Microsoft is pushing legal buy and provider engagement to the next level and asking their primary firms to come along. Here’s why it matters: they’re thinking bigger, committed for the long haul, and bringing a STEM mindset to legal innovation.

Trying something new is 😨 scary. Doing so in public ramps up the 😱 fear factor. Some of that is due to the evolutionary survival instinct hard-wired into our brains. We are social animals, and for millennia our very existence depended on our ability to gain and sustain acceptance by a tribe who would share the arduous work of evading both starvation and predators.

Fast forward to 2018. Trying something new in front of an audience of one’s professional peers still carries real stakes — and so it takes a special kind of courage to do so. On September 20, I was lucky enough to be present for several acts of courage, at Microsoft’s Redmond Campus where over 150 people convened for the company’s Trusted Advisor Forum. See Post 068 (explaining the design of the Trusted Advisor Forum event and the broader Strategic Partner Program).

I’ll let Casey Flaherty, the architect of the Trusted Advisor Forum, set the scene:

In brief, Microsoft invited select outside counsel, many of whom belong to its Strategic Partner Program, to come present to Microsoft, to each other, and to several other corporate clients in attendance. The presentation prompt was simple:

- Tell us one way have you have gotten better in the last year

- Tell us one way you will get better in the next year

The hypothesis being tested is whether clients need to actively engage with their law firms to drive innovation in legal service delivery. A core premise of the Forum was that our current approach is broken—i.e., nebulous complaints from clients about failure to innovate (or use technology or be efficient or other amorphous laments) are insufficient to incent meaningful action. Lack of specificity and accountability create ambiguity for consensus-driven organizations (law firms) where collective-decision making defaults to stasis.

I’ve written before, at length, about the adverse impacts from clients criticizing firms publicly and anonymously, see Post 054, but Flaherty diagnoses the most critical issue more concisely here. Such complaints tend to be vague. That vagueness engenders ambiguity and precludes accountability. The Trusted Advisor Forum initiative was purpose-built to cure this ill, and I believe it will, in time, show its efficacy. But the Trusted Advisor Forum is but one piece of a much larger puzzle: firstly, Microsoft’s Strategic Partner Program and secondly, the broader legal buy and provider engagement strategy that underpins it.

Bill’s commentary from the event (068) sets forth his views on the factors for and against the eventual success of Microsoft’s efforts. In this post, I offer some thoughts on how we might improve the odds for success — and why I believe it is an absolute imperative for the industry to (a) pay attention to the Microsoft experiment and (b) give the hypotheses driving that experiment every consideration and opportunity for the necessary trial-and-error.

⚠️ Fair warning: this post is #longform in the #extreme, even for me and even for Legal Evolution. Maybe grab a drink ☕️ or 🍺 or perhaps a survival kit first. (I invite everyone to blame Greg Lambert, who recently made known his wish for a 10,000 word post… although that may just have been to win a bet with Marlene Gebauer.)

I. The Obvious Questions (Though Not the Most Important)

Since I returned from Seattle, the question I’ve been asked most often is some variant of how the presenting firms performed at the Trusted Advisor Forum. More often than not, the questions are couched in a tone of curiosity tinged with skepticism. (Were the presentations good? Was I impressed by the innovations presented? Did I believe the innovations were real? Will the firms actually do anything?)

I get the skepticism. The legal market is a bit fatigued with talk of innovation, and a general air of distrust often follows on the heels of hype. Because I think both the hype and the distrust are bad for the ecosystem, I will actually address all of these questions here. The answers may be (much) longer and more fulsome than expected or wanted (I know everyone who knows me is shocked 🤯 and saddened 😢 by this).

I should note here that Jason Barnwell, Microsoft’s Assistant GC for Legal Business, Operations and Strategy, invited me to the event with the expectation I would write about it. Part of that expectation was that I would do so objectively, with both context and candor. On whether I deliver on that expectation, you’ll be the judge.

Who Showed Up (and Who Didn’t)?

I won’t list the names of the firms here, but instead give an aggregate summary.

- Of the 17 teams invited across two rounds, 4 simply declined to participate.

- Of the 13 teams presenting, 6 elected not to tell a retrospective innovation story.

Many will take this as an indication of the deplorable state of affairs in our industry, but I see it a little differently. One valid (but not sound) assumption might be that 7 of Microsoft’s primary legal service providers could not produce an example of how they’ve improved anything at all in the past year. This assumption may well be true, but I don’t think it is the best (or most helpful) read on the situation.

Microsoft’s actual ask was quite structured, although it left firms a wide berth for creativity (first round of 👏👏 to Flaherty-Barnwell): the 17 firms were asked to present on innovations that did (if in the past) or would (if in the future) result in (a) demonstrable improvement (b) of service delivery (c) to Microsoft. This is a very specific assignment. Though understated, it implies a high bar for inclusion and participation in Microsoft’s go-to roster of law firms (more on that below).

In any case, a very defensible analysis of participation rate tells us that nearly half of Microsoft’s primary providers did not or could not come up with a credible story of how they had pursued demonstrable improvement of service delivery to this specific client in the past year. In fact, I’d call for a second round of muted 👏 for their honesty here, though I hope they will be better positioned in future. After all, it was Casey Flaherty himself who hilariously took law firms to task for their apparent inability to say nothing even when they have nothing worth saying. (In furtherance of his view, I should note that not all presentations hit all three marks — but most of them did.)

How’d They Do? (I’ll Get to That… in a Hot Minute)

Before we get into this, a few additional notes on the mechanics of what we did there that will inform the rest of this discussion.

- The participation rate broke down to 20 presentations: 7 retrospective and 13 forward-looking innovations were presented.

- The participants were asked to provide real-time feedback using a structured form (of my design). This form asked the audience to determine whether the presentations were responsive to Microsoft’s request along each of the three dimensions and it did include a few scoring and rating elements: (a) presentation clarity, (b) the materiality of the problem being addressed by the innovation and (c) level of respondent interest in learning more about the presented solution. The Microsoft team has this data now; I expect they will be sharing their analysis with the presenting firms, and perhaps more broadly in future.

- I used a different form (again of my own design) to capture my reactions in real-time. The primary purpose of this particular form was more to categorize the stories presented along several dimensions, and all categorization elements allowed for multiple categories for each story.

- Type of innovation. See Post 063 (identifying 5 broad categories of legal innovation plays)

- Type of problem being addressed.

- Type of solution levers considered and deployed/proposed.

- Type of value the innovations did or could deliver to the client

- Type of value the innovations did or could deliver to the firm

The form I used did have scoring elements, but I’ll emphasize here that they reflect my views only. My reactions to specific presentations are of little utility to the market at large, so I place more focus on a topline analysis of the group as a whole, as well as the categorization breakdowns of the content presented.

