell legal tech?

Clients and lawyers are attracted to technology because of the enormous potential for better, faster, and more efficient legal work. No one in the legal industry disputes that technology is integral to our future. Despite this relatively positive and uniform outlook, however, legal tech as an industry remains notoriously risky, primarily because of long sales cycles, limited exposure to potential issues and concerns of end-users, and lengthy deployments that fail to deliver on the many promises made in order to make the sale.

Yet, if we step back and look at the sales strategies used by some of the most successful pure technology companies, we observe that many are adopting Product-Led Growth (PLG) strategies that jump over the usual points of contact in large enterprises (e.g., the chief technology officer, IT administrator, operations manager) to solve a specific discrete problem for an end-user, converting him or her into an internal champion for company-wide adoption.

The above matrix summarizes the key differences between the Sales-Led Growth (SLG) model, which is nearly universal throughout the legal industry, including among very small start-ups, versus Product-Led Growth (PLG). The chart also includes many well-known tech brands that have used a PLG approach to fuel the massive adoption of their technology. Indeed, many of these brands are familiar to readers because lawyers and law firms are among the adopters.

For those of us in the legal tech community, is it time to take a fresh look at how we sell?

This post does not advocate an abandonment of SLG—not every technology and use case is amenable to the PLG approach. We do, however, suggest an evolutionary approach where we look for opportunities to solve discrete end-user problems as fast and as well as possible, thus shifting the dynamics from selling legal tech to expanding its use. To do this, we need to understand the biggest constraints and challenges of SLG (the dominant paradigm) as well as the key touchstones in the PLG playbook.

Sales-Led Growth (SLG)

The dynamics of sales in the legal industry are the same across all enterprise software businesses. It is what Venture Capital firm Andreessen Horowitz labels as “the old world of enterprise go-to-market”, in which technologies are mostly acquired through Sales-Led processes. See Peter Lauten & Martin Casado, “Growth+Sales: The New Era of Enterprise Go-to-Market,” Andreesen Horowitz, July 29, 2020.

The following typical attributes of a Sales-Led approach, which is the dominant approach in the legal industry, expand upon the short descriptions in the above lead-matrix:

- A Top-down Go-to-Market Approach. From a vendor’s perspective, the sales motion is aimed at buyers and influencers within the customer’s organization, such as CIOs or Legal Operations, as these decision-makers are crucial to making the sale. This model assumes that the total addressable market for legal technology falls within a relatively niche ecosystem of law firms, corporate legal departments, and to a lesser extent, alternative legal service providers. To illustrate, compare legal technology vendor presence at events like ILTA or CLOC (attended by more buyers than practitioners), with events such as the IBA, ABI, or other specialized practitioner associations. Notice that most of the Legal Tech’s marketing dollars and human capital are aimed at raising product awareness among buyers and less so the end-users (i.e., lawyers and other legal professionals)–even though the end-users are often the real equity owners of the firm and thus should be open to innovations that make them more competitive. Cf. Post 063 (Jae Um lamenting that access to buyers and access to users has been “uncoupled” in B2B sales, stifling legal tech’s potential).

- Delayed Time to Value. Months may pass between when the buyer becomes aware of a product and when an end-user can employ it in a valuable way. The opportunity cost for a non-technical legal practitioner to learn a new tool is very high, especially considering heavy workloads and billable hour requirements. Demo instances or trial versions are often not designed to provide immediate value to the end-user. Legacy technology rollout plans have entrenched expectations of legal practitioners who may have reservations on using the tool without offline handholding, onboarding, and sponsorship from the organization’s tech function. Assuming a user is fully onboarded, the software is still shelf-ware until there is a point of need.

- Professional Set Up and Deployment. To realize value, the software must be fully deployed, which means rolled out in compliance with the legal organization’s information security policies. To adequately function, it may also require integrations with other systems, such as identity authentication, document management, or billing software. The end-user (i.e., lawyer or another legal professional) won’t be able to fulfill the deployment themselves and the effort is likely to require weeks or months of planned work, in addition to paid professional services to help configure and train administrators and users.

