2018 has been a watershed year for capital flow into legal markets. Will it be enough, at last, to push legal innovation forward?

It’s an age-old saying: money can’t buy everything. The most common examples include happiness and love. It’s time to add “legal innovation” to this lofty list.

In the past few years, we have seen unprecedented levels of capital flow into the legal space. The partial views of funding activity we see from various sources imply an already high level of energy as well as money invested into legal innovation. Further, those investments (and one would presume, attendant efforts) only appear to be increasing:

And yet the market appears awash in disillusionment. Many established thought leaders and influencers remain skeptical about the actual impact (or lack thereof) of these developments. Pinpoint signals from corporate buyers indicate a glacial pace and highly uneven distribution for meaningful improvements in service experience and value delivered. And the PeopleLaw sector remains woefully underserved, even as legions of practitioners outside the strongholds of Big Law struggle financially. See, e.g., Post 037 (presenting data).

So what gives?

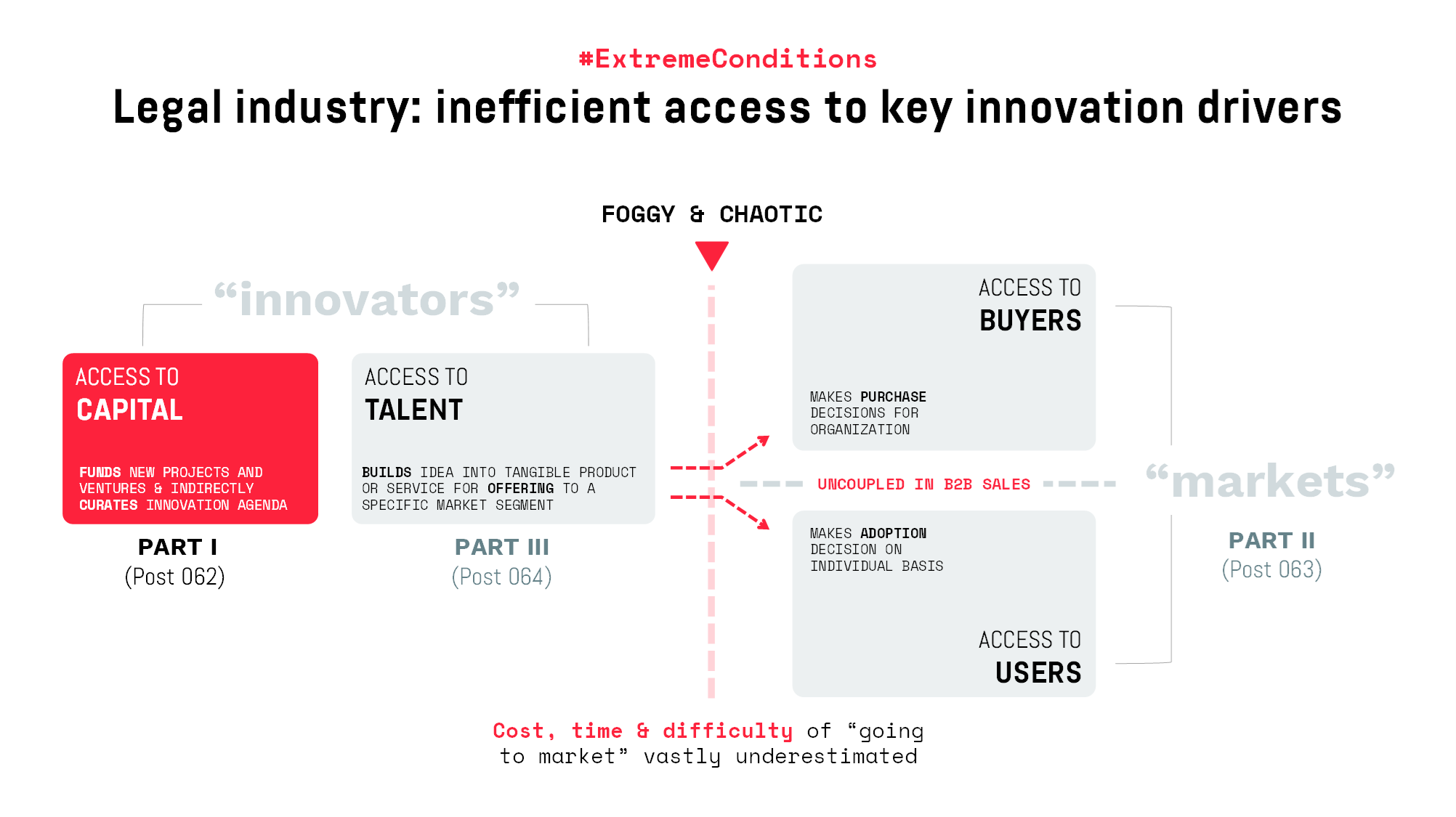

A Roadmap to Innovation Woes: Key Innovation Drivers

In my first post on Legal Evolution, I addressed a few of the structural attributes that make legal a particularly unfavorable ecosystem for innovation. See Post 051 (legal innovation as an extreme sport). That discussion zoomed out for a broader view at the makeup and composition of legal service providers.

Now it’s time to zoom in. This is Part I of a three-part series about systemic barriers to innovation maturity in legal markets. In this series, I’ll pose a new set of hypotheses about the current state of our industry — to explore whether would-be innovators and visionaries have sufficient access to the ingredients that are necessary to make innovation actually happen.

The above graphic lays out the roadmap, along with a brief description of the critical function of each component.

- Part I (062) provides an overview of recent trends in capital investment into legal innovation. While several valuable directories, listings and analyses have already covered this topic from many different angles, the aim of this post is to explore why we are seemingly stuck in the “early days” of legal innovation despite an overarching trend toward expanded access to capital.

- Part II (063) probes a critical problem facing all new offerings in every permutation of legal innovation: the difficulty of identifying and understanding the customer. Part II summarizes the various customer roles in B2B service environments and the common reasons that new offerings fail to achieve problem-solution and product-market fit.