My goal on site was to capture my reactions and notes in a more structured format and in real time to facilitate more reliable reporting. To the extent I provide commentary here, the purpose is to contextualize the rating elements and also to provide additional feedback on the presentations I found to be most compelling. In highlighting just a few of the presentations, the intent is to provide constructive and specific guidance for future reference, in hopes that the comments will help a broader audience leverage their innovation investments more effectively.

Last disclaimer: the sample size of participants and projects presented here are both too small to extrapolate broad generalizations of the current state of play, but I believe they do provide anecdotal snapshots that are suggestive, if not instructive. Again, you’ll be the judge.

But First… 😇 What Makes Innovations “Good”? 🤔

This is often treated as a subjective question. We ought to question that assumption — if only for the reason that it’s more helpful to would-be innovators and change agents to think more specifically and tangibly about the mechanics across concept and execution phases of their work. That will require some objective parameters. Here’s the thinking behind the parameters I used.

Innovations don’t spring into existence fully formed. They are born as ideas, and most ideas come into the world in pretty much the way humans do (fragile, messy, basically unintelligible for a while and in need of care and nurturing for years). Unlike human babies, however, ideas aren’t born with a right to life. Nurturing an idea to execution at scale usually takes time, effort and therefore money. In commercial settings, a critical capability of innovation teams is to exercise rigor and discipline in managing a portfolio of ideas through validation and culling.

At the idea stage, our first tendency is to evaluate ideas for novelty or originality, but this often leads innovation teams astray. Why? Because novelty and originality are too unbounded; these questions often work to impede rather than facilitate effective validation. Novelty is in the eye of the beholder while originality is often tied closely to the vanity of the innovator, and so it very easy and often tempting to keep our ideas on life support for way too long.

And some ideas do come to us suddenly in random places, like the shower. There is a pleasing air of delightful serendipity and implied genius to this notion, but it’s not very helpful for teams charged with driving innovation programs forward on demand or on schedule. (I suppose we could all take 🚿 long showers 🚿 and wait for a flash of inspiration to strike, but the #showerthought approach is risky and will seem even riskier come budgeting season. Plus, we’d all get pruny fingers.)

This is where the technical innovation toolkit shows its value: there are many structured methods and frameworks to help teams generate, validate and iterate on ideas. (In fact, innovation does sometimes come in a box). The graphic below is another example that maps well to the Trusted Advisor Forum: the Value Proposition Canvas from the team that popularized visual tools to drive business model innovation.

Innovations don’t exist in a vacuum. They create business value by solving business problems; sometimes, innovations create new gains that are as yet unconceived, but most often innovations work by relieving a known pain. For this reason, the most important element to consider at the idea/concept phase is the quality of problem statement, following by considerations of materiality and scale. Both questions should be validated with strong customer-orientation. In essence, the follow-up research and testing must determine, in an evidence-based manner, whether the problem really matters to a large enough number of paying (and preferably loyal and/or strategic) customers.

At some point, innovations must actually work. When evaluated against the backdrop of a problem that really matters, the controlling question becomes rather obvious: feasibility of the proposed solution. Feasibility here implies far higher bar than a single instance of conceptual proof: that tells us the idea can work. The feasibility bar for innovation in a commercial context is much higher: the proposed solution must work reliably, for real users in real-world conditions, at a workable price and effort — and usually, innovations must deliver material benefits over existing solutions to justify the switching costs.

Real validation and testing for both dimensions requires intentional and frequent contact with reality: problem statements must be tested with real users and feasibility can only be proven out through building and testing. Although I enjoyed the presentations at the Microsoft Trusted Advisor Forum, sitting through a 15-20 minute talk does not represent a rigorous application of either dimension. Based on that rationale, perceived problem quality and perceived solution feasibility are the two primary parameters I applied to the innovations presented at the Microsoft Trusted Advisor Forum. In essence, the scoring mechanisms reflect whether the presenting firms successfully articulated a compelling problem statement with sufficient attention to the customer perspective and a credible proposal for a solution that demonstrated sufficient consideration of the factors driving feasibility.

Lastly, the parameters I applied matched up well with the overall structure and design of the Trusted Advisor Forum. Prior to September 20, the participating firms were asked to first submit a project canvas articulating the problem, proposed solution, key metrics and the value proposition. (Another round of 👏👏 to Flaherty-Barnwell.)

Let’s Try Again: So, How’d They Do?

Overall, I genuinely thought the presenting firms did well. (More 👏👏👏!)

I’ve said it before many times, but I’ll reiterate here my respect here for anyone who takes a risk by trying something new, particularly in an audience of peers in a professional context. The Microsoft Trusted Advisor Forum is itself an innovation: something new they are trying as they explore to test their hypotheses. One of the core values underpinning Microsoft’s efforts is a commitment to open and candid feedback. In that spirit, I declined to rate the presentations on any kind of curve.

Despite being subject to a rather stringent set of standards, the presentations still fared relatively well.

- (Perceived) problem quality: 50% of the presentations scored 5 or better on a 7-point scale, with an average score of 4.7.

- (Perceived) solution feasibility: 40% of the presentations scored 5 or better on a 7-point scale, with an average score of 4.1

Of particular interest, retrospective presentations performed significantly better on both dimensions relative to future presentations.

| Perceived problem quality | Perceived solution feasibility | |

| Past | 5.1 | 4.3 |

| Future | 4.4 | 3.6 |

This, of course, makes sense. It is difficult to think specifically and tangibly about problems and solutions in a vacuum: even refining a problem hypothesis usually requires direct interactions with users — a practice that is rare in our industry due to inefficient access. See Post 063 (discussing market access as one of three key structural barriers to innovation).

A Few Suggestive Trends

Again, the sample size of 20 innovation stories is not representative of the market as a whole. But it is a snapshot, and some of the trends are definitely worth reporting.

- Better and faster win out over cheaper: Over 70% of the presentations focused on delivering “better” services. In comparison, 60% were designed to deliver “faster” services and 50% to deliver “cheaper” (i.e. price reductions to the client). In my view, this is a positive development for the entire ecosystem. It’s not realistic to expect law firms to resign themselves to competing on price only, and clients should reward an industry-wide innovation agenda that drives quality and velocity improvements to services.

- Most of the ideas presented will need to grapple with scalability (sooner or later): Over 80% of the presentations would eventually investment into the firm’s overall platform to enhance service delivery capabilities. This is noteworthy because such investments often lead to infrastructure improvements, and those usually require validating for at-scale rather than account-specific deployment (e.g. delivery to clients other than Microsoft).

- We’ve got a lot of problems to solve: There was no clear winner in the type of problem targeted by the firms: coordination costs, intra- and inter-organizational visibility, reducing costs of usable data all tipped over 50% share of the innovations presented. This suggests a complex operating environment for legal businesses for both buyer and seller, and at least in part explains the diversity and variety of innovation efforts that abound in the current state of play.