- Sales Channels are Offline. Because sales-led growth is relationship-driven, go-to-market efforts are focused on positioning the vendor as a technology advisor and trusted source of solutions through activities such as thought leadership and trade shows. The goal is for a prospect to have a direct line of communication with the vendor as soon as a need arises. Lead nurturing techniques, such as Account-Based Marketing, help vendor and buyer speed through bottleneck phases of the marketing-sales funnel in order to get to a lengthy evaluation phase as quickly as possible, once an opportunity to solve a need has been identified.

- Technology is Positioned as a Capability. Because the enterprise purchase is very expensive and consequential, buyers often seek options through an RFP process or by informally comparing available products. Because buyers represent multiple stakeholders and end-users within an organization, there is a bias toward solutions that can solve the needs of the enterprise or a large amount of end-users. In order to remain competitive, vendors are incented to check the box on features and position their products as capabilities that can be extended for core and non-core use cases. This positioning can often be a stretch and require creative workarounds to apply a tool to a non-core use case. To illustrate how point solutions are positioned as capabilities, take a look at the ABA’s Legal Technology Buyer’s Guide. Marketing descriptions show how code automation and text extraction become AI engines; OCR and imaging becomes document management; time tracking becomes practice management; and so on.

We all stick with this approach because it is familiar and it has delivered the results we needed in the past. Yet, it is also partly responsible for slow technology adoption and end-users being underwhelmed with the promises and potential of what legal tech is capable of delivering.

Product-Led Growth (PLG)

In a product-led world, the product drives its own acquisition, activation, conversion, and expansion, as the product experience is part of the buying process. See, e.g., Wes Bush, “What Is Product-Led Growth & Why It’s Taking Off?,” Product-Led Institute, July 22, 2020. The graphic below illustrates the dynamics.

The key difference between SLG and PLG is that effort is focused on getting the product in front of the end-user so that it can be used immediately at the point of need. If the end-user is getting value, conversion into a purchase becomes almost inevitable. Thus, Sales and Customer Success teams are focused on supporting the expansion and nurturing of customers with higher lifetime values. The flywheel is reinforced through tactics that minimize off-product handholding. In the backend, usage data gathered throughout a unique user’s adoption journey helps personalize and improve the user experience. Analytics captured contextually reduce the need for intrusive offline and intermediated user feedback.

The following expands upon the short descriptions in the SLG/PLG comparison matrix at the top of this post:

- A Bottom-Up Go to Market Approach. Marketing campaigns are aimed at specific end-users. They communicate targeted value propositions around the job that the technology can do for the end-user in the context of their work. The go-to-market model is thus flipped on its head by generating awareness directly with the target end-user and making it simple for them to activate directly and without the intermediation of a buyer. The target addressable market expands beyond legal service organizations as the proposition appeals to users coming out of the woodwork of adjacent fields or functions (e.g., procurement, real estate, insurance, sales, etc.).

- Short Time to Value. End-users have frictionless access to the tool at the point of discovery. The product experience is positioned to solve a discrete need in a way that is understandable by the user. Trial or freemium versions of the technology are not a demo and pricing for paid versions is transparent and non-negotiable. These tactics remove price and contract negotiations as sources of friction that delay the end-user using and adding to their own work product. A good example of this is Atlassian, a publicly held software tool and collaboration company with $1.6 billion in annual revenue that publishes the prices for packages up to 10,000 users and publicly state they don’t negotiate terms and conditions. In the legal space, Atlassian’s most familiar product is Trello, a kanban-based project management tool.

- Do It Yourself (DIY) Deployment. Seamless onboarding is critical to user acquisition. The end-user can quickly set up the tool without technical support. They can self-educate and follow prompts to solve their need. The tool doesn’t require integrations or has designed workarounds, such as file importing/exporting capabilities, that are not limiting to the product experience. Paid versions of the technology may require deeper integrations or a planned rollout, but the end-user can deploy and obtain value from the solution before seeking an enterprise-grade deployment.