- Part III (066) addresses the people side of the equation for teams and businesses trying to drive change to the status quo in legal markets. Whether the goal is (a) to drive incremental improvements to existing offerings or (b) to develop and bring to market a wholly new service or business model, legal evolution is a team sport that demands differing configurations of specialized skill sets. Part III will summarize the necessary competencies and capabilities, with the goal of evaluating whether it is feasible for most legal businesses – whether incumbent or new entrant – to assemble a winning team.

Posts 062 – 064 are not intended to pose an exhaustive, definitive, or controlling theory of legal innovation. Instead, the goal is to provide a useful framework, by endeavoring to draw attention and focus to factors that can be influenced and changed, once examined and understood, by economic actors in the marketplace. As a counterpoint, I have previously criticized narratives that hinge on personality traits of lawyers, in large part because it is not a tenable proposition to ask a group of millions of adults to change stable aspects of their disposition. See Post 051 (“because lawyers … ” riff).

Here, the hope is to better equip innovators and change agents who find this analysis compelling and to enable them to perform more structured evaluations and make more rigorous decisions. For everyone else, this series invites constructive dialogue.

Regulatory Constraints Affect Capital Flow (in Obvious & Non-Obvious Ways)

Like many other features of the legal industry, the flow of capital investment in this space is littered with idiosyncrasies. The regulatory barriers to non-lawyer ownership has been debated ad nauseum elsewhere by wiser and more knowledgeable minds, but it bears one more mention here. The blindingly obvious implication is that this severely limits the pool of available sources for equity capital into businesses that practice law.

The current regulatory scheme has three less obvious implications on legal innovation as well as the mechanics of how innovation efforts are funded and governed:

1. The Role of Incumbents (Yes, That Means Law Firms and Lawyers)

It secures for incumbents (law firms owned and largely operated by lawyers) a material role in deciding when, where, what and how the entire industry will change. This, of course, is a feature, not a bug: protectionism is intended to establish clear and insurmountable advantages for the artisan guild.