- We’re definitely learning to remember that process matters, but still cagey about changing incentives: A clear majority emphasized process improvement as a solution lever. This also appears to be a positive development away from pure-play technology innovations (because many tech-led initiatives often fail without the attendant changes to supporting processes). That said, only 12% of the presentations addressed incentive changes for people (although it is very possible that some presenting teams omitted those particulars given the open forum).

How the Trusted Advisor Forum Might Improve

Next year, I would love to see two structural changes to the Trusted Advisor Forum. I touched upon these in a looong podcast discussion with Barnwell, I but reproduce them here.

- More direction from the Microsoft team on pain points to address.

- More integration of end-users of services (i.e. Microsoft internal clients) to help outside firms test and iterate.

A few standout teams, highlighted below, did a fantastic job focusing their efforts on material problems that matter to Microsoft. Unsurprisingly, the same teams also fared better than most in articulating their thought process around feasible solution hypotheses.

Based on the presentations I saw, I think it’s likely that many firms struggled to scope and focus their efforts. To this, I want to add two points: (a) it’s OK that they struggled; (b) the best fix isn’t for those firms to get smarter on their own or try harder next time, but for the voice of the client to provide additional clarity.

If you’ve gotten this far, you’re not allergic to long reads, so perhaps you’ve gotten past the title of “Unless You Ask.” If so, you’ll know the client’s role doesn’t end with simply making the ask. The crux of the Flaherty-Barnwell thesis is structured dialogue, and the mission is to advance the industry beyond a one-way request from clients for firms to improve to a two-way exchange of information, insights and ideas.

Some of the information and insights that the client must provide pertain to the pain they’re feeling and the missed opportunities they’re seeing. It’s worth noting here that establishing that client perspective is itself a significant challenge: while we might reference Microsoft as a monolithic entity or reference Barnwell as the appointed spokesperson, the corporation itself has no sentience and we’re not talking about the personal viewpoints of Barnwell himself. The reality is that the most critical pain and high-value opportunities for the company are felt and experienced by hundreds of individuals across the legal and corporate environment. That’s why starting and sustaining that dialogue takes work, from both in-house and outside counsel. But I am confident Barnwell will keep up his end of the deal and forge ahead with the necessary work of sussing out what matters most to his internal clients.

The open-ended nature of the prompt was optimal to start the initiative. As the Trusted Advisor Forum advances in maturity, I think interesting opportunities open up for the Microsoft team to direct and influence the path of law firm investment in innovation. As some of these innovation efforts mature toward building, testing and iteration, Barnwell is well-positioned to attack a key structural problem: access to end-users of services. If the Microsoft team can help its outside firms focus their innovation investments toward problems that matter and pull together working groups comprised of buyers and users from across its business to help outside counsel teams validate problem and solution hypotheses, that creates material lift to the upside potential of the Trusted Advisor Forum.

II. No Participation Trophies 🚫🏆🚫 Here: Instead, a Few Bright Spots ✨

With express permission from Barnwell, I’m highlighting a handful of presentations that I thought were most successful. Again, the ratings reflect my views, but in comparing notes with both Casey Flaherty and Bill Henderson, I found that our respective, independent picks for standouts matched up fairly well. Apart from these factors, I found these presentations to be worthy of general interest to the extent they shed light on some broader trends and shared challenges I see in the marketplace.

Perkins Coie [Past] / Redesigning Firm-Client Engagement with Pricing Innovation as Linchpin

The identified problems are systemic and all too familiar:

- Purely transactional relationships with outside counsel are frustrating and ultimately costly for in-house departments.

- The mechanics of traditional legal buy fail to scale, often creating process friction and drag in situations where speed is at a premium.

- Administrative procurement tasks (fee negotiation and spend approvals) present a pain point, but also disincentivize the type of deep engagement required for outside counsel to invest time and effort in learning the client’s business.

The proposed solution pulled together multiple components in client service innovations that also sound very familiar.

- Portfolio fee model encompassing an entire tranche of work

- Process and technology tools to (a) eliminate friction during new matter intake using business rules to assign work quickly based on strategic value and complexity profiles and (b) automated feedback collection workflows to reinforce culture of improvement and mutual investment

- Integration of key metrics into hard incentives to drive (not just “encourage”) deeper engagement and more fluid interactions across inside and outside counsel to drive investment in learning Microsoft’s business

What made this noteworthy? If you are reading this and thinking 😴 that you’ve heard all this before, you’d be right. If you’re thinking that these ideas no longer count as innovative because it’s been done, you’d be wrong.