- Online Sales Channel. The segmentation of users is based on need. Behavioral data and digital marketing tools are leveraged to find and target individual persons that have a specific need that the product maker can fill. A good example of this is Canva, a graphic design platform that allows users to create social media graphics, presentations, posters, documents. Canva creates two landing pages for each of their thousands of potential use cases. The first page is for discovery and the second is for creation. This enables the end-user to make a purchase or installation through purely online interactions. The online sales motion is focused on acquiring users before converting them into paying customers. The model relies on virality and network effects. Delighted users become the product champions that help upsell the tool with their organization’s buyer. The product’s go-to-market model is designed to provide incremental value to the end-user if the adoption of the technology is scaled within their organization or with users external to their organization.

- Positioned as a Point Solution for a Use Case. The technology is positioned as capable of solving a specific job for the end-user. Whether they need to run a quick document comparison, execute an electronic signature, share heavy files with their clients or validate market terms for a transaction; the technology can do one job at the point of need. Even if a technology can be applied to multiple jobs or use cases, the onboarding journey will be unique for users fitting each use case. A good example of this is online database company Airtable, which offers a library of templates for their most common database types by category. Cf. Post 196 (Seth Saler using Airtable to track his projects while interning in Cisco’s legal department).

Why is PLG taking off?

The move to Product-Led Growth is a natural response to changing market conditions in the wider software industry. The rise in the number of software providers has shifted the balance of power from software providers to end-users. As a result, software providers must now go to market in a way that suits end-users.

But what has driven this shift in power?

- Rise of Cloud Computing: The relative cost and availability of cloud computing has reduced barriers to entry, thus dramatically increasing the number of software providers. In turn, the lower costs of entry enable companies to focus on ever-narrower niche markets as a way to “cross the chasm” and become a viable operating company. See Post 024 (introducing readers to Geoffrey Moore “Crossing the Chasm” framework).

- Consumerization of IT: End-user expectations for software in the workspace have been elevated through consumer experiences (e.g., Netflix, Amazon). As a result, end-users are increasingly willing and allowed to seek out their own software solutions for the workspace.

- Higher Cost of Customer Acquisition: Increased competition has driven up demand and thus prices for advertising space on what was once considered cheap digital marketing channels such as Google and LinkedIn.