It is true that law firms have resisted change and thus bear full responsibility for the current state of the industry. The fact remains, however, that incumbents must be included in any serious dialogue about legal innovation. Regardless of their performance to date, law firms are both financial sponsors of, and direct participants in, legal innovation.

2. Practice vs. Business of Law

The requirement of lawyer ownership calcifies unhelpful divisions between the “practice of law” (the domain of lawyers, with limited access to capital) and the “business of law” (a set of enabling activities for legal practice, in the domain of… everyone else with varying non-lawyer titles). These divisions extend deep into our collective consciousness and they do serious harm not only to workplace cultures but also the rigor and clarity of our thinking about legal innovation.

This distinction creates an artificially binary model that fails to accurately represent the reality of how legal teams serve clients in the real world. Ultimately, this type of thinking favors incremental improvements to the status quo and R&D based on misguided and antiquated assumptions. It’s akin to exploring a closet with the lights off.

3. Follow the Money

The requirement of lawyer ownership also diverts a great deal of available capital into non-core segments of legal services. This has a dramatic effect on the experience of the end-users and shapes their expectations and appetites. This is, at least in part, why “legal tech” receives a disproportionate share of both capital and attention in the legal innovation dialogue: A lot of money is going into a disproportionately small part of the value chain.

The aforementioned wiser and more knowledgeable minds continue to discuss the desirability and feasibility of changing the regulatory moat around lawyer ownership. In the meantime, this discussion will remain premised on the status quo, in the spirit of focusing on factors that can be influenced by individual market actors.

Who Funds Innovation & Why?

Due to the idiosyncrasies of the legal markets, it is helpful to think about innovation in two simple categories: the typical/conventional financial sponsor vs. atypical sponsors unique to the legal innovation ecosystem.

Traditional Sponsors: PE Firms Are All About That Multiple 💰❌💰

The archetype for the traditional financial sponsor of a new venture is the private equity firm. PE firms (inclusive of angels and venture capital shops) are themselves commercial enterprises. Essentially, they offer specialized expertise in the strategic deployment of capital for wealth creation. To put it as simply as possible, PE firms invest capital to buy part or full ownership of companies, apply their expertise to make those companies more valuable, and then sell those companies (hopefully at a higher price point than at purchase).

PE firms attract capital from investors (typically institutional or ultra-high net worth) with investment theses that communicate a unique viewpoint about market opportunities; they retain investors through sustained performance in generating high returns. The below chart is an extremely simplified and theoretical comparison of PE returns against the S&P 500. See “Does Private Equity Really Beat the Stock Market?,” Wall Street Journal, Feb. 13, 2018. There are many caveats about the difficulties inherent in comparing apples to oranges but suffice to say that the ROI expectations are high.

Of course, the ultimate returns to investors are abstractions in that they aggregate the outcome of the PE firm’s many activities, both successes and failures alike. To put this into more concrete context, it is helpful to think about private equity investments at the company level (again, a simplified, theoretical exercise).

- Holding times. On average, PE firms hold portfolio companies for about 6.5 years, although early-stage venture capital investments will have longer holding periods (sometimes much longer).

- Returns/exit multiples. Target multiples are more difficult to generalize than holding times. Venture capitalist Fred Wilson of Union Squares Ventures is famous for saying often that he looks for one investment that “will return the whole fund.” This is a different way of indicating that VCs usually make many high-risk investments with the expectation that most will fail, with a few wins that will make the losses look minuscule. Still, it’s probably a safe and meaningful rule of thumb to say early stage VCs will seek something in the neighborhood of 10x returns while mid-stage investors will be looking for a 3x to 5x range.

Funding innovation is both a means to effectuate and a happy byproduct of the PE firm’s raison d’être: generating returns for investors. As we will see, things are not so simple in legal markets.

Simply put, most legal startups require a long bake for a relatively small pie. In addition, the vast majority of legal startups are point solutions targeting niche markets that are far too small to ever reach the size & scale needed to attract traditional venture capital interest — at least in part due to the highly fragmented composition of the legal services market, as well as the added layer of geographic silos imposed by jurisdictional differences, see Post 051 (legal markets are especially balkanized and opaque).