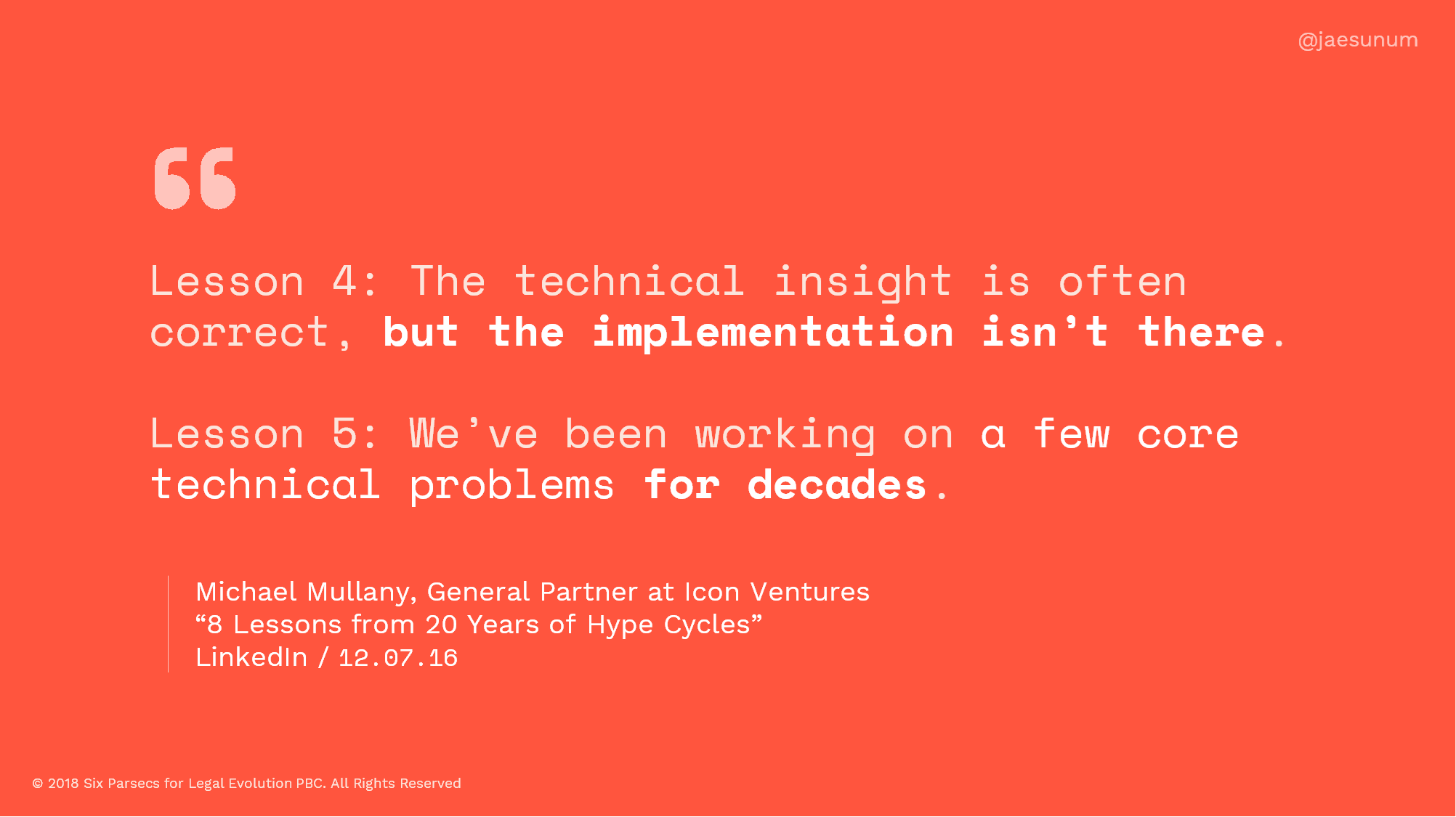

A couple of years ago, Michael Mullany, a General Partner at Icon Ventures, actually went through 20 years of Gartner Hype Cycles to build a holistic picture of how new innovations actually advance through full implementation and adoption. See “8 Lessons from 20 Years of Hype Cycles,” LinkedIn, December 7, 2016. See also Posts 024, 025 and 026 for discussions relating chasm theory to the Hype Cycle.

Mullany’s LinkedIn essay is a great read for anyone who is disillusioned about the level of hype or pace of change in the legal industry. My favorites of his 8 broad themes are these:

Similarly, the legal vertical has been grappling with a few core business problems for a while now. We’ve heard ad nauseum about the pernicious second- and third-order effects of the billable hour (also, intermittent and exaggerated reports of its imminent death continue). We’ve heard, over and over and over again, clients asking firms to better understand their business. The reason that these problems pop up regularly and persistently over the years (like zombies 🧟♂️) is because… well, they’re hard to solve. They are precisely the types of questions that seem galactically obvious in an armchair discussion yet present as wicked problems out in the real world where people work and live: because they’re subject to “incomplete, contradictory and changing requirements,” often with overlaid on top of social complexity and complex interdependencies.

The problems addressed by the Perkins Coie team are the core technical problems of our industry: how might we (a) actually improve the client experience around legal buy and service delivery, and (b) do so in a sustainable manner that rewards service providers for value delivered? It would be a grave error (and the most harmful side effect of the current environment of hype) for would-be innovators and change agents in the legal industry to dismiss these fundamental problems just because we’re, like, 🙄 bored 😴 by them. The Perkins Coie team should earn full marks for tackling head on the old and familiar problems that really, truly matter — a much-needed antidote to the ongoing hunt for the next shiny thing and the new hotness. See Post 066 (arguing that siloed innovation efforts lead to arrested development in legal innovation).

Alternative fee arrangements, in particular, have presented in the legal industry as innovations that sound plausible but often fail during implementation because teams fail to design and deploy a true whole-product solution around the innovative pricing model (key graphic from Post 024 reproduced below). The original model is designed for software products, but the framework applies broadly to other innovations: the challenge is to think through the enabling and adjacent components needed to drive sustained adoption by real people.

The same story applies to new business intake: every major firm in the Am Law 50 has by now been through multiple cycles of improvement projects to cut down turnaround times for new matter opening, and yet clients still experience significant process friction around fee negotiations, conflict checks, spend approvals, and staffing assignments. These problems are difficult in implementation because they take more than top-down controls imposed by enterprise software: they require deep understanding of how actual people perform their work in the context of their everyday lives. See also Post 041 (giving a client-side example of the high bar a whole product solution represents, based on solutions deployed by David Cambria during his time at ADM, in close collaboration with Eric Elfman of Onit).

While it’s far from bleeding edge technology, Perkins Coie’s deployment of business rules and automated workflows is key and demonstrates canny insight on how to drive changes that stick. To use David Cambria’s vernacular, such mechanisms reverse the flow of change management from “top-down controls” to a system of “nudges.” But these solution levers require material up-front investment by both client and firm to articulate the logic behind risk and complexity profiles. Translating those requirements into actual tech tools that work requires deep domain understanding of both organizations’ current operating environment.

Novelty is NOT the key. Ideas (both new and old) are everywhere: execution is everything. Until an idea is tested, built and deployed in a manner that makes a difference to clients (and hopefully to the firm’s P&L), the innovation has no commercial value. And I 💯 believed in the Perkins Coie solution, because the presentation gave every indication of both technical insight and implementation know-how. The holistic nature of the problem statement and the configuration of solution components is what proves out the Perkins Coie team’s innovation maturity: the recognition that the solution has to address both sides of the coin in relieving client pain while fixing both the incentives and the work context for the firm.

Also worth noting here are the profiles of the presenting team from Perkins Coie:

- Chief Practice Management Officer Toby Brown brings years of cross-functional line leadership experience across marketing, business development, practice management, knowledge management, and strategic pricing. Here’s what those functions all have in common: they comprise the core business functions of a law firm that underpin the client experience. There are many across Big Law with experiential depth in 2 or 3 of these areas, but Toby Brown is in a class of his own when it comes to technical understanding of how every part of a law firm operation actually works.

- Chief Information Officer Rick Howell similarly brings diversity of perspectives to bear: intimate familiarity with the law firm finance stack (a core infrastructure barrier to meaningful advances in law firm management and legal buy innovation) and “extracurricular” activities that evince a clear interest in customer-orientation. At least for now, these are atypical traits for a Big Law CIO, a beleagured cohort where many are overwhelmed with the mechanics of managing a patchwork environment in the back-office stack, ensuring that the mission-critical systems (email, DMS) stay on-line and provision of user support to a constituency still debating whether they really need to learn Microsoft Office.

The final reason I found the Perkins Coie solution worth highlighting here is this: there is a wind change coming to the legal vertical, across the buy- and sell-side. To fix the core technical problems of our industry, operational discipline and client-orientation must come together. Successful innovation teams will leverage improved integration of cross-functional business and technical talent into the work required to conceptualize and execute on improvements to service delivery. Toby Brown and Rick Howell represent an instructive example of such a team.