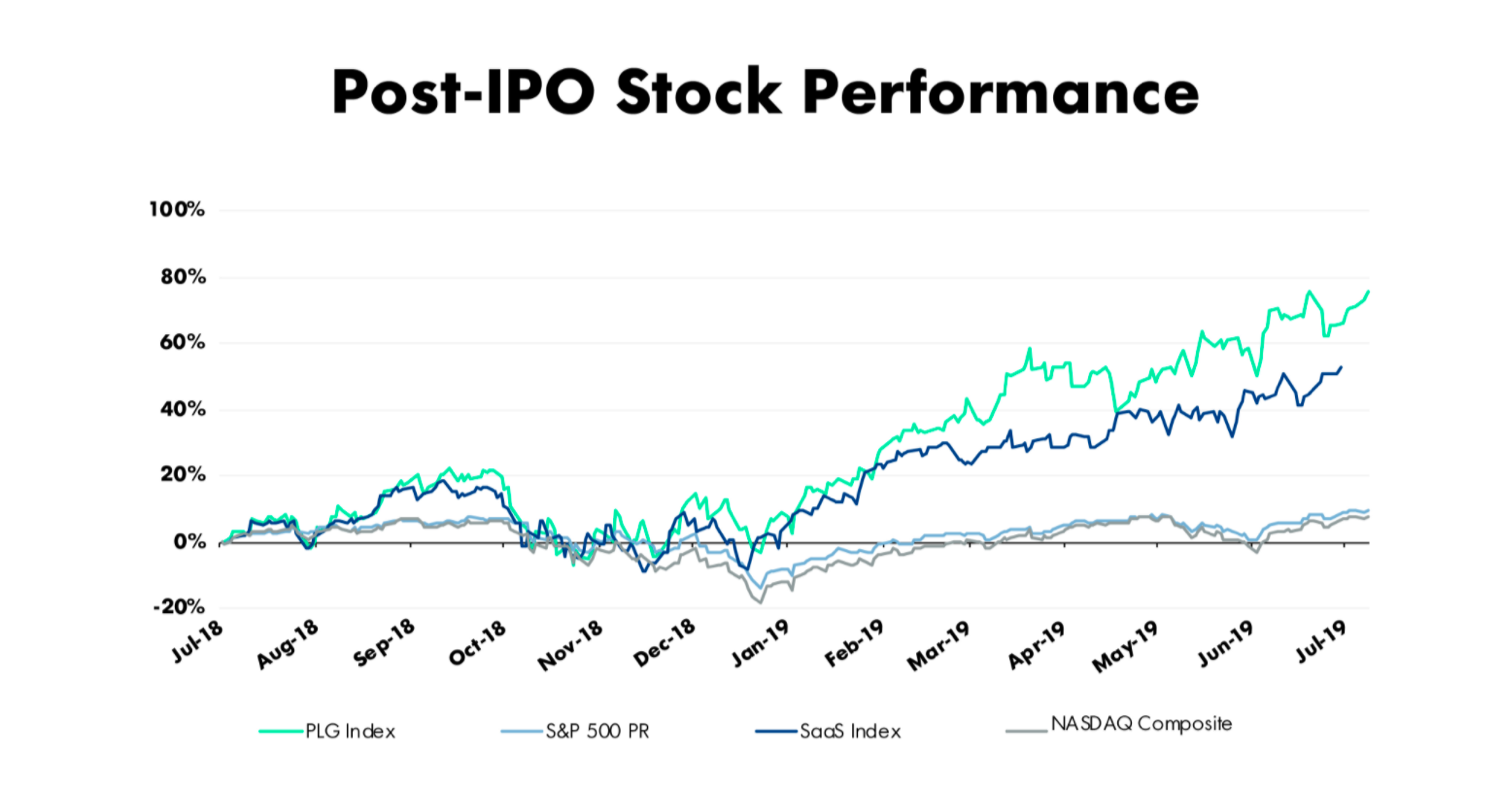

Nonetheless, user acquisition and technology adoption doesn’t make business sense if usage cannot be converted into sales growth. Perhaps counterintuitively, recent studies by Profitwell and Openview Partners find evidence that companies that operate Product-Led strategies experience a number of benefits compared to other SaaS companies:

- Slower increases in the cost of customer acquisition

- Higher rates of customer retention

- Faster increases in stock prices. See below graphic.

Another PLG benefit is the ability to more rapidly expand internationally, as companies using the PLG strategy are spared the time and cost of hiring sales teams. Two of the pioneers of the Product-Led approach, Slack and Atlassian, have customers in 150 countries and 190 countries respectively.

Can PLG work in Legal Tech?

An argument can be made that the Product-Led approach has yet to arrive in the Legal Tech space. Few vendors publicly offer freemium models or free trials. Pricing is not published on websites, and even start-ups in the space quickly create sales teams to develop relationships with the large global firms.

An interesting experiment is to compare the home pages of a selection of Legal Tech start-ups with tech start-ups operating in other industries. The overwhelming majority of Legal Tech start-ups have Request a Demo as their call-to-action, whereas the default for tech start-ups in other industries now appears to be Try for Free or some variant on the theme.