Big Law Both Funds AND Manages Innovation (And It Sometimes Works 😲)

The innovation theater that often happens (inadvertently or otherwise) across the law firm landscape is more analogous to the recent explosion in corporate innovation. With technology driving a faster pace of change and startups eating into every major sector, mature businesses of all shapes and sizes have embraced the mantra: “what got you here won’t get you there.” This has fueled mystique around the “intrapreneur”, a rash of innovation “labs” housed within staid and stable companies, and the rush to co-opt startup-style innovation and strategy tools, all with mixed results. (Enjoy a moment of relief and schadenfreude: innovation theater was not created by the legal industry.)

As always, there are lessons to be gained from the mistakes of others, even those outside our own domain. Drawing from the hard-earned lessons of corporate innovation programs outside of legal, two reliable litmus tests emerge to gauge the innovation maturity of established firms:

- Why? Clearly articulated strategic objectives for innovation investments, tied to financial KPIs that measure the impact on the core business or progress toward profitable exit

- How? Process and governance around build, buy or partner decisions

A few bright spots exist

Yes, many law firms engage in some level of innovation pantomime for hype and awards, simply to keep up with the Joneses. (Award submissions in 2018 that tout a successful migration from Office 2007 to Office 365 would fall into this category.) And other law firms often get in over their heads in innovation endeavors that are beyond their core capabilities (more on this in Post 064).

But a few law firms do think and act with the recognition that they are future-proofing their businesses against emerging threats. Allen & Overy is a good example of an outlier firm displaying both indicators of innovation maturity. In 2016, A&O partnered with Deloitte to bring to market MarginMatrix, an “IT solution for compliance with the mandatory variation margin rules that now apply to the USD500 trillion OTC [over-the-counter] derivatives market,” now deployed for 8 global investment banks with over 20,000 negotiations completed. See Allen & Overy Annual Results Factsheet for Fiscal Year 2017.

MarginMatrix shows interesting signs of innovation maturity in that it is hyper-focused in product design and target market. The solution design also displays a high degree of customer-orientation, around which coalesces (a) complementary technology components (expert system, workflow, document automation) and (b) a managed services play that leverages (presumably) lower-cost staffing from Deloitte’s deep bench.

Most importantly, however, MarginMatrix makes strategic sense for A&O. OTC derivatives are important to global investment banks (a key market segment for the firm) because the customization flexibility of off-exchange products provides banks with highly sophisticated means to hedge risk. A&O also has comparative advantage to produce and maintain the high-value content that drives MarginMatrix: the legal analysis of multi-jurisdictional regulatory requirements imposed on OTC derivatives.

In the below visualization of potential strategic objectives for innovation investments, MarginMatrix fits comfortably into the “add new offerings box,” which enables the firm to anchor existing key accounts with a tranche of work offering relative revenue predictability.

The notion of packaging expert knowledge into a productized subscription model is not a new idea. Many firms continue to flirt with this idea, and mapping some of those efforts to the above strategy matrix gives some sense of the variation in motivating drivers for innovation investments.

- Littler invested heavily in new offerings spinning up a myriad of branded solutions and toolkits (e.g. LittlerGPS, among others) indicating greater focus on grabbing downmarket share with productized solutions. In 2015, Littler also entered a joint venture with Neota Logic to launch ComplianceHR, which layers Neota’s expert systems technology onto the firm’s knowledge stores into an enablement product mapped to specific and high-volume HR and employee relations workflows. See Press Release.

- Cadwalder Cabinet has evolved into a slightly different strategic play: extending its existing product into a new market segment. See “Regulators Become Cadwalader Clients as Tech Investment Begins to Pay Off,” The American Lawyer, June 18, 2018.

- Reed Smith recently launched GravityStack, a spin-off subsidiary group that will design, test and license technology solutions to legal clients. See “Reed Smith Enters the Legal Technology Market With GravityStack Subsidiary,” LegalTechNews, April 24, 2018.

Apart from these examples, countless firms are now engaged in serious efforts to integrate process, technology and legal operations to both manage costs and improve service delivery. But a sustained product/solutions focus to spin up new offerings to the market remains more the exception than the rule.