EY [Future] / A Risk-Based Approach to Evaluate Legal Documents for Translation & Localization Services

The identified problem addressed Microsoft’s need to translate thousands of legal documents each year as a function of the company’s global reach. Due to the frequency and aggregate volume of this work, and the fragmented nature of how the business needs would arise, the EY team hypothesized that there would likely be inconsistency in how the company currently determines the need to localize document templates for compliance with jurisdiction-specific requirements.

The proposed solution combined a full stack deployment of Microsoft technology with a risk scoring model that would evaluate documents submitted for translation & localization that would centralize workflow tracking of localization and translation requests. EY’s proposed solution included the MS Azure rules engine and MS AI Engine to integrate new patterns and improve the quality of risk evaluation over time. Although not discussed at length, the solution implied fluid deployment of people resources from EY to respond to fluctuating workload. The presentation also included a mockup reporting panel providing summary analysis of all requests on a quarterly basis.

What made this interesting? This presentation tackles precisely the type of problem that is difficult for incumbent firms to see: high-frequency needs for low-complexity legal work where complications are introduced by factors other than the law. The scope and reach of global operations demands some level of process thinking and attention to traffic control, but the higher-value opportunity that EY identifies here is the legal risks that are created by human and organizational factors. A fairly typical problem in high-volume work is the variation and inconsistency introduced by humans in how they apply standards to each instance. In this case (as in many others), the inconsistent application of expert judgment can in and of itself introduce both legal risk (where localization is needed but not requested) and lead to spend leakage (where localization is requested but likely unnecessary).

Similarly, EY’s proposed solution hinges on elements where the Big Four are advantaged and most incumbent law firms are challenged: the ability to deploy a whole-product solution combining process and staffing levers with technology. But most notably, the Big Four are able to stand up and deploy such solutions (a) with velocity and (b) at scale. While law firms have been experimenting with process and technology in isolated pockets for some years now, the Big Four bring to bear greater discipline in precisely the area Microsoft asked providers to improve: service delivery.

Across various service lines, Big Four projects are led by mid-level managers who are expected to develop core competencies as engagement leaders. Compare that to the training provided in Big Law not to relationship managers in the equity partner class, but to the senior associates and income partners who often take on the role of caserunner on broad swath of legal matters. For the Big Four, operational excellence and client service competencies are woven into the fabric, not applied on top, and that advantage will manifest itself in superior velocity. Their scale advantages flow from relatively superior tech fluency, but also from depth of experience in pulling together cross-functional teams that combine domain expertise with technical and business talent. It’s this combination of competencies and depth of experience that better equips EY to stitch together a suite of tech tools into a solution stack, but also to know where and how to supercharge processes with secondary elements like extraction and robotics process automation.

Sizing and tracking the Big Four threat. In recent weeks, the PwC-Fragomen “alliance” has been covered in a bevy of musings on the looming threat of Big Four encroachment and the countless advantages these new entrants bring to bear. See “Where Else Will the Big Four Pop-up in Legal?” Erin Hichman, Law.com, September 27, 2018. Hichman’s article is a good read and provides a great overview of Big Four capabilities as a general matter. But I question the assumption that encroachment into the legal vertical represents manifest destiny for the accounting firms, or that they’ll be able or strategically motivated to put the full weight of every resource available to disrupt the legal vertical.

In particular, i question the assumption that the current Big Four channels into the Fortune / FTSE 100 C-suite symbolize a material threat to incumbent firms. The Big Four are plugged into the CFO’s office for a reason: their current revenues take them there, and those service lines represent barriers as well as opportunities for the relatively nascent legal arms of the Big Four. Audit represents about a third of Big Four revenues; Deloitte, PwC, EY and KPMG collectively audit all but one of the Fortune 100 companies. Keep in mind, too, that the accounting giants have a spotty track record of managing complexities around auditor independence requirements and very real conflicts of interests across their various business lines. Following the Enron scandal and Sarbanes-Oxley regulations, the Big Four were obliged to execute a flurry of spin-offs of advisory and consulting arms.

Incumbent firms should watch the Big Four threat, and there are many reasons for law firms to bolster capabilities where they are currently challenged in serving large corporates. That said, incumbents law firms would do well to also consider carefully where they are comparatively advantaged and where the Big Four face significant headwinds. Preemptively protecting that ground by developing whole-product solutions may well be as important (and more strategic) than defending the fringes where the Big Four are encroaching now. That’s a segue into our next spotlight.

CMS [Future] / Productizing the Incumbency Advantage in M&A Transactions

The identified problem addressed an opportunity for gain creation rather than relief of a well-known problem: how Microsoft might better position itself in markets outside the US by calibrating deal terms based on superior market-specific intelligence of norms and expectations. This already sets the CMS team apart from the pack — and the identified opportunity evinced deeper understanding of Microsoft’s business strategy as a global strategic acquirer. M&A deals are complex to evaluate and deals that fall through late in the cycle represent not only significant expenditure of time, effort and money from the legal function, but could lead to strategic competitive setbacks in key categories where Microsoft seeks to acquire critical assets like talent, IP or market share. This represents a textbook example of how to integrate legal expertise into idea generation for innovation opportunities: the best pathway for incumbent law firms to widen the moat against new threats, by scaling up the critical assets that underpin their unique comparative advantages.

The proposed solution is a productized solution called DealFlow, which would leverage the firm’s proprietary intelligence and data stores collected over 3,600 deals, capturing over 60,000 deal points in total. Based on the contextual value to Microsoft (as well as other strategic acquirers in the Fortune/FTSE 100), the product opportunity is absolutely worth pursuing for CMS. The data asset, as described by the CMS team, certainly represents latent value: Experienced practitioners would certainly be better positioned than Bloomberg or Mergermarket to identify the deal points that tend to make or break deals. The open question is whether the CMS team can extract and package the intelligence into a usable product and how they would bring such a solution to market in a way that delivers value to both the customer and to the firm.

What made this interesting? The notion of packaging data and content stores (often developed and maintained as internal knowledge management stores) isn’t new. Many firms have explored this path, often with third-party technology partners. See Post 062 (citing various examples of law firm forays into expert systems and productized legal solutions). As noted previously, novelty isn’t the name of the game. The fact that other firms have experimented with product plays that attempt to capture existing KM and data stores should actually be an encouraging fact: good ideas usually occur to multiple market participants and observers. I thought the CMS presentation was well worth highlighting here because it addresses, head on, a pathway to new products and services that many law firms are pondering now. Plus, it is a great example of how legal expertise can be deployed in innovation efforts to tackle high-value client problems that extend beyond the legal function to create measurable value to the business.