Like with many forms of digitalization, the COVID crisis could accelerate the pace of change. Since the start of the crisis, we have seen a few sales led companies dipping their toes in the product-led water by marketing directly to end-user lawyers and making elements of their service or technology available for free and for (almost) immediate use. Litera Transact (transition management solution, formerly Doxly) and Knowable (contract intelligence and management solution, which spun out from Axiom) come to mind, though their approaches seemingly still require off system interactions with sales representatives for onboarding to use. As expected, automated free trials seem to be more readily available with content solutions, such as Thomson Reuters Westlaw, Practical Law, or Casetext, since these products tend to be intuitive “out-of-the-box” for attorney end-users.

![]() However, there are a few cloud-native applications designed for smaller legal organizations, where the buyer and user are frequently the same people. Clio does a particularly good job at not positioning a full practice management system out of the gate and, instead, prompting the end-user (e.g., a lawyer unfamiliar with generating invoices) to follow steps to perform this task, as a way to begin onboarding onto the system. The question here is whether the offering of value that can be obtained from performing discrete tasks (e.g., generating invoices) in a 7-day free trial of the system is representative of the value of the entire proposition (e.g., practice management).

However, there are a few cloud-native applications designed for smaller legal organizations, where the buyer and user are frequently the same people. Clio does a particularly good job at not positioning a full practice management system out of the gate and, instead, prompting the end-user (e.g., a lawyer unfamiliar with generating invoices) to follow steps to perform this task, as a way to begin onboarding onto the system. The question here is whether the offering of value that can be obtained from performing discrete tasks (e.g., generating invoices) in a 7-day free trial of the system is representative of the value of the entire proposition (e.g., practice management).

Often overlooked is that Docusign, a poster child for the Product-Led approach, came from the Legal Tech industry. The value proposition of their e-signature product is clear (i.e., sign a document to make it legally binding). Onboarding is seamless. An individual user can open an account for free and collect the e-signature from a user that doesn’t have an account. A free version can deliver a signed document and, with it, value. Pricing is transparent and based on the number of documents and users. Users of the product drive conversion into enterprise accounts. Penetration of the technology is ubiquitous in legal organizations today. However, the same technology is positioned to collect signatures beyond law firms, including in much larger customer segments such as financial services and sales organizations.

Often overlooked is that Docusign, a poster child for the Product-Led approach, came from the Legal Tech industry. The value proposition of their e-signature product is clear (i.e., sign a document to make it legally binding). Onboarding is seamless. An individual user can open an account for free and collect the e-signature from a user that doesn’t have an account. A free version can deliver a signed document and, with it, value. Pricing is transparent and based on the number of documents and users. Users of the product drive conversion into enterprise accounts. Penetration of the technology is ubiquitous in legal organizations today. However, the same technology is positioned to collect signatures beyond law firms, including in much larger customer segments such as financial services and sales organizations.

With these powerful proof points, will we see an acceleration in the use of Product-Led approaches in the Legal industry? Considering that many of the drivers noted above were previously playing out slowly in the legal industry but are now being accelerated out of necessity due to the COVID-19 pandemic, the likely answer seems to be “yes.”

Coexistence of SLG and PLG adoption models

A perceived blocker to the adoption of Product Led from a vendor’s perspective is that a Product-Led approach means giving up the Sales-Led tactics that have worked so well in the past.

Our research indicates, however, that going to market in a Product-Led way does not preclude the continuation of Sales-Led tactics. In fact, the most successful companies appear to be moving to a hybrid of both approaches depending on the customer segment, product, or Geography. For instance, Sales-Led tactics align with serving customers with potentially high lifetime value (CLV) and with selling products that require heavy customization, proprietary training data, or managed services to achieve value for the end-user and the legal service organization. On the other hand, Product-Led tactics work especially well where the customer acquisition cost (CAC) is prohibitive for sales teams and where the job to be done by the tool requires no customization and is well addressed by the application.

The key mind shift between SLG and PLG is that revenue cannot grow without product usage. Thus, extreme focus on the user experience and on immediate value delivery is critical. The second-order effect of product-led growth is accelerated adoption of the technology by the legal service provider’s end-users. Sales and Customer Success have a role to play in sustaining and expanding usage but less so on initial user acquisition. This results in the reduction of shelf-ware products purchased by the legal service organization and on higher customer retention. It’s a virtuous cycle for both the vendor and the buyer.