The wide variety of motivations for incumbents to invest in innovation explain, at least in part, why it is difficult to generalize about legal innovation. Some of the variation can be explained by the extreme fragmentation of the marketplace and the resulting dispersion in market position and thus strategic opportunities available to each player. The fact remains, however, that rigorous attempts to measure and compare innovation investments, maturity or performance will need to consider these differences.

Capital for Legal Innovation: Current State & Emerging Trends

A survey of the current market landscape as well as recent developments/dialogue suggests there are four key trends to watch in the next 3-5 year timeframe.

- Liquidity events suggest sorting/matching behavior by market participants

- Platform + bolt-on strategy by serial acquirers and mature scale-ups

- Smart money eyeing legal, to the tune of $500m+

- Capital gets creative: working around the regulatory moat

1. Liquidity Events: Not Necessarily a Silicon Valley-Style Bonanza

2018 has already seen a number of deals that have raised many questions (and inspired many hot takes). The below graphic picks out a small selection of headliners. Given that financial terms are rarely disclosed, the LegalZoom secondary investment attracted a lot of attention by virtue of deal size and resulting valuation. See, e.g., “LegalZoom Gains $2B Evaluation in Funding Round,” Bloomberg, July 31, 2018.

Liquidity events have a generally pleasing air of a positive development; some of that may be due to the glorified stories of founder exits vaguely reminiscent of the trailer for “The Social Network.” Certainly, liquidity events usually involve some people coming into a large lump sum of money. Without raining on anyone’s parade, it bears mentioning that the overall texture of recent liquidity events in legal markets indicates that a few different forces may be in play:

- The Avvo, BAL and Riverview Law deals give indications of a strategic sorting in which major players with strategic goals acquire specific assets; in contrast, the Lawyers On Demand and LegalZoom deals feel more like capital churn/injections that will lengthen the runway for these companies to prove out an independent scale/growth strategy that may still be in the works while providing liquidity back to the early stage investors.

- Traditional PE exit strategies favor strategic acquirers and IPOs over financial sponsors, who tend to be more sophisticated and able to negotiate a lower purchase price. Those dynamics may or may not hold in legal markets; the available data is too scant to speculate.

- The exits by BCLP and DLA Piper raise an interesting question about the optimal role of most law firms in the midwifery and nurturing of new ventures. For reasons we will cover in upcoming installments, law firms have unique assets that make it a fertile environment for experimentation and testing — whether they are well positioned to hold their equity positions to a late exit remains to be seen.

2. Platform + Bolt-On: Next-Level Serial Sorting

The activities of serial acquirers and emerging platforms deserves some mention.

- Unsurprisingly, Thomson Reuters and LexisNexis remain most active acquirers as they supplement internal innovation agendas with strategic M&A. LexisNexis, in particular, has been aggressive in sourcing new product & service innovations through recent acquisitions of Ravel Law, Intelligize, and Lex Machina — all prominently on display at the recent AALL conference. in contrast, Thomson Reuters’ recent launch of WestLaw Edge appears to be powered much more heavily by internal innovation and R&D.

- Epiq, Consilio, and Mitratech are all PE-backed and have access to the capital to continue bolt-on deals to round out their market offerings. Most recently, Mitratech acquired ThinkSmart for an undisclosed sum.

- Relativity may emerge as a likely platform looking for bolt-on acquisitions: the company has invested in Heretik and HealthJoy, signaling financial commitment to extend its platform beyond eDiscovery into contracts and highly regulated data stores.

- Earlier this year, Elevate announced that it had secured a line of credit from Morgan Stanley Expansion Capital to fund its growth. See Press Release. Elevate did disclose that the proceeds would be spread out across strategic acquisitions as well as investments in product and service expansions.