Should law firms build products and if yes, how? But success is forged in the crucible of execution, and the CMS team has many milestones to cross before we’ll know whether DealFlow will survive contact with reality. The truth is that the product play (like most good ideas) sounds much easier in concept than in execution, and there are open questions on whether the optimal strategy for law firms is to build, buy or partner here. Building tech-enabled content offerings that can compete in the open marketplace is quite a high bar. As a comparison point, Kira Systems builds software that extracts data points out of contracts, deploying both machine learning models and ex-lawyers to train them. Though Kira wouldn’t be a direct competitor to the DealFlow idea, companies like Kira have a huge head start over law firms in the component technologies that could close the gap much more quickly that we might imagine — not to mention other talent advantages in design, DevOps, and software/solution sales.

Aside from the choices on how to build the product, CMS will face other business decisions around viability (key graphic reproduced below, from Post 066).

Many of those decision points are unique to the current market position of CMS and their competitive strategy going forward: will CMS leverage DealFlow as a key differentiator in driving wallet share with existing M&A clients or growing market share by taking away M&A clients from other prestigious firms in the Europe region? Does it make strategic sense for CMS to DealFlow to market as a standalone offering to create a new revenue stream? That product strategy should support their overall competitive strategy and should inform other downstream decisions around marketing, pricing and sales. I’ll be interested to see where this one goes.

III. The Most Important Questions: Why Do All This? And Why Should Everyone Care?

The Trusted Advisor Forum was a very promising start. It represents the beginning of something big — I sincerely and wholeheartedly place it in the category of “huge, if true.”

The September 20 event is itself an important endeavor, for the following reasons.

- Shared learning matters. I’ve written before that duplicated efforts by many innovation teams in separate organizations create systemic drag on the pace of market-wide progress. Such teams tend to be leanly staffed and under-resourced, often working without the full complement of diverse competencies across technology and business to make material headway. Forums like this are important so that we advance our collective thinking by learning from the trial-and-error of others, not just our own.

- A habit of collaborative dialogue at close proximity. It’s a famous proverb that makes intermittent appearances at political conventions, but it’s famous because it rings true: “If you want to go fast, go alone. If you want to go far, go together.” The Microsoft team is playing the long game. They intend to go far with their partners rather than move fast alone. Building real bonds of partnership requires many forms of engagement, and they recognize that some face-to-face togetherness at regular intervals is a must for collaborative work of high complexity in a relationship-based business. This is meaningful particularly because Barnwell is refreshingly candid about the investment of time, energy and effort such events require — from his own team as well as from the invited providers. Even with that recognition, he’s asking — and on September 20, at least, lot of people showed up.

- Building resilience together through candor. The aim is to get better together. Getting better requires continuous cycles of honest, constructive feedback. Both giving and receiving such feedback are skill sets that require practice. Microsoft is putting itself — and its primary service providers — through the necessary reps, and they’re taking steps to prove their commitment in public.

These reasons are important. I am optimistic that the Trusted Advisor Forum, over time, will bear fruit in all 3 areas — but my optimism is based on the much broader and brilliant design of Microsoft’s overall strategy for legal buy and provider engagement.

Strategy First, Innovation Second

The Trusted Advisor Forum, as well-designed and executed as it was, is a fit-for-purpose component in a much bigger picture: it is specifically intended to create incentives for a specific set of behaviors that Microsoft seeks from specific firms. To understand why this experiment is truly noteworthy, we need to look under the surface to the strategic thinking that is driving Microsoft’s experimentation.

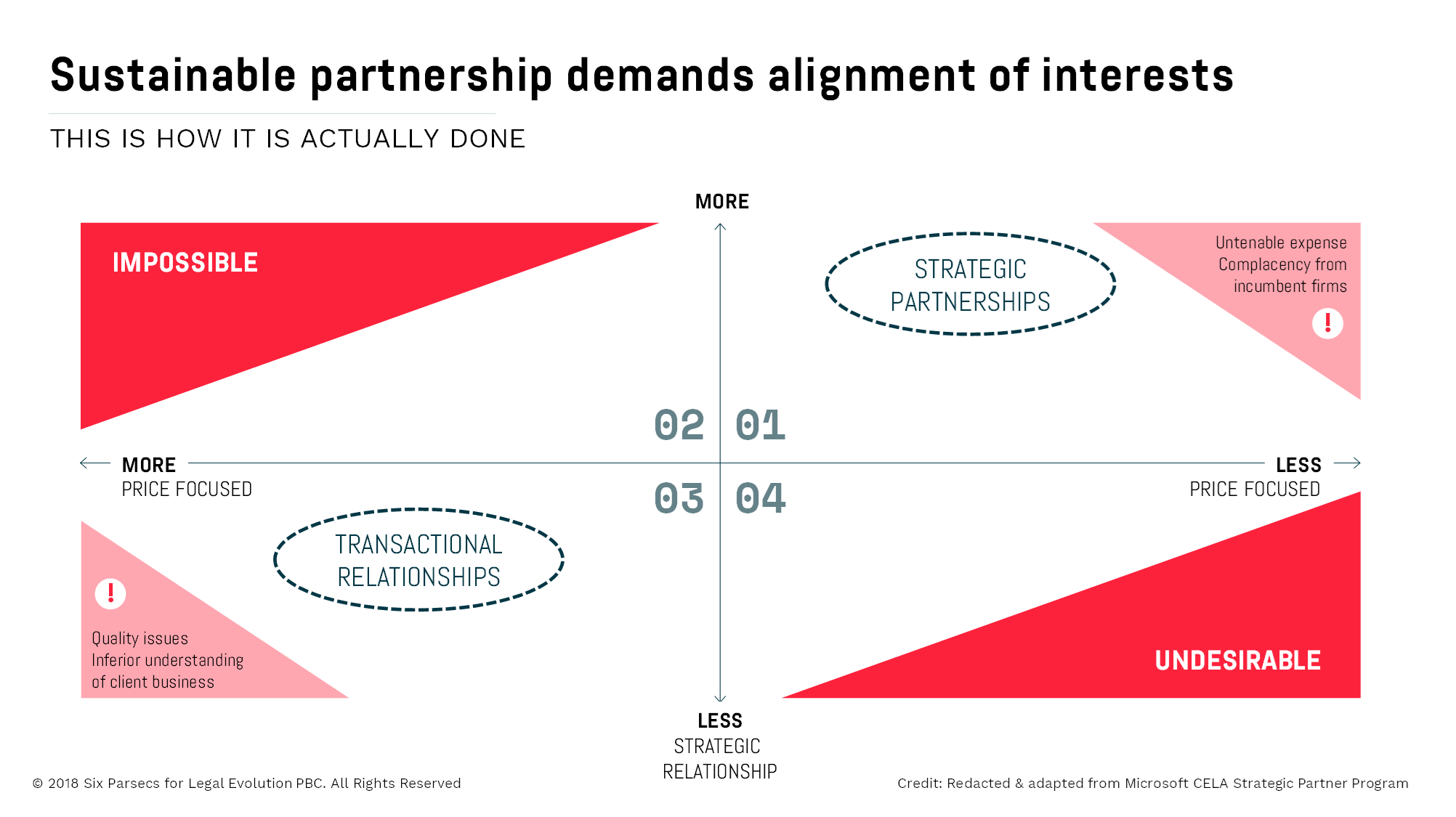

The vast majority of participants in the Trusted Advisor Forum are part of Microsoft’s Strategic Partner Program (SPP). A new iteration of its precursor Preferred Provider Program, the SPP has several unique features worthy of note. The graphic below helps illustrate the salient points. It’s adapted from Microsoft’s internal materials laying out their forward-looking strategy for legal procurement and provider engagement. It has been lightly redacted to remove sensitivities, but Microsoft is openly sharing its strategic thinking with the market. (Of course, there’s a reason for that. Stick with me for a few more minutes.)