Complementary accelerators for Legal Tech adoption

The effects of COVID combined with wider implementation of Product-Led models can accelerate the slow rates of technology adoption that are so pervasive through the legal industry, with benefits for clients, practitioners, firms, corporate legal departments, and technology vendors.

Yet, to achieve these benefits, both firms and vendors need to be willing to change behavior. Below we lay-out the five changes we see as most vital to unleashing the PLG opportunity.

- Develop end-user relationships. Vendors need to develop deeper relationships with actual practitioners, not just the CIOs and CTOs they speak at Legal Tech conferences. These relationships will not only open-up additional ‘bottom-up’ go to market channels but the richer insights will flow through to better product design.

- Build freemium and self-service channels. The number of steps built into traditional sales processes not only increases friction in the sales process, delaying time to value, but it also restricts audience size. Vendors who successfully create freemium versions of their product, so that potential users can access without the need for demos, price negotiations, and signing contracts, will find they are building a pool of advocates for the paid version of their product among end-users. In addition, the reach could easily extend to new and far-flung geographies.

- Embrace the Cloud. Numerous studies have validated that law firms are migrating to cloud-based solutions. See, e.g., “The Power of the Private Cloud,” ABA Law Practice Division, Oct. 8, 2019; Travis Howe, “Law Firms Turning to Cloud Technology for Increased Data Security,” Law.com, Dec. 10, 2019. However, the perception that law firms are conservative when it comes to approving and implementing new technology reduces the incentives for attorneys to seek out potential new solutions. If technology leaders in law firms can provide a more constructive and open framework for the use of cloud-based solutions, they may empower end-users to play a greater role in finding and adopting the best technology solutions, enabling them to make better use of their technology budgets.

- Platforms and integrated experiences. Vendors must design products with functional interoperability in mind. To position a tool as a point solution, integrations must go beyond data synchronization. The product should seamlessly extend the user’s experience as they navigate between multiple applications to perform a task in the context of their work. Blake Bartlett, a partner with Openview Venture Capital, describes this process nicely in speaking about Trello’s integration with Slack.

- Collaborate to improve technologies. Buyers and end-users need to understand that a non-proprietary technology is not a competitive advantage. Rather, a competitive advantage is only possible by applying technology to the service of clients in a differentiated way or through a more valuable user experience. In Legal Tech, there are many technologies that require training, templating, or customization. Collaboration, often in the form of open source and collaborative projects, such as those hosted by GitHub, has been key to making technology useful and usable for specific cases in other industries. It shouldn’t be different in Legal. For example, Alejandro Pérez, a legal technologist in continental Europe, makes an excellent case for why law firms should be teaming up to train contract review software. See “Law firms collaborate on artificial intelligence training,” Legal Business World, Aug. 20, 2020.

Concluding thoughts

A Product-Led approach does not commoditize, through automation (or a “digital experience”), the relationship between a vendor and a buyer.

Rather, PLG is about shifting the human interaction between vendor and client away from pre-sales and focusing it on the post-sale (growth and adoption) motion. It doesn’t preclude the post-sales need for Customer Success teams, but rather it enhances their ability to empathize and offer valuable insight to end-users, through the availability of usage data, analytics, and monitored interactions. PLG enables Customer Success teams to expand the client’s lifetime value. PLG doesn’t disenfranchise the buyer within the legal organization, but rather it empowers them by helping them accelerate the software’s time to value and eliminate shelf-ware from the firm’s technology stack.

But perhaps most of all, legal practitioners should not be considered special snowflakes when it comes to technology adoption. Implementation, adoption, and change management techniques used by legal service organizations today have largely been imported from adjacent, and often more highly regulated industries. Product-Led adoption is a well-established trend in other enterprise software categories. The benefits of this approach to technology adoption in legal professional services should be no different.