3. “Smart Money” from Silicon Valley Continues to Eye Legal Vertical

Independent research conducted by Six Parsecs indicates that “Smart Money” VCs (the Silicon Valley elite, as identified by CB Insights) have invested in almost 30 legal tech companies in funding rounds totaling over $500m. This list includes some of the most recognizable names in legal tech, including Avvo, Clio, DocuSign, LegalZoom, and Ravel, as well as some newer names to watch like Atrium LTS, Casetext, Ironclad, Judicata, Modria, and SimpleLegal. Famed Valley seed accelerators Y Combinator and 500 Startups have been fairly active as well, funding over 20 startups in rounds totaling almost $180m.

An interesting counterpoint to the “Smart Money” portfolio are the investments made by Ulu Ventures. While Ulu’s legal startup portfolio is small, it includes Lex Machina and Ravel Law, both acquired by LexisNexis. Ulu founder Clint Korver was part of an early cohort of VCs who were early adopters and customers of legal startups as an alternative to incumbent firms (and expressed intense skepticism about the waves of change washing over Big Law); that cohort included Foundry Group founder and ex-Cooley lawyer Jason Mendelson, whose claim to fame included, among other things, hating on startup lawyers. See “These Venture Capitalists Skip Law Firms for Legal Services Startups,” ABA Journal, May 2014. This raises some interesting questions about what legal startups might need more: capital to fund growth or advisors with a keen understanding of the domain.

4. Capital Gets Creative: Workarounds for Regulatory Barrier

While only orthogonal to this discussion, the emergence and growth of litigation finance must be noted. Litigation finance is a rare bird in legal innovation that fits into Marc Andreessen’s “huge, if true” paradigm. According to BTI Consulting, litigation made up nearly 30% of the demand for all outside counsel services in 2018; while a rough proxy, the share of litigation spend in all outside counsel budget still gives an idea of the significant addressable market size for litigation finance. See BTI Practice Outlook 2018 (forecasting market size by practice). Since 2014, litigation funders have raised capital in excess of $3bn. See “Litigation Funders Face Their Hardest Sell: Big Law,” The American Lawyer, June 28, 2018. While still in its early days, litigation finance has the potential to reshape the current landscape for a huge segment of the legal services market, and represents a creative channel for outside capital to influence and ramp up investment into legal data handling and predictive analytics.

Access to Capital: Could Be Better, but Not the Choke Point

Research by Six Parsecs suggests that the total amount of hard capital invested into legal tech, legal services and adjacent spaces is in all likelihood much, much larger than the $998m estimate reported by CB Insights in 2017. Further, is impossible to account for all of the soft investments made by existing players to fund strategic projects, initiatives, feasibility tests, as well as the ongoing payroll of the growing roster of internal innovation teams across the legal space.

The aggregate amount of capital invested in legal isn’t the issue — the more serious problem is the inefficiency in finding and funding the right opportunities. However, emerging trends suggest that access to capital is getting and will get more efficient over time.

Upcoming installments will make the case that inefficient access to markets and talent are much more serious barriers to innovation maturity in legal markets. That said, a rigorous look at capital flows in our industry is still important.

Why? Because there is no better accelerant for #realtalk than the topic of money. Discussion of capital must necessarily address the question of returns. Too often, we across the legal industry use innovation as an emotional lift: workshops and brainstorming sessions usually make us feel better and more hopeful about the future. Where accountability mechanisms are absent, good feelings often provide sufficient returns for these costs.

To culturally co-opt an obnoxious catchphrase of one Ben Shapiro, “money doesn’t care about your feelings.” Looking at the current state of the legal innovation landscape through this unforgiving lens can produce unexpected clarity. For the industry to mature beyond isolated experiments at the edges, we must engage in more rigorous thinking about (i) what innovation experiments actually cost, (ii) what returns they generate, and (iii) how both sides of the equation fare as the endeavor scales. Not all the inputs and outputs of innovation efforts will be quantified in dollars, but much of it can and should be.

The capitalists will enter the U.S. legal mainstream sometime between a few years from now and never. But in the meantime, those on the inside could stand to take a page out of the capitalists’ playbook, starting with the notion that investable ideas must focus on value rather than novelty. Not all new things are better than the status quo, and not all old things are bad enough to be discarded: much like handsome and stupid, innovation is as innovation does.

What’s next? See Legal Innovation Woes, Part II: TBD Markets + MIA Customers (063)