Currently, the Microsoft legal function sees itself playing somewhere near the center of this 2×2: they’re not particularly price-focused relative to comparable buyers of legal services and they believe they have upside opportunity to create far more strategic collaboration with outside providers. The future-state they envision, though, is what I would call a bifurcation strategy to the design and management of their legal supply chain: strategic partners will move upward and to the right squarely into Quadrant I, and transactional relationships will shift downward and to the left into Quadrant III.

In my analysis, the bifurcation strategy is important because it represents precisely the shift in thinking we need from the buyers of legal services:

- Real commitment and pragmatic approach to partnering with outside counsel

- Sustained focus on a holistic buying strategy deployed across the relationship lifecycle

- Clear alignment of investments and incentives across the entire legal supply chain

Co-Prosperity: Partnership Should Be More Than a Byword

In the early years following the Great Reset, corporate legal functions correctly perceived a repricing opportunity. The enormous pressure on inside counsel to drive cost containment was one driver, but there is also a distinct sense that over the preceding decades, the “artisan guild” had also functioned as a price-fixing cartel. The resulting price pressure on outside counsel is neatly summarized in this annually updated chart from the Thomson Reuters-Georgetown Report on the State of the Legal Market:

In addition to steep discounts, corporate buyers of legal services took other steps to structurally improve their negotiating position. For instance, the insourcing trend worked to create viable alternatives to law firms. See Post 003 (data showing that in-house departments have grown more than 7x faster than law firms since the late 1990s). Over time, other alternatives emerged, and law departments experimented with then embraced new types of legal service providers. See Casey Flaherty and Jae Um, “ALSPs: Already Here & Looking Upmarket,” Law.com, September 20, 2018.

As a result, law firms have been operating in an environment of both immediate and remote existential threats. Meanwhile, the public discourse around disruption in the legal market seems to me more adversarial rather than collaborative. The head-shaking, finger-wagging and eye-rolling about the obliviousness and arrogance of outside counsel are fairly constant. Of course, it is the client’s prerogative to opine that outside counsel rates are too high, Class A office space is unnecessary, associate compensation is too high, and law firms headed for extinction — but these messages signal to firms that many clients are not at all interested in the continued viability — let alone prosperity — of law firms.

Against that backdrop, many clients claim to want deeper engagement and greater investment. After all, the vocal minority doesn’t speak for the entire constituency. Law firms vigorously agree that they want that too. I think I believe them, but I’m not sure the industry has been realistic about what this will require from both inside and outside counsel. Convergence initiatives and preferred panel programs have been held out as a promising pathway toward this promised land of engagement, collaboration and all the other warm and fuzzy words: these have now been through multiple cycles in the past decade, and the word on the street is that they… don’t really work. See Firoz Dattu and Aaron Kotok, “Law Firm Panels, Part I: Are They Designed to Fail?” The American Lawyer, June 26, 2018.

The repricing effort has taken its toll on the financials of the Am Law 200; that is the nature of a buyer’s market. However, by 2018, I think we are seeing many undesired second-order effects of the Great Reset across the entire ecosystem:

- In some cases, procurement tactics applied haphazardly to legal buy has created more complication, not less, to outside counsel selection and engagement.

- Many law departments are challenged to keep up with a broader brief and some are straining under the weight of accumulating change initiatives: driving improvements to law department operations that are growing more complex, allocating work across a more diverse supply chain, and the never-ending exploration of new technologies and capabilities.

- Most law firms are running leaner than ever on administrative staff, and in some cases this leaves these players poorly positioned financially and politically to invest in infrastructure improvements or client-facing innovations.

(By the way, it is true equity partners can choose to “invest in the future” instead of clocking a higher PPP ranking for the firm and banking a bigger distribution check each year. Some firms have actually done that. Perhaps all of them should. But as Casey Flaherty often remarks, the legal market is not a morality play. It is difficult to expect most people to take risks in trading in certain profits today for uncertain returns sometime in the distant future, particularly on abstract schemes they only vaguely understand.)

I think the Microsoft strategy deserves attention because their thinking cuts to the heart of the issue: we need to engage in more realistic thinking about aligning commercial interests across the buy- and sell-side. The reality is that clients have pressured firms from right to left on the pricing axis, and for various reasons many relationships moved downward along vertical axis to become less strategic.

The results-oriented approach is to ask what can be done about it, and this is Microsoft’s hypothesis. Note the huge swath of Quadrant II that is blocked off (“IMPOSSIBLE”) in addition to the corresponding edge in Quadrant IV (“UNDESIRABLE”), here and in the original framework from Microsoft’s materials.

In essence, the Microsoft team acknowledges, publicly and candidly, that it is not tenable to expect any of their service providers to invest in a strategic partnership under maximal pricing pressure. This is one of those insights that seems obvious when stated, but something many in-house departments have failed to integrate into their buying behavior when they ask vaguely for (and fail to reward) “better” or “faster” but focus more on “cheaper.” It requires a healthy dose of pragmatism, commercial empathy, and clarity of thought to recognize that law firms will not subsume their financial interests under the guise of “partnership,” just as clients will decline to reward transactional relationships with premium pricing.

The next step is how Microsoft translates that clarity of thought into consistent execution.

Insight → Strategy → Action: What Makes Microsoft Different

The bifurcation strategy creates greater clarity around incentives, and Barnwell is candid and open about both Microsoft’s intentions and the downstream implications for firms. Here’s a direct quote from Barnwell (again from our looong podcast episode):

The presumption that we hire one firm to do all our work is just not realistic. What we do is we partner with many firms, and we try to pick the things that they do really well. And we try to monopolize that as much as we can. So the idea that there is one major platform firm that we go to and we want them for one stop shopping is not practical. I see the future as having more unbundling, not more bundling. I suspect we’re going to see more specialization that results in more success and excellence that’s going to concentrate our buying patterns with the firms that have specific expertise on the things that we need. And what we will do is ask them to partner [with us and with our other firms].

In essence, Barnwell is laying out his worldview and buying philosophy pretty clearly here: Microsoft is on a path toward spend consolidation in categories that matter most to their business and pursuing something akin to a best-of-breed procurement strategy in those categories. For the firms that will ultimately win out a stable slot in the Strategic Partner roster, this will translate to the triple crown in law firm account strategy: (a) in-category wallet share growth (b) in premium rate practices, with (c) fairly solid revenue security for the long run.

That is the prize at stake and the incentive structure that supports the Trusted Advisor Forum. And Barnwell is equally clear-sighted and candid about what it will take to win that prize:

[Firms] say they want to be on our panel. We ask for all kinds of things. Amicus briefs, relationship support, diversity engagement, and the list goes on. I see semi-informed behaviors around these asks that tell me… firms asking do not know what they are signing up for.

This recognition of what partnership costs is important, from both buyer and seller of legal services. As demonstrated in the Perkins Coie presentation, implementing deeper engagement in a strategic partnership takes time and effort and energy. Time and effort and energy are finite resources for any going concern, and so they must be allocated with discipline and all ROI accounted for. If what we want to see is systemic, sustained innovation in the legal vertical, we need to advance our collective thinking on how incumbent firms can pursue innovations that are commercially viable. See Posts 062 (legal innovation must include law firms) and 066 (viability as one of 3 key axes for de-risked innovation).

One frustrating behavior I see in the legal market is this: all of us instinctively understand that we can’t be best friends with all our friends. We love our best friends best, and we also invest more time and energy into them relative to all our other friends. Hopefully the investment is mutual, and when it is, BFF-ship is more rewarding than standard friendship. For example, I recently flew toward a Category 5 hurricane warning while nursing a cold to be in my best friend Jennifer’s destination wedding in Hawaii. I have many other friends for whom I care dearly, but I probably wouldn’t have done the same for anybody else. All of that may have been obvious and instinctual to all of us in grade school, and yet I continue to see too many law departments and law firms slap the tax that comes with BFF-ship on far too many relationships that don’t offer BFF-level benefits. And just as pretend-BFF-ship demands social and emotional costs, pretend-partnerships lead to unwarranted costs for everyone involved.

Microsoft’s bifurcation strategy systemizes the core insight. The company is building one system of engagement for its strategic partners and a different system for everyone else. Microsoft expects to buy, consume and measure services differently with its Strategic Partners relative to other providers in its supply chain. Strategic partners will contend with different expectations for investment; the brilliance of the strategy is that the incentives for Strategic Partners need not be wholly extrinsic. Sustained focus on execution toward deeper engagement are more likely to create opportunities for intrinsic profit opportunity for the firms with the pricing, process and service design capabilities to chase them. Again, see the Perkins Coie example above. See also Post 063 (law firm innovation efforts must at some point encompass legal buy innovations).

Events like the Trusted Advisor Forum are but one example of how the strategy will be deployed across the entire relationship cycle, structurally and intentionally. Barnwell is an engineer by training, a voracious reader, and an inveterate tinkerer (so I can’t think of anyone better suited to put the Flaherty playbook to the test). Barnwell’s also got an All-Star team behind him (including a data science team! 🤩💖 Yay for data!) and top-down executive support from his leadership. All this bodes well for the Microsoft experiment: an atypical combination of factors in an industry that is generally unfavorable to innovation. See Post 051 (legal innovation as extreme sport).

The Choice Before Law Firms: Markets of One vs. Markets of Many

Microsoft is ranked 30th in the Fortune 500 list. In 2017, they reported nearly $90 billion in revenue. Thus, they buy legal services at fairly decent scale. To give a sense of sheer size, this means Microsoft’s revenues match up with the collective revenues of the Am Law 100 ($91.4 billion in 2017). In essence, Microsoft has the clout and the legal spend wallet to make unusual requests of their firms and to kick off a new wave of thinking– but even this buying power can’t sustain an entire market shift on its own.

At that point, the question becomes whether other law departments will follow Microsoft’s lead. if Microsoft and Barnwell can evangelize their way of thinking to a critical mass of Fortune 100 law departments, this could signal a material shift in legal buy. If the Microsoft system catches on further, the implications for the legal market could indeed be huge.

Law firms are already challenged to compete in an environment of flat demand and ongoing volatility. The graphic below summarizes my thoughts on what separates the best performing firms from the pack. These are simple concepts that are difficult for most firms to execute and often require a multi-year runway. If Microsoft’s ideas catch on, that runway could get a lot shorter.

In particular, law firms everywhere should think seriously about how they invest in innovation and how that innovation agenda fits into their competitive strategy.

One key question raised by Microsoft’s bifurcation strategy is this: law firms should be asking whether they have sufficient focus in their practice mix and in which areas they are really equipped to compete for a best-of-breed spot. This is a critical question in a market where many firms have been pursuing broad-based expansion of geographic and practice coverage.

Platform firms should also pay attention to how they allocate innovation investments across markets-of-one (e.g. highly customized client service and account-level investments for premium rates) or markets of many (e.g. at-scale platform enhancements and time/labor displacement plays to compete on margin). Earlier reporting on the Trusted Advisor Forum quoted Barnwell saying it is not practical for Microsoft to be the only client that is asking; some have taken this to mean that law firms will invest nothing into innovation unless asked. Again, that may be true of some firms, but I have a different read on why other clients need to ask. For those firms better positioned to pursue market-of-many innovations, clients who share similar needs and desires must at some point coalesce into large-enough segments where their preferred innovations (and those that perform at a superior level) can scale into viable market solutions.

Meanwhile, mid-size and downmarket firms (and yes, new entrants like the Big Four and ALSPs) may have an opportunity to leapfrog the competition if they can just place the right bets.

These are all reasons for the market at large to take note of the Microsoft experiment.

IV. Deliberate Doing, Based on Very Smart Thinking

“Less talking, more doing” — this is the mantra du jour on Law Twitter. I understand the frustrations that lie beneath, but I submit what may be a minority report.

Talking without doing is indeed bad. But doing without thinking isn’t much better. Often, academics and consultants are guilty of a lot of talking without enough doing, but practitioners are at perpetual risk of a lot of doing without enough thinking. When we stop talking, our collective thinking gets dumber, not smarter — no matter how many mental, emotional and physical calories we burn in our own silos, our collective pace of learning gets slower, not faster. And we need smart thinking to tackle some of the thorny and complex inefficiencies in the legal market. To accelerate positive change, we still need communication channels to learn from the trials and mistakes of others, not just our own.

Microsoft is doing something unusual here: sustained and intentional action underpinned by very rigorous thinking. And the entire team at Microsoft is brave enough to do this with as much transparency and candor as practically possible. This alone is worthy of one last round of 👏👏👏 applause 👏👏👏 — from everyone who is really invested in positive change in the legal market.

In the long run, I’ll bet my money every time on teams that think long and do deliberately.

(If you have made it all the way to the end, you have my sincere gratitude. 🙏 Please know I really and truly appreciate the time and attention you invest in reading.)

What’s new? See I am a LegalZoom customer (